But the stock price over the past few years tells a different story, as well-funded companies have entered the paints sector. Asian Paints has felt the heat, and subdued demand and rising competition have taken a toll on growth. Valuations have thus softened, weighed down further by muted discretionary spending.

However, now may be the right time to re-examine Asian Paints.

Let’s dive in.

India’s paints behemoth

India’s foremost paint and home decor company, Asian Paints ranks among the top 10 decorative coatings companies worldwide, with a group turnover of ₹33,800 crore.

With operations spanning 14 countries and 26 state-of-the-art manufacturing facilities, the company sells its products in more than 60 countries. It has more than 169,000 retail touchpoints across India, and this vast network is expanding all the time.

It has a diverse family of brands including Asian Paints Berger, Apco Coatings, SCIB Paints, Taubmans, Asian Paints Causeway, and Kadisco Asian Paints.

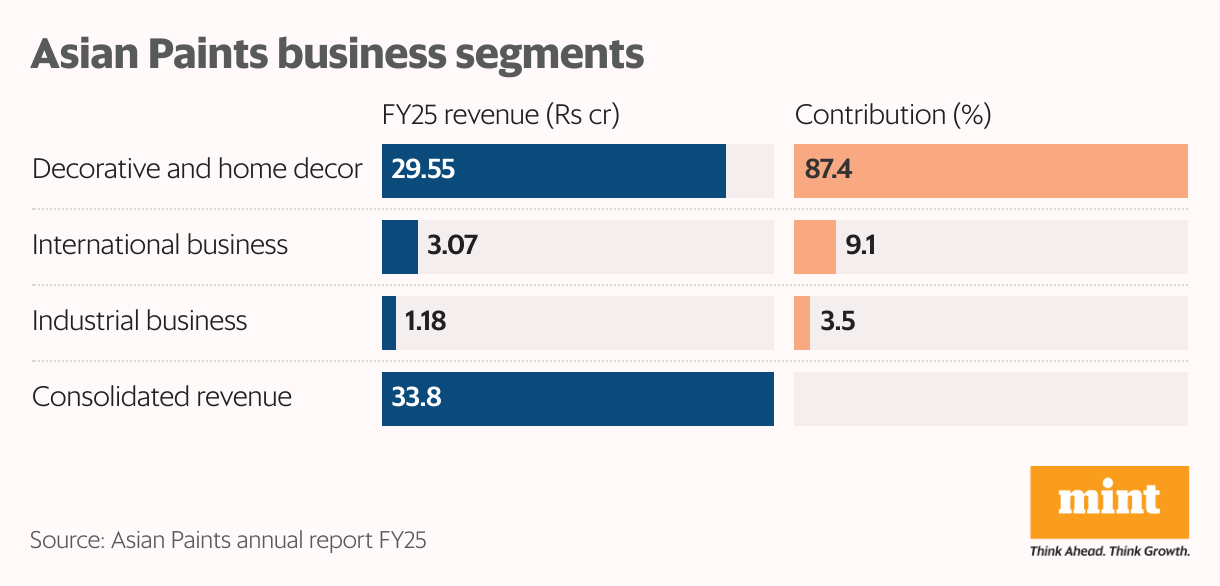

Business segments

The company operates across three business segments: decorative and home decor, industrial, and international.

Decorative and home decor accounts for 87.4% ( ₹29,500 crore) of the company’s revenue. It includes offerings for the ‘bottom of the pyramid’ such as Neo Bharat, the Sparc range under Tractor Emulsion and Ace, and premium and luxury emulsions such as Protek, Royale Glitz, and Nilaya Arc.

Asian Paints also offers end-to-end personalised interior design with professional execution.

It’s also a leading integrated home decor player, offering modular kitchens and wardrobes, bath fittings, decorative lighting, uPVC windows, and doors.

View Full Image

It is a leading decorative lighting company with the White Teak brand.

Asian Paints is also the leader in wall coverings, collaborating with global players such as Pierre Frey and Sanderson Design Group.

It is the number two player in furniture and fabrics, operating 72 home stores across 54 cities.

Asian Paints’ international operations account for 9.1% of revenue. It operates in 13 countries across four key regions, including South Asia, the Middle East, Africa, and the South Pacific.

The industrial segment accounts for 3.5% of revenue. It operates through a joint venture with PPG Industries, focusing on automotive, general industrial, and marine coatings.

Decorative paints and home decor

Asian Paints has been grappling with several sectoral challenges, including competition from new entrants and lower discretionary spending owing to slower economic growth.

Management said FY25 was a challenging year for the entire domestic coatings industry as demand was subdued. It said the organised paint industry, especially the decorative sector, recorded negative growth in FY25 – unprecedented in the last two decades.

This has weighed on its financials, dampening growth. In FY25, standalone revenue declined 5.4% year-on-year to ₹29,400 crore, despite a 2.5% rise in volumes. However, value declined 5.7%, a sign that competition is intensifying and eroding its pricing power.

