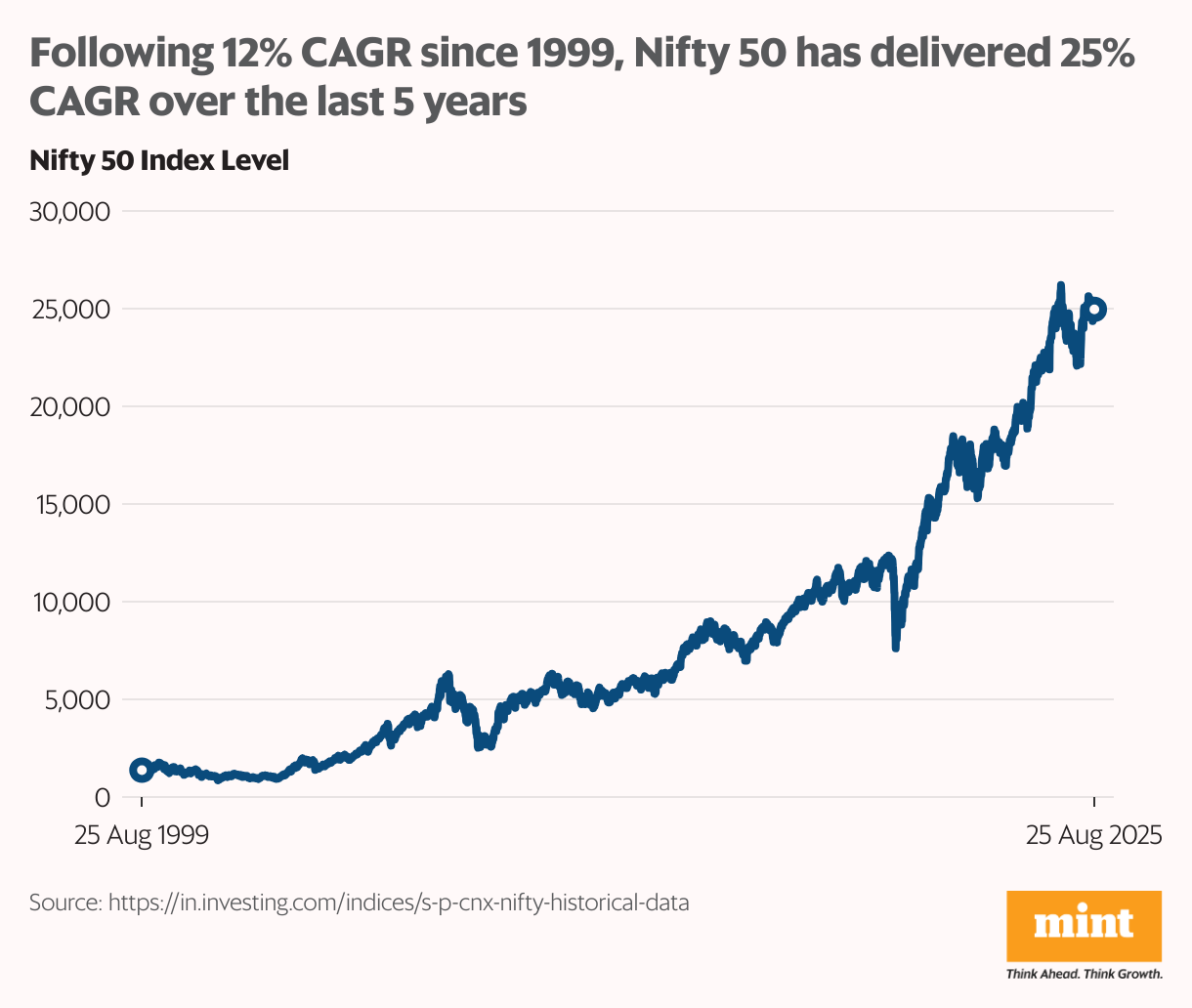

The Nifty 50 index opened over 300 points higher before paring gains, but sentiment has remained buoyant since. To be sure, Indian equities have tripled investor wealth since the pandemic lows—delivering a striking 25% CAGR since April 2020.

