India’s largest multiplex chain, once a stock market favourite, saw its shares tumble nearly 49% from a 2022 peak of ₹2,215 as weak content, box-office flops and falling footfalls pushed audiences toward streaming platforms.

Now, stronger collections, rising occupancy and a promising release slate have helped lift the stock about 10% since its latest earnings. Valuations, meanwhile, sit well below historical averages. For investors, the question is whether this early rebound marks the start of a sustained turnaround—or just another short-lived rally.

We break it down.

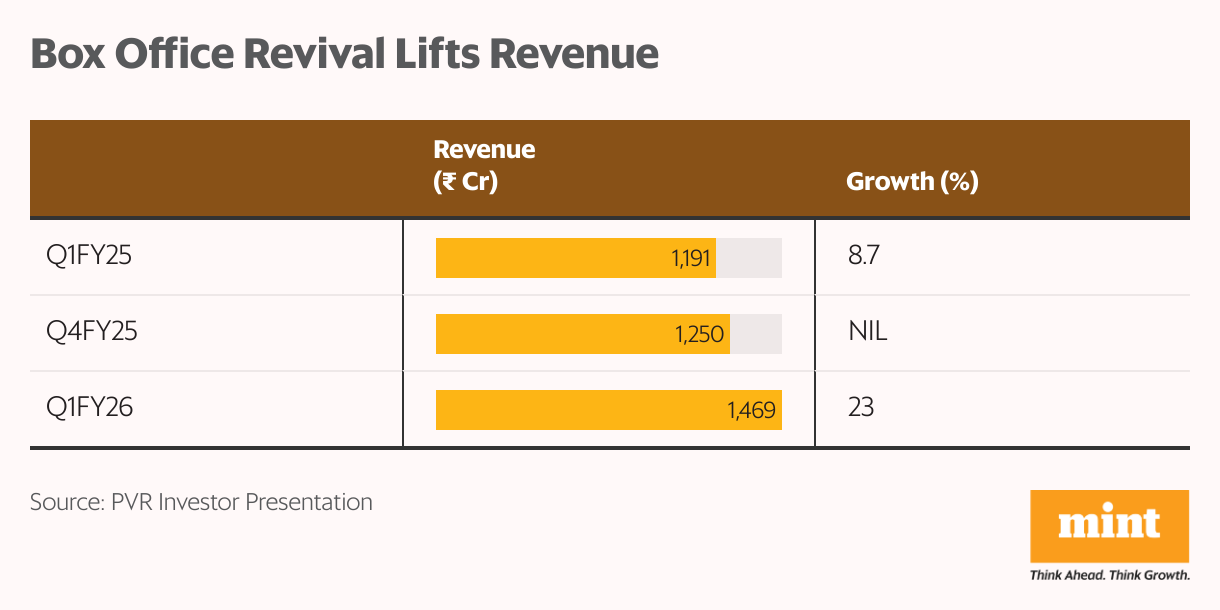

Q1FY26 performance

Consolidated revenue rose 23% year-on-year to ₹1,469 crore in the June quarter of FY26 (Q1FY26), fuelled by stronger box-office collections. Hindi cinema led with a 38% rise, while Hollywood registered an even sharper 72% growth.

With a healthier film pipeline ahead, analysts expect the momentum to continue through the rest of the fiscal year.

