JK Cement Ltd’s shares have rallied as much as 55% so far in 2025 on strong project execution, healthy earnings show and a clear growth roadmap.

Thus, some brokerages have raised their valuation multiples. For instance, ICICI Securities Ltd now values JK Cementat 22X FY27 estimated EV/Ebitda (18X earlier), tracking its impressive project execution capabilities and its crowning achievement of the past 10 years’ Ebitda per tonne being the most pronounced among cement majors. Ebitda is short for earnings before interest, taxes, depreciation, and amortization.

“RoE (return on equity) too has transcended peers all along,” said ICICI in a report on 1 September. The broking firm reckons JK Cement’s valuation multiple may converge to being at par with peers once growth matures.

JM Financial Institutional Securitiesraised its target multiple by one notch to 18.5X, with strong earnings visibility (>20% Ebitda CAGR), controlled leverage and improving return ratios.

Chasing scale

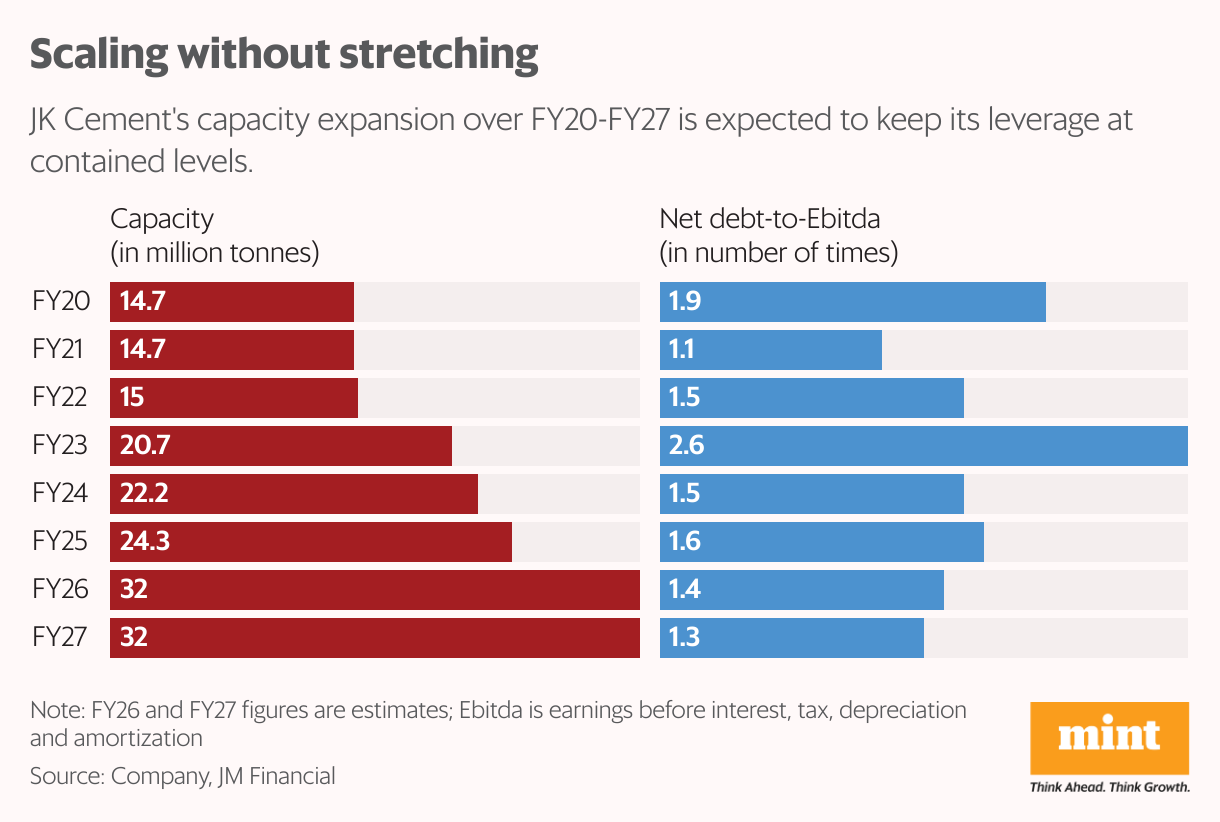

The optimism rests on a sharp capacity buildout and continued market share gains. The cement maker has visibility of about 16% CAGR capacity creation over FY25-30, compared with about 9% in the past decade. Current grey cement capacity stands at 25.26mt and is slated to rise to 31.26mt by December, aided by new units at Panna, Hamirpur, Prayagraj, and a 3mtpa split unit in Bihar. Debottlenecking in the South could potentially take it to about 32mt by FY26.

Additionally, on 15 August, the board approved a 7mtpa greenfield project in Jaisalmer—a 4mtpa clinker unit, 3mtpa grinding unit and two split grinding units of 2mtpa each in Rajasthan and Punjab, at a cost of ₹4,805 crore, to be commissioned by September 2027. This project is part of the company’s broader plan to expand capacity to 50mtpa by 2030.

Meanwhile, it saved ₹40-50 per tonne in costs in FY25 and expects another ₹40-50 per tonne in the coming quarters through a higher share of blended cement, greater use of renewable power and automation, with the ambition to rank among the lowest-cost producers in the industry.

Furthermore, JK Cement has signed a limestone supply agreement for future expansion. It also received allocations for two coal blocks in December 2024, which should improve fuel security and reduce volatility in input costs.

Its June quarter (Q1FY26) performance was healthy. Grey cement volumes rose 15% year-on-year, with consolidated revenue growing at 19% to ₹3,353 crore. Ebitda per tonne came in at ₹1,247 versus ₹1,014 last year. FY26 guidance is steady. The management expects grey cement volumes of 20mt, an 11% year-on-year growth, ahead of industry growth.

Testing execution

Still, scale comes with risks. While JK Cement is guiding for cost cuts, freight costs are set to rise as it pushes further east, and petcoke prices have edged higher. Importantly, the expansion will also lift debt. “With rising scale, JK Cement’s balance sheet remains robust, and despite planned capex of ₹7,000 crore over FY26-28, we expect consolidated net debt to peak at about ₹4,000 crore in FY27 (versus ₹3,200 crore in FY25). Net debt-to-Ebitda is projected to remain <1.5X, supported by healthy operating cash flow generation through the period,” noted JM Financial in a 16 August report.

At an 18X FY27 EV/Ebitda valuation multiple, based on Bloomberg, the stock is already priced for flawless execution. The real test, now that can decide if the rally still has legs, is if JK Cement can maintain its execution streak through its endeavour to double capacity.

In general, pricing trends are key for all cement stocks, including JK Cement, so investors should follow that closely.

{kind=link}