Yet, compared with a long-term CAGR of 12% since 1999, the past five years look like an exceptional run. A cooling-off phase was inevitable, and that’s what has played out: Nifty has moved largely sideways over the last 12 months.

That said, even as the broad market index has remained flat, there are undeniable value opportunities at the stock-level. In this article, we shall look at few of the stocks which are still trading around their pandemic-lows.

Stressed industries miss the rally

The market’s post-pandemic rebound was not broad-based. Sectors riding on government-led capex—PSUs, capital goods, and infrastructure—led the charge. Others have been left behind.

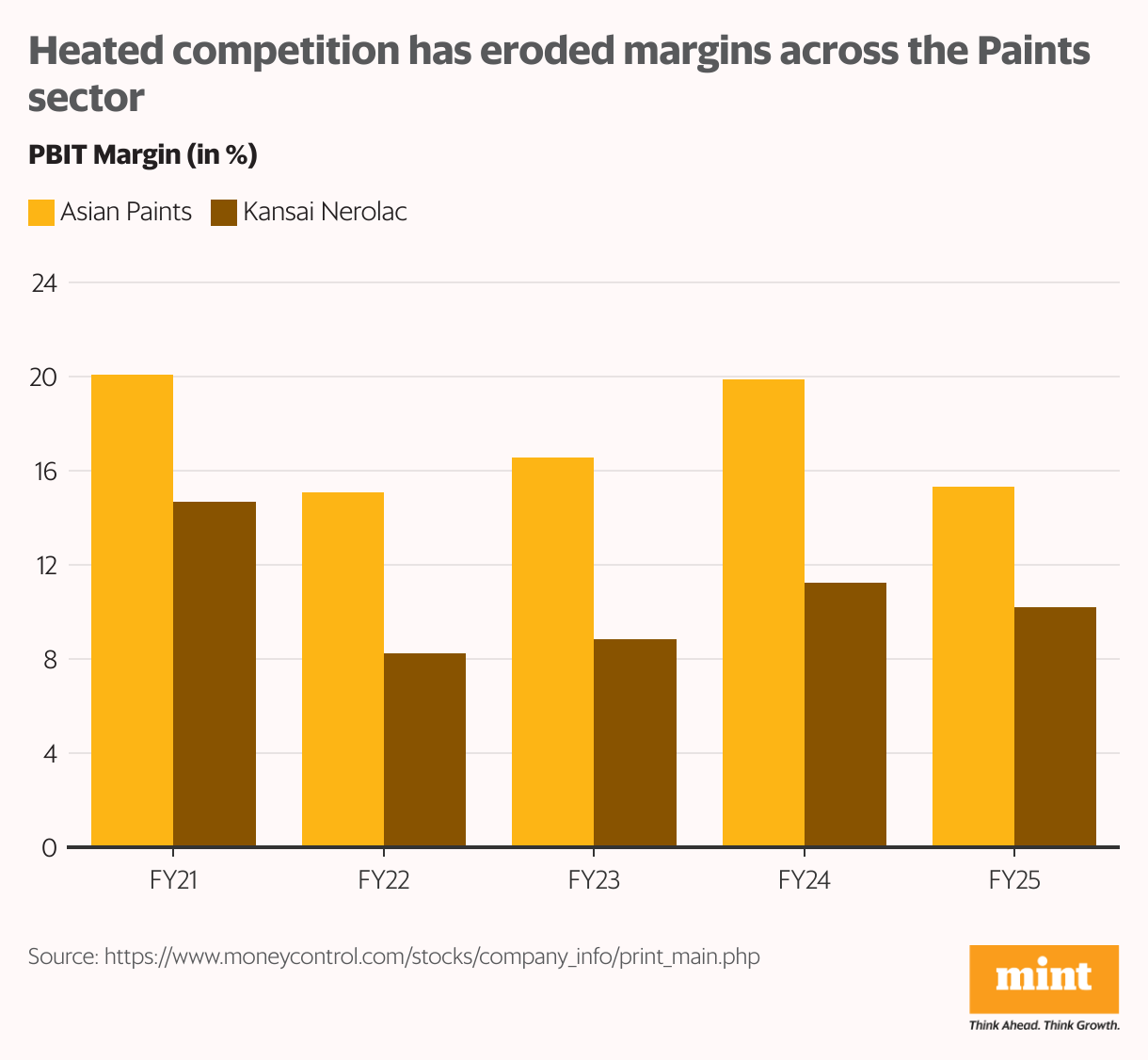