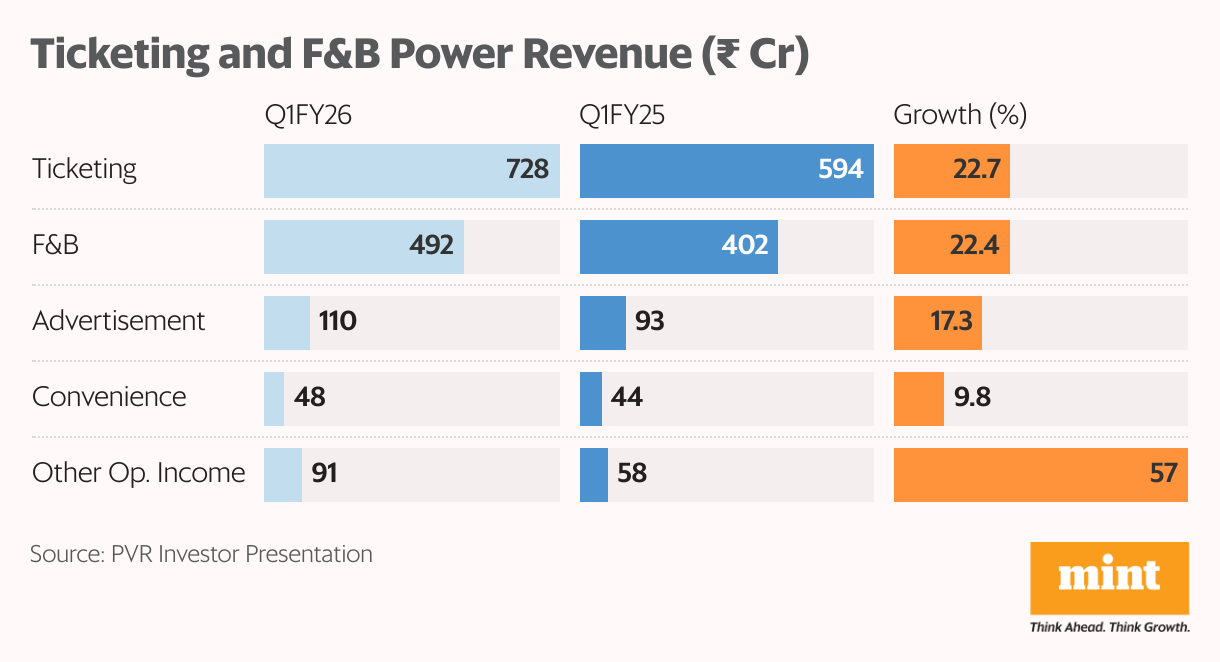

Movie tickets and food and beverages remained the company’s bread and butter. Ticketing revenue rose 22.7% to ₹728 crore, nearly half of overall revenue, while F&B climbed 22.4% to ₹492 crore, contributing 34%.

A ₹99 weekday menu boosted sales among value-conscious audiences, while advertising revenue, at ₹110 crore, was the strongest since the pandemic. The remainder came from convenience fees ( ₹48 crore) and other operating income ( ₹91 crore).