On the positive side, volume growth of 3.9% in Q1 FY26 was the highest since Q2 FY25, indicating that demand may be seeing a revival. However, value growth remained negative at -1.2%, though it improved from -3% in Q1 FY25.

Discounting by new entrants to gain market share forced Asian Paints to offer promotional benefits and reduce prices.

This company’s net fixed assets increased from ₹4,640 crore in FY23 to ₹7,930 bn in FY25, but demand did not keep pace with the expansion. As a result, asset turnover fell sharply to 3.7 from a high of 6.5.

View Full Image

The kitchen business remained flat at ₹390 crore, and the bath segment grew just 5% to ₹350 crore. Both are still in the red.

White Teak revenue declined 20% to ₹100 crore owing to headwinds such as BIS specifications, weak urban markets, and import challenges. The company has written down its ₹100 crore investment in White Teak, recognising a fair value loss of ₹78.5 crore on derivative contracts for future stake purchases in White Teak.

Earnings before interest, tax, depreciation, and amortization (Ebitda) fell 19.6% YoY to ₹6,300 crore. Ebitda margin declined to 21.4%, from 25.2% in FY24.

As a result, profit after tax fell 32.6% YoY to ₹3,580 crore, even lower than the ₹4,100 crore recorded in FY23. This weighed on its return ratios. The return on capital employed fell to 28.4% from a high of 41.2% in FY24.

This slow growth and mixed with a high valuation has caused its share price to appreciate just 28.3% over the past five years.

The company expects competition to remain intense, but it’s banking on brand saliency to drive growth recovery. It anticipates an improvement in demand, particularly in urban markets, on the back of a normal monsoon, government spending, an income tax cut, and a GST reduction.

International business faces headwinds

The international business reported 0.2% growth to ₹3,070 crore, driven by the Middle East, which grew 14%. The Middle East is the biggest overseas market, accounting for 37.4% of international business revenue. It’s followed by Asia (40.9%), Africa (18.3%), and the South Pacific.

It saw 24% negative growth in Africa, mere 3% growth in Asia, and was flat in South Pacific. The Africa business was impacted by currency devaluation and high inflation in Egypt and Ethiopia.

The company expects geopolitical uncertainty in many markets, which could hamper growth. However, international remains a tiny part of the overall business.

Industrial segment revenue rose 6% to ₹2,140 crore while profit before tax rose 5% to ₹370 crore. The segment recorded broad-based growth driven by the general industrial and automotive segments.

View Full Image

Asian Paints’ consolidated revenue declined 4% to ₹33,900 crore, led by subdued performance of the paints business. Gross margin fell 7%, meaning it’s making less profit on each unit sold after covering direct production costs. PAT fell 3.3% to ₹3,710 crore.

Cautious outlook

In FY26, Asian Paints aims for single-digit value and volume growth, and an Ebitda margin of 18-20%.

The company is focusing on sustainable, long-term growth drivers, not short-term gains. Innovation, brand prominence and new offerings are expected to drive growth amid intense competition, driven by an anticipated recovery in government spending, mid-to-luxury housing, and rural demand following a good monsoon.

The company is on an innovation spree, having launched over 300 new products and secured more than 130 patents in the past five years. It is setting up a futuristic, environmentally friendly emulsion plant (vinyl acetate monomer emulsion) with an investment of more than ₹3,000 crore. To this end, the company plans capital expenditure of ₹700-800 crore each in FY26 and FY27.

This plant, one of only four facilities worldwide with such technology, is expected to be partially operational by March-April 2026 and fully operational by April 2027. It is expected to significantly enhance margins and product quality thanks to the versatility, environmental benefits (low volatile organic compounds and no odour), and other unique properties of the emulsion.

The white cement plant in Fujairah, Dubai, with a capacity of 275,000 tonnes, was scheduled to be completed by June 2025, marking Asian Paints’ entry into the cement industry, with potential for future expansion into other types of cement.

The company is also continuing its premiumisation drive, including revamped packaging and ingredient marketing for products such as Ultima Protek with graphene and Royal with teflon. It is also offering value propositions for products such as Ace and Tractor Emulsion with campaigns such as ‘Budget Kam, Warranty Mein Dum’.

In the home decor segment, it plans to deepen category penetration in existing stores by offering comprehensive decor solutions under one roof using technology-based in-store innovations. The company is expanding premium retail formats, such as Beautiful Homes Studio and Signature Stores. It is also expanding its distribution reach, seeing vast potential in smaller towns, suburbs, and smart cities.

The goal in international markets is to consolidate its position as one of the top two players.

Conclusion

Asian Paints finds itself at a crossroads. Once a relentless compounding machine, it is now navigating muted demand, stiff competition, and pressure on profitability.

While valuations have cooled to historical averages, a recovery in housing, government spending, and rural demand could revive growth.

With its strong brand, wide distribution, and renewed focus on innovation, Asian Paints still holds long-term promise, but investors must weigh near-term challenges against its structural strengths.

However, instead of relying only on hype, it is necessary to carefully analyse the company’s fundamentals, including financial performance, corporate governance practices, and growth prospects before deciding whether to invest.

Happy investing!

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com

{kind=link}