Paints: Competition has intensified sharply. Grasim’s entry with Birla Opus disrupted pricing and distribution, while consolidation reshaped the industry. JSW acquired Akzo Nobel to strengthen its presence, even as leaders like Asian Paints moderated growth outlooks. Smaller players have suffered the most—Kansai Nerolac continues to trade below its pandemic-lows.

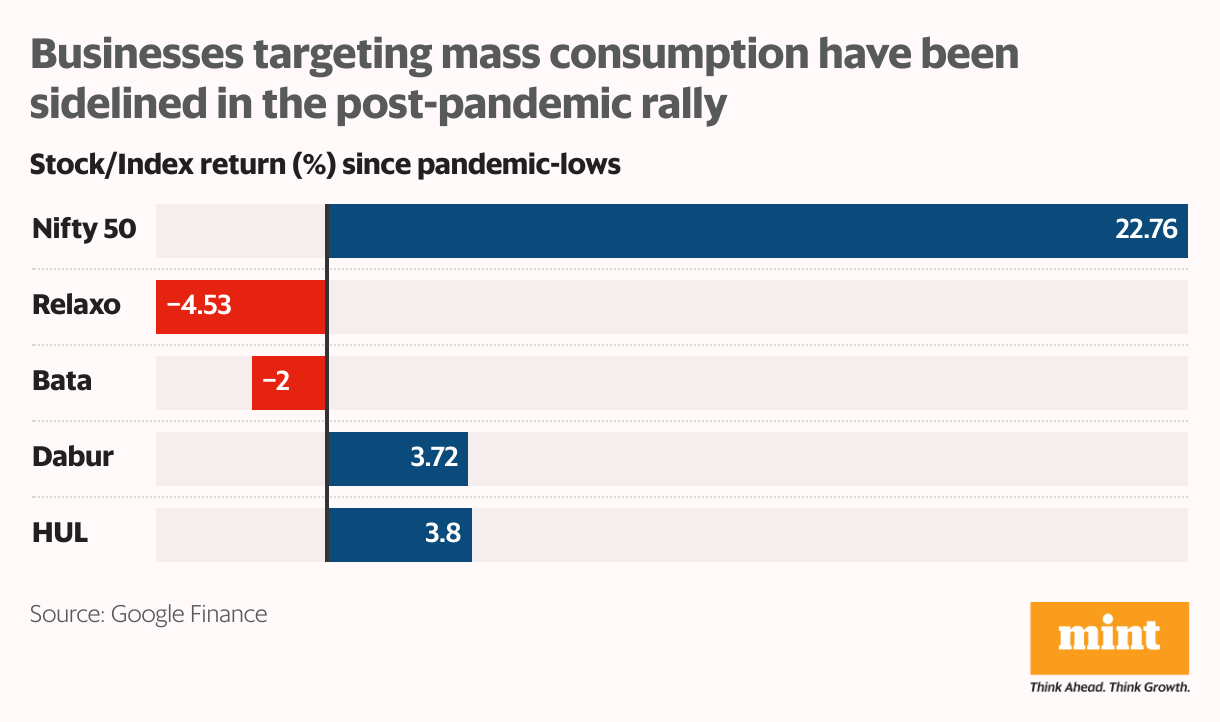

Consumers: The K-shaped recovery has deepened. Rural demand is showing signs of revival on the back of monsoons, but urban mass consumption remains sluggish. Footwear majors Relaxo and Bata, along with FMCG names like Dabur and HUL, have struggled. While premiumisation is underway, brand repositioning takes time.