Box office and footfalls

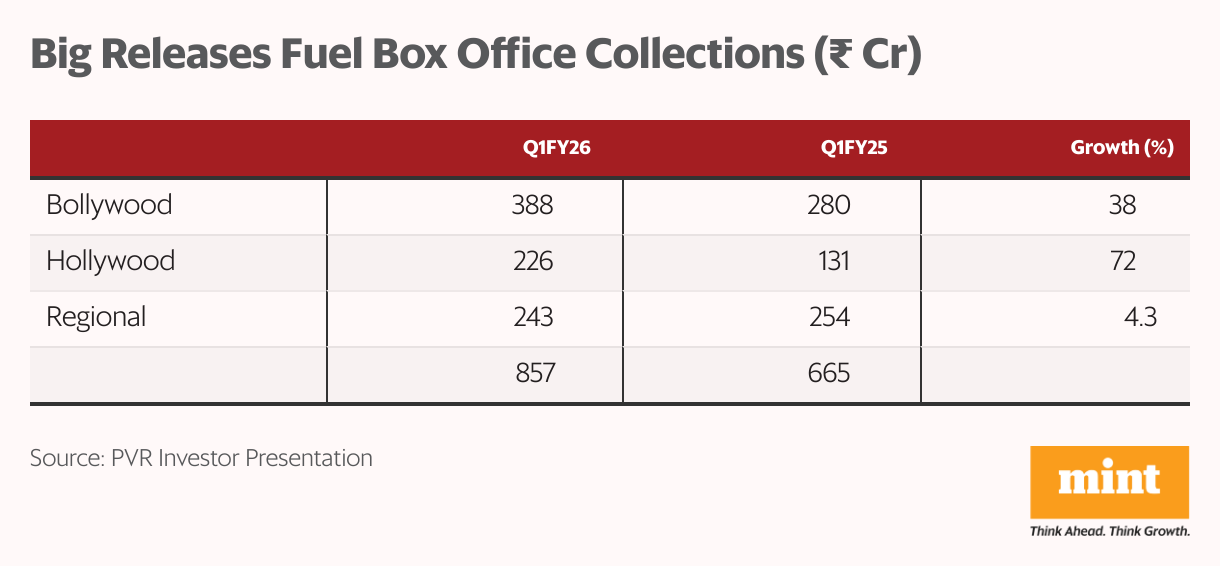

Box-office gains were powered by a string of successful films, including Raid 2, Sitaare Zameen Par, Kesari Chapter 2, Housefull 5, and Jaat. Five Hindi films crossed ₹100 crore, and three surpassed ₹200 crore, pointing to a healthier environment less reliant on single blockbusters.

Hollywood also contributed, with titles such as Mission Impossible: The Final Reckoning, Final Destination, Ballerina, and F1. Regional films, including Good Bad Ugly (Tamil), Thudarum (Malayalam), and Tourist Family (Tamil), pulled in strong numbers.

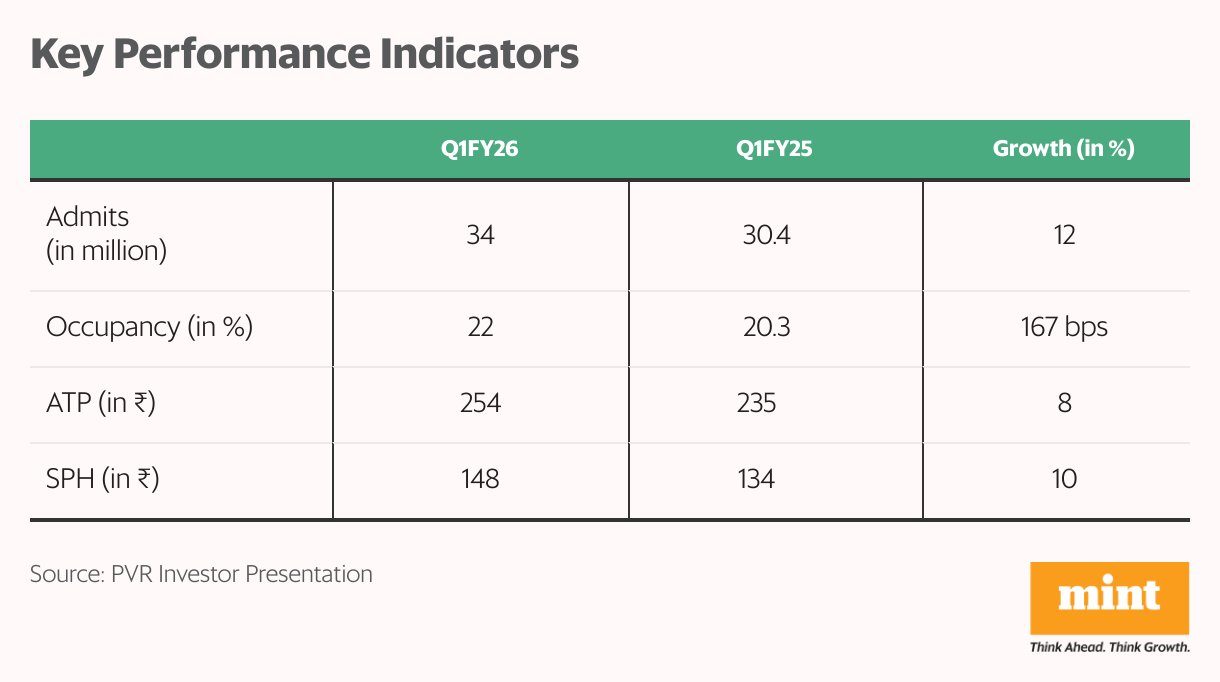

The better content slate translated into higher attendance and spending. Footfalls rose 12% to 3.4 crore, average ticket prices increased 8% to ₹254, and spend per head touched a record ₹148. Unlimited popcorn and Pepsi refills, along with premium pricing for Hollywood films, helped drive spending.

