{kind=link}

Mint decodes the trend.

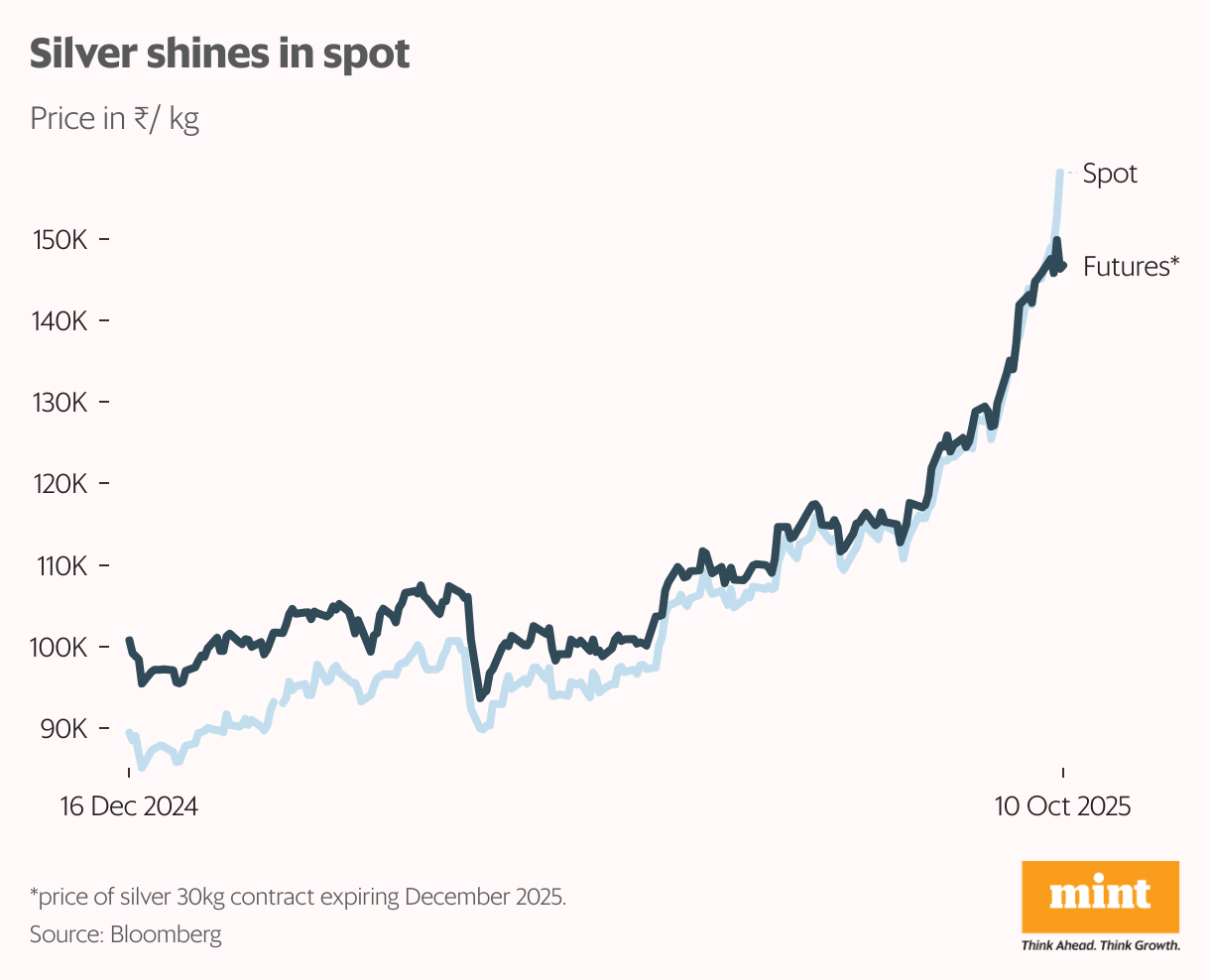

A surge in retail demand for silver ahead of Diwali is upending bullion prices in the spot market. Rising consumption of silver coins and jewellery, along with heavy inflows into silver exchange traded funds (ETF), is further distorting a domestic silver market already in so-called backwardation. Backwardation is a market phenomenon where the spot price of a commodity exceeds its futures price, often signalling supply constraints or excess near-term demand.

