National Securities Depository Ltd (NSDL), the rival of Central Depository Services (India) Ltd (CDSL), was listed in August. Investors in NSDL’s public issue got shares at ₹800 apiece and are now sitting on handsome gains of nearly 60%. The main difference between the two depository companies is that, unlike CDSL, NSDL has a subsidiary NSDL Payments Bank (NPB).

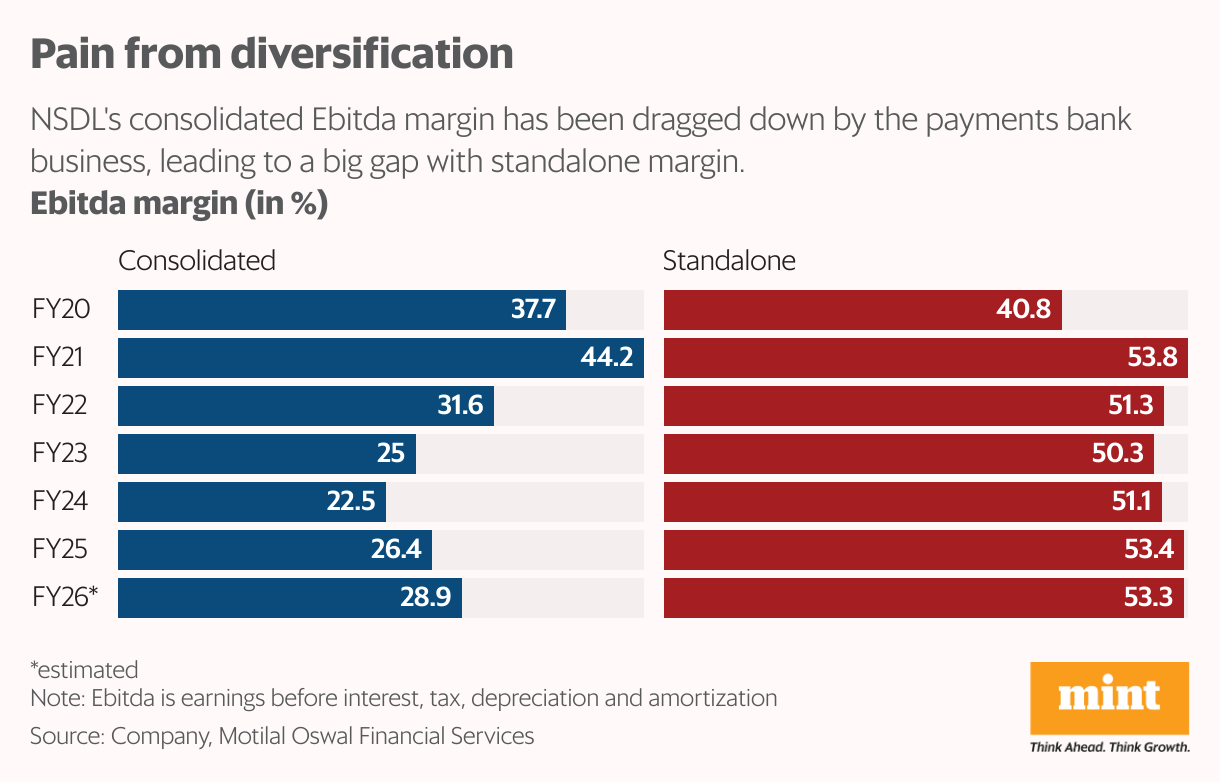

What sets a payments bank apart is that it cannot give loans and must deploy deposits in government securities. So, the earnings of fund-based banking business cannot be combined with NSDL’s non-fund business of a depository for valuation and assigned a price-to-earnings (P/E) multiple. This can be further illustrated by the fact that NSDL’s FY25 standalone Ebitda margin was at 53.4% versus the consolidated margin of 26.4%, which was dragged down by the banking business.

The CDSL stock trades at 49 times FY27 earnings per share (EPS), based on Motilal Oswal Financial Services’ estimates. The broking firm initiated coverage on NSDL on Tuesday and estimates non-bank revenue of ₹870 crore and a standalone PAT margin of 52% for FY27. This gives an EPS of ₹22.6.

Applying CDSL’s P/E multiple, NSDL’s non-banking business is valued at ₹1,106. Since NSDL stock now trades at ₹1,290, NPB’s implied valuation is ₹184 per share. Effectively, it means the Street is valuing NPB at nearly ₹3,700 crore if its value per share is multiplied by NSDL’s 200 million outstanding equity shares. This is far higher than Fino Payments Banks Ltd’s market capitalization of ₹2,316 crore.

NPB’s valuation premium is even more striking, given its FY25 book value was ₹150 crore versus ₹720 crore for Fino. So, NPB is being valued at price-to-book-value of 24x versus 3x for Fino. Also, NPB has two branches with total customer deposits of ₹180 crore versus 152 branches and ₹1,940 crore deposits for Fino.

Motilal Oswal points out that NPB has launched a three-in-one account service that integrates banking, demat and trading services. This structure is open to leading discount brokers. This proposition positions NSDL uniquely within the capital markets ecosystem. Still, the valuation premium looks too big.

Alternatively, if NPB’s valuation is assumed to be on par with Fino’s, then it means the Street is assigning a higher P/E multiple to NSDL’s depository business versus CDSL’s. Either way, NSDL’s stock is more expensive than CDSL.

{kind=link}