Occupancy rose 167 basis points to 22%, aided by the launch of “Blockbuster Tuesdays,” which drew nearly 1 million new or returning patrons with tickets starting at ₹99. The initiative is aimed at students, homemakers, and retirees, and helped July deliver the highest footfalls in 18 months.

Alternative programming, from IPL streaming to concerts, added another 5 lakh admissions. Management expects total footfalls to surpass FY24’s 15 crore in fiscal 2026, supported by both content and non-film events.

Cost discipline and debt reduction

While revenues improved, so did cost controls. Fixed costs rose just 2.8%, with rentals up 5%—below the 6.2% increase for comparable cinemas—thanks to renegotiations and waivers.

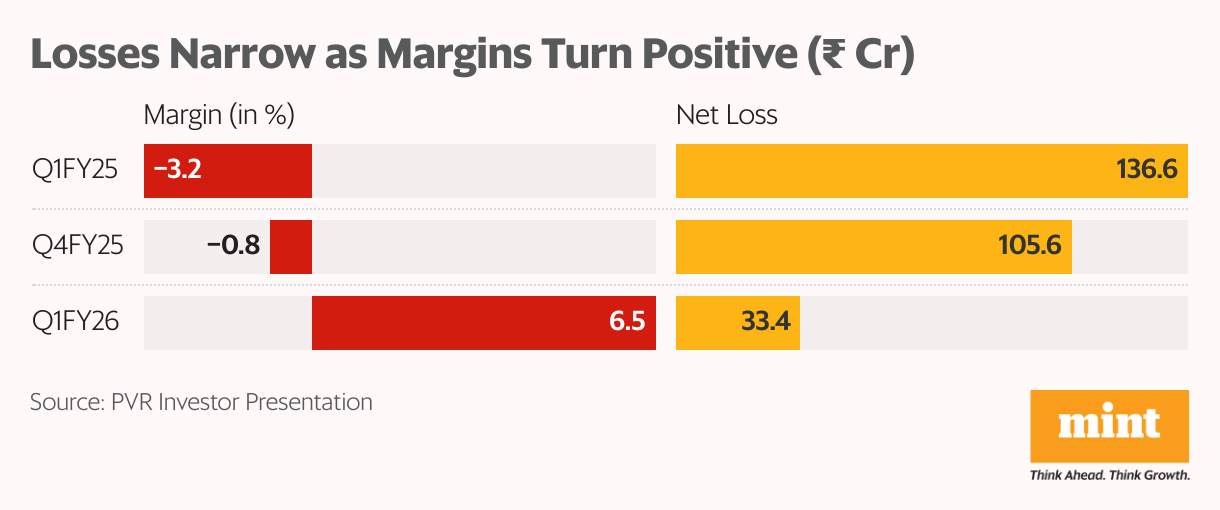

That discipline, coupled with stronger revenues, pushed operating margins back into the black. Ebitda came in at ₹95.3 crore, with margins at 6.5% versus a negative 3.2% a year earlier, at the same 22% occupancy. Net loss narrowed 76% to ₹33.4 crore.

Margins are expected to improve further as occupancy expands, especially with Q3 traditionally being the strongest quarter.