What caused the spike in silver ETF premiums?

Globally, silver prices are in backwardation too, owing to stagnant supply and strong demand from industries. But delivery bottlenecks are amplifying distortions in the domestic market, experts said.

“A large silver dealer I know had ordered 2,500 kg nearly two months ago has received only 600 kg so far, with no confirmed timeline for the remaining delivery,” a markets expert said, asking not to be identified.

Consequently, as dealers fell behind in sourcing silver to meet the surge in ETF inflows on Thursday, unit prices began trading at a premium to the physical silver they are designed to mirror.

Is silver’s rally a blinding shine?

In light of ongoing silver scarcity, Kotak Mutual Fund has temporarily halted fresh subscriptions to its Kotak Silver ETF Fund of Fund.

UTI Mutual Fund has cautioned investors that its Silver ETF units are trading at a steep premium to their indicative net asset value, which could hurt future returns. “Purchase at current price may adversely affect the future returns realised by investors,” it said.

Meanwhile, institutional profit booking has brought some liquidity to the market, easing premiums towards the end of the day on Thursday, said Satish Dondapati, fund manager at Kotak Mahindra AMC. Funds reported premiums as high as 10-14% in the morning which eased to 6-7% by day end. “But bar availability is still thin in the spot market,” Dondapati added.

How tight is the physical silver market right now?

While quotes for bulk volumes are in-line with global prices, the pain is sharper for retail buyers of physical silver. Premiums in the physical market, from Sarafa Bazaar to Zaveri Bazaar, have surged to ₹7,000-15,000 per kg amid tight supply, said Naveent Damani, head of commodities and currencies research at Motilal Oswal Financial Services.

That’s because smaller lots are commanding higher premiums, with mini and micro contracts trading well above the standard 30-kg ones, Damani noted. The 30-kg standard silver contracts align with refinery inventories and institutional supply chains, so they closely track international spot prices. Mini (5-kg) and micro (1-kg) contracts draw from smaller dealer inventories that deplete quickly during retail rushes, pushing up premiums.

When stocks are tight and logistics slow, converting large bars into smaller ones becomes costly, preventing quick arbitrage, Motilal Oswal’s Damani said. “Hence, premiums on smaller contracts are likely to be elevated going forward.”

At this juncture, silver ETFs may fare relatively better, as they can manage supply more efficiently, noted Bhargav Vaidya, an independent bullion expert.

Why doesn’t gold usually behave like this?

Silver’s richer cousin, gold, also has been touching fresh life-time highs on ongoing uncertainties but its market behaviour is strikingly different. Gold’s market is deeper and more liquid, backed by central bank reserves, bullion-bank leasing, large ETF holdings, and a mature distribution network — making shortages rare. With gold’s higher per-kg price, minting and handling costs form only a small fraction of its value, keeping premiums on small bars far lower than in silver, said Vaidya.

Hence, silver’s lower price makes it far more sensitive to short-term inventory disruptions, amplifying its volatility — a trait that’s earned it the moniker “the devil’s metal”.

Are high silver prices here to stay?

Yet, some commodity experts believe there is still steam left in the silver rally.

Kaynat Chainwala, associate vice president for commodity research at Kotak Securities, said silver’s rally reflects supply tightness rather than mere market frenzy. Global deliverable inventories at Commodity Exchange Inc (COMEX) and London Bullion Market Association (LBMA) are thin as supply from mines has remained stagnant, she noted.

“Of roughly 500 million ounces sitting on COMEX only about 180 million are readily deliverable, while LBMA inventories can meet the global demand for only about eight months,” Chainwala said.

With supply already tight, any fresh wave of buying on expectations of strong industrial demand could trigger a short squeeze, she said. “If spot prices sustain above $50 per ounce for several days, silver could surge to $55–60 per ounce,” she added.

The current supply deficit to demand is currently recorded at 20%, and is expected to be in deficit for the foreseeable future, said Emkay Wealth Management in a recent report. They expect the price of silver to touch $60 per ounce in the next one year, a potential of 20% y-o-y from the current price level owing to growing industrial demand.

Yet, Chainwala cautioned that silver’s dual role as an industrial and precious metal makes it far more volatile than gold. Any talk of tariffs on US bullion imports or signs of a US economic slowdown could drag prices back to around $40 an ounce.