Chemicals: Export-oriented chemical companies have been hit by protectionism and cheaper Chinese imports. Aarti Industries, once a market favourite, is still reeling.

Entertainment: OTT adoption has eroded theatre footfalls. PVR Inox, once expected to ride a post-pandemic recovery wave, has disappointed.

Microfinance: Weak borrower profiles and rising stress have weighed on lenders. Bandhan Bank has borne the brunt, trading well below its earlier highs.

When poor governance weighs on stocks

Not all underperformers are victims of macro trends—some have fallen prey to governance lapses.

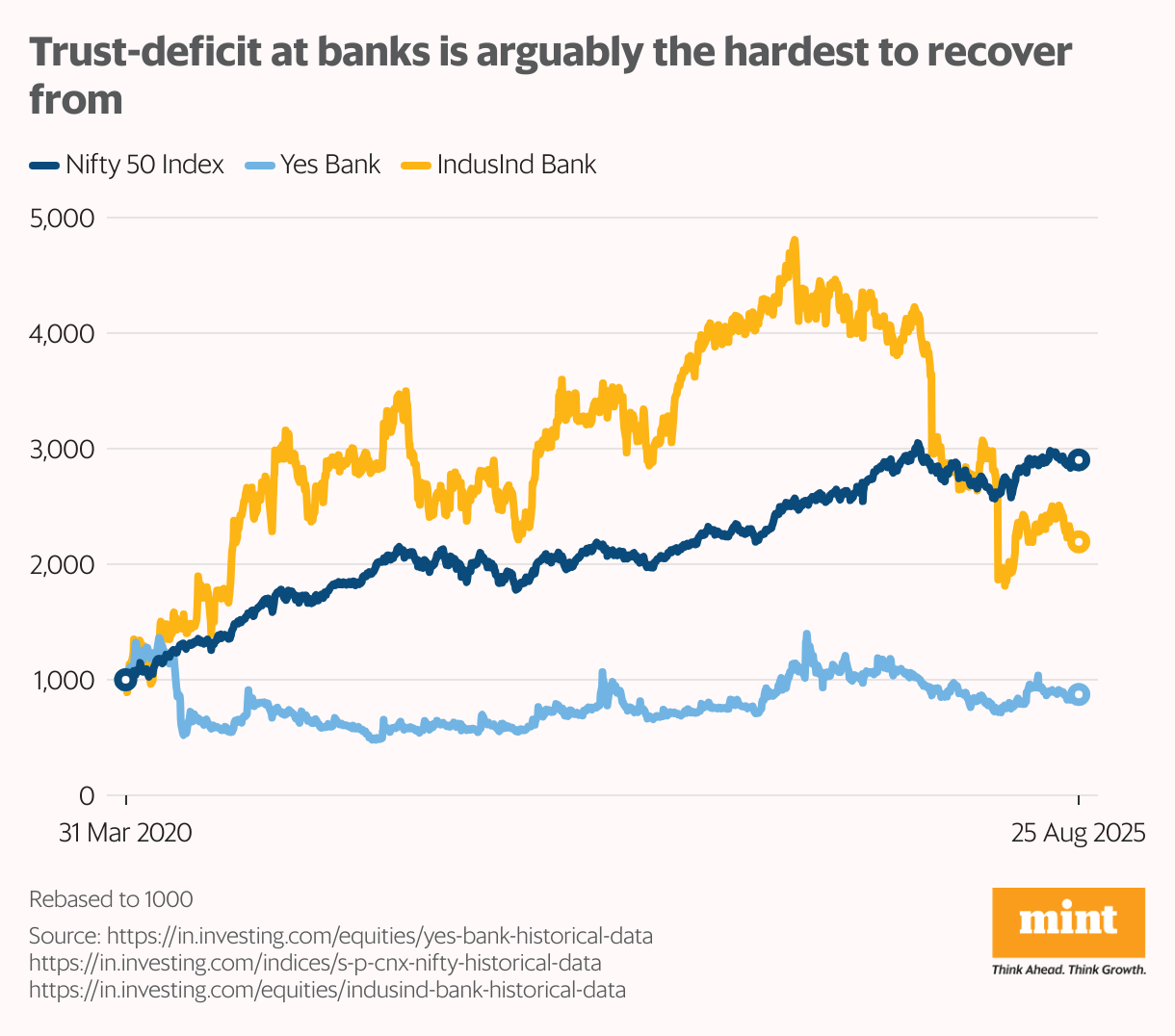

Banks: Yes Bank collapsed under the weight of ballooning non-performing assets (NPAs) and boardroom feuds, while IndusInd Bank faced scrutiny over accounting practices exposed by regulatory changes. Both banks have replaced leadership, but rebuilding trust is proving harder than fixing balance sheets. Depositor confidence, once lost, is not easily regained.

Media: Something similar happened with Zee Entertainment where years of indulgence in debt reached a head during the credit-freeze following the IL&FS crisis in 2018.

The promoters kept reducing their stake to pay off the mounting debt, tanked a potential deal with Sony, got embroiled in fund-diversion allegations by the regulator, and eventually lost the trust of their shareholders. So much so that their latest attempt at rebuilding stake in the company was rejected by the shareholders.

Regulations and misfortune weigh heavy

For some companies, regulatory changes and business missteps have compounded challenges.

City gas distributors: Indraprastha Gas (IGL) and Mahanagar Gas (MGL) lost margin cushion after the government curbed supply of subsidized gas under the administrative price mechanism (APM) mechanism. With higher exposure to industrial and commercial users, IGL still trades near its pandemic-lows.