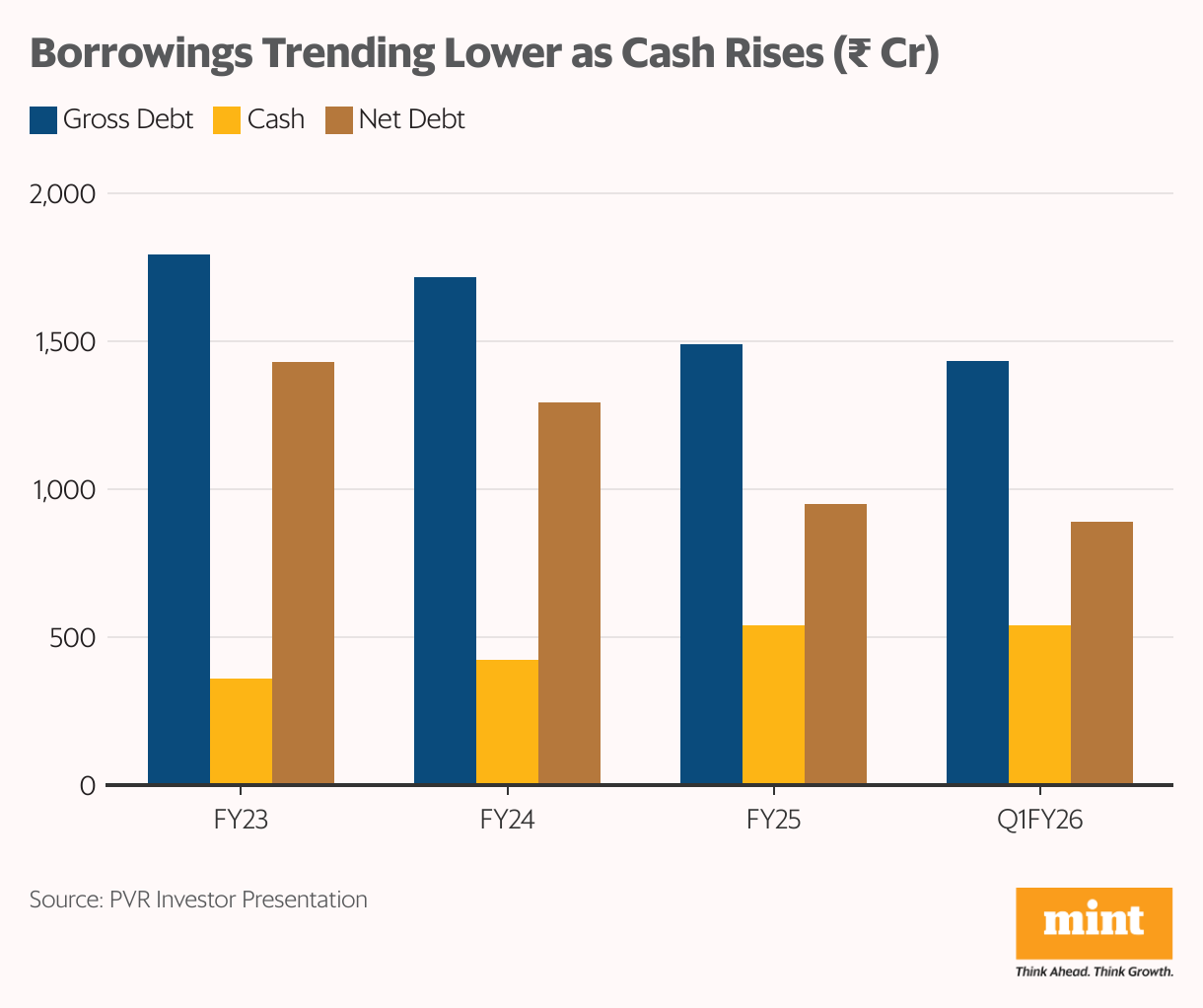

The rebound in profitability has given management more room to manage the balance sheet. Net debt fell 6.3% sequentially to ₹892 crore, with further reductions expected as cash flows improve.

The company has shifted toward a capital-light model, which is helping returns on capital and keeping leverage in check.

Expansion through an asset-light strategy

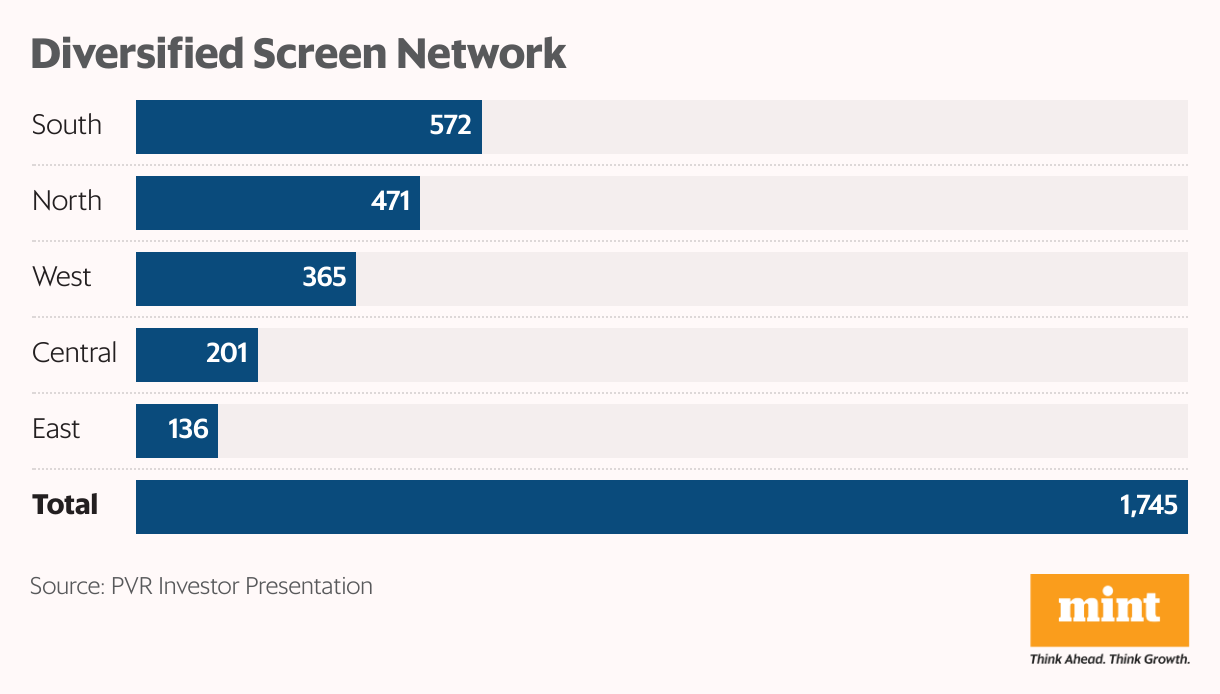

PVR Inox added 20 screens in the quarter, bringing its total to 1,745. Fourteen of those were under the “franchise-owned, company-operated” (FOCO) model, in which developers fund the investment and PVR earns management fees.

The rest were under an asset-light structure that shares investments and rental obligations with developers.

The pipeline is sizeable. Another 55 screens are signed under FOCO and 72 under the asset-light model, with a target of 90-100 new screens in FY26. To support this, PVR Inox has earmarked ₹425 crore in capital expenditure for the year. About ₹260 crore will go into new screens, with another ₹150 crore split between renovations and maintenance.

Valuations at a discount—but risks remain

Valuations provide some cushion. PVR Inox trades at about 10x EV/Ebitda, a 38% discount to its 10-year median of 16. If the current momentum holds and flows through to net profitability, that gap could narrow.

The risks, however, are real. The business is cyclical and heavily dependent on occupancy, which in turn hinges on the strength and timing of film releases. Even a modest 2-3% dip in attendance can weigh heavily on screen-level economics and Ebitda.

For more such analyses, read Profit Pulse.

Regulatory uncertainty adds to the overhang: a draft Karnataka bill to cap ticket prices, if implemented, could squeeze margins further.

For now, though, the stock stands at a crossroads. Footfalls are rising, margins are improving, debt is easing, and valuations remain well below historical averages.

Madhvendra has over seven years of experience in equity markets and writes detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

{kind=link}