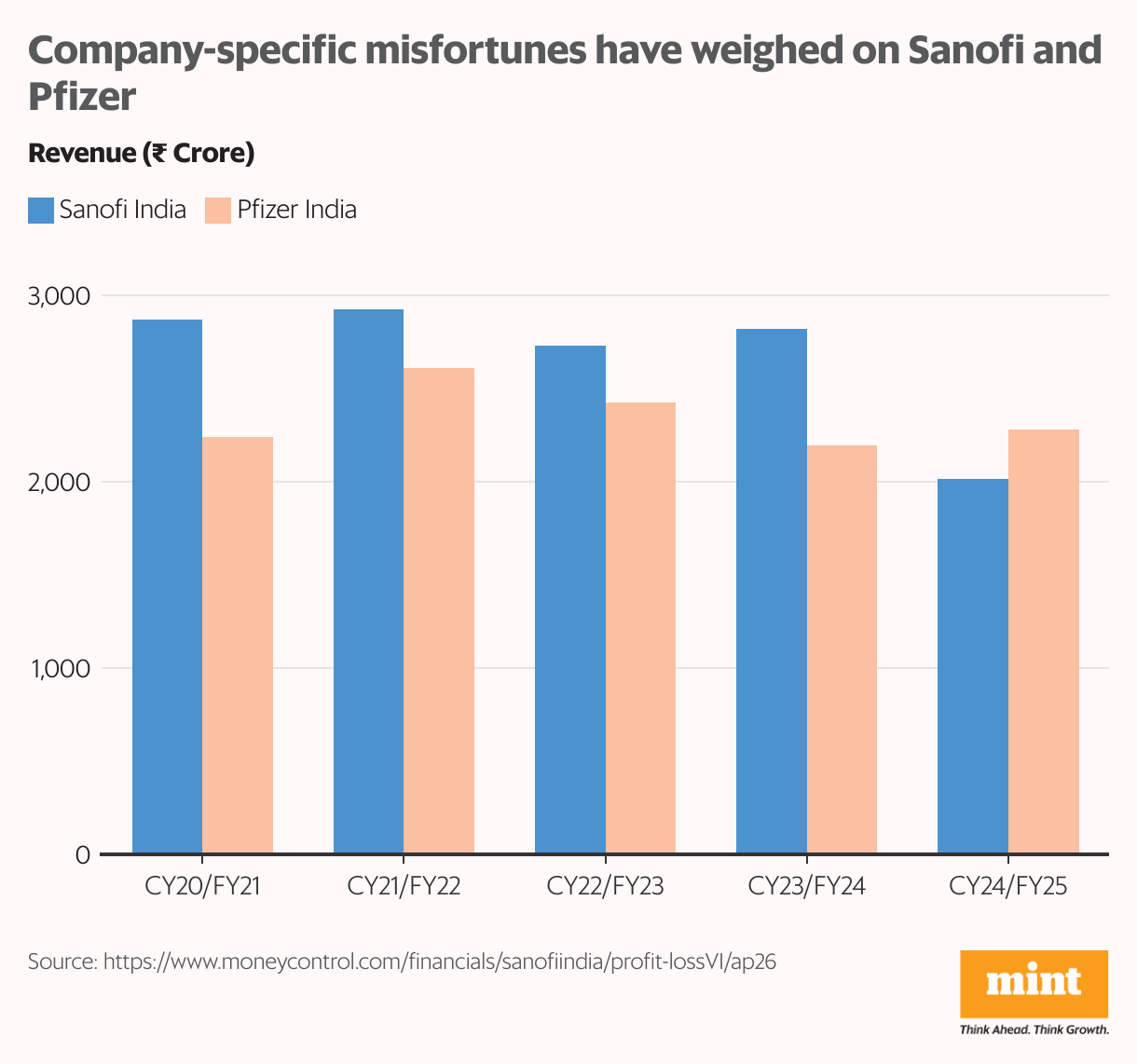

Pharma laggards: Sanofi India, despite spinning off its consumer healthcare arm, disappointed on earnings and divested key brands. Pfizer India, once flush with Covid vaccine gains, has struggled with failed bets in migraine, sickle-cell, and obesity drugs. Activist investor pressure has only added to its woes, erasing pandemic-era gains. That said, upbeat earnings and positive cancer-trial data have recently lifted sentiment.

Bottom line

When scouring the markets for value buys, it is important to note that not all beaten down stocks are worth buying. The thin line that distinguishes a value-trap from a value-buy is whether the business is going through structural or cyclical headwinds.

Structural headwinds—such as governance failures or management shake-ups—often leave lasting scars. Recovery, if at all, is uncertain. Take Yes Bank: despite its 2020 bailout, the stock is yet to regain ground. Zee Entertainment, too, remains mired in going-concern risks that could swing either way.

For more such analyses, read Profit Pulse.

Cyclical headwinds, on the other hand, usually resolve with time. A weak consumption cycle, for instance, will eventually turn, offering long-term investors an opportunity. Higher-beta names in consumer discretionary are more likely to rebound strongly compared with defensive consumer staples.

Somewhere in between these categories of value picks, we have the businesses whose models are inherently risky. Pfizer India, for instance, employs a go-big-or-go-home strategy, that had paid off beautifully during the pandemic. But it has fallen flat since then. Taking calls on such businesses, requires a deep understanding of the sector, and is best left to the experts.

Ananya Roy is the founder ofCredibull Capital, a SEBI-registered investment adviser. X: @ananyaroycfa

Disclosure: The author does not hold shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.

{kind=link}