{kind=link}

ICICI Prudential Life Insurance Co. Ltd’s stock is down about 10% so far in calendar year 2025, even as peers HDFC Life Insurance Co. Ltd and SBI Life Insurance Co. Ltd have delivered positive returns. The company’s muted September-quarter (Q2FY26) performance suggests this lag may persist.

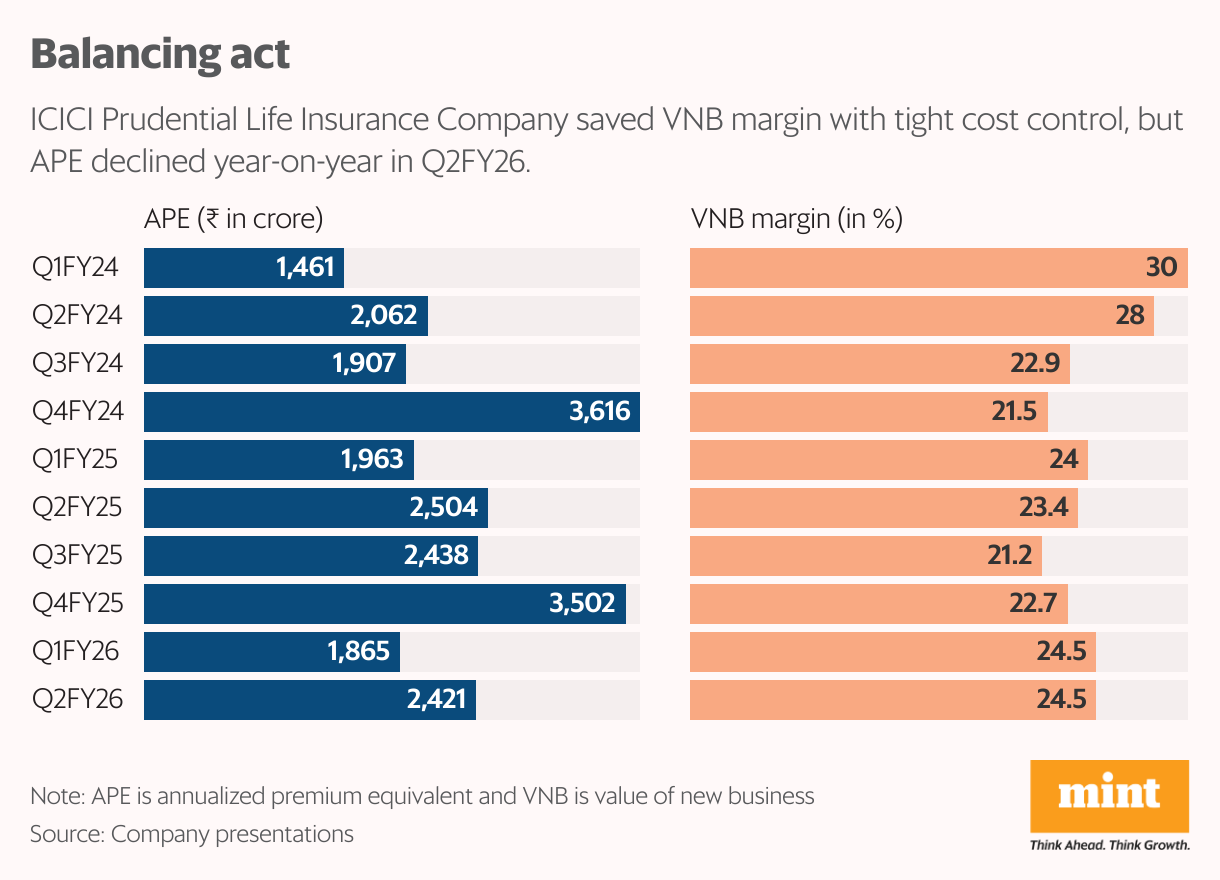

The insurer’s annualized premium equivalent (APE) fell 3.3% year-on-year to ₹2,421 crore on an unfavourable base, dragged by weaker sales of unit-linked insurance plans (Ulips), which dropped 8.5% to ₹1,187 crore. Ulips still made up nearly half of APE, but the decline likely reflects volatility in Indian equity markets. In contrast, Ulip demand had surged in the year-ago quarter when the Nifty 50 hit a record high of 26,277—momentum that has not carried through.

Tight cost controls, driven by technology initiatives and operating leverage, helped offset the slowdown. Total expenses declined 5.1%, outpacing the fall in APE, allowing ICICI Prudential to eke out a modest 1% year-on-year rise in the value of new business (VNB) to ₹592 crore. VNB margin improved by around 105 basis points to 24.5%.

Higher margin could be due to the revival in premium income from traditional non-linked saving insurance policy that rose by around 12% year-on-year to ₹1,187 crore. The company’s non-participating guaranteed income products, that are more in the nature of investment, have seen good traction as policy buyers wanted to lock in higher rates in view of declining interest rates over the last couple of quarters. The impact of loss of input tax credit on profitability, however, remains to be seen.

The performance of other segments was less encouraging. Annuity sales (retirement products) nearly halved year-on-year to ₹116 crore in Q2FY26, possibly due to delayed decisions by buyers awaiting clarity on the goods and services tax (GST) rate on insurance products.

GST reduction increases the internal rate of return (IRR) of an annuity product as they become cheaper unless the company decides to reduce the benefit. But even in Q1FY26, ICICI Prudential saw annuity sales fall sharply. Further, term insurance was flat in Q2FY26 with APE at ₹419 crore. As such, both the products put together accounted for about 25% of total APE in Q2FY26.

Industry headwinds

Moreover, ICICI Prudential’s Q2FY26 presentation highlights that scenario is not rosy at the industry level. Total premium-to-GDP ratio, an indicator of insurance penetration, peaked out at 4.1% in FY10 and stood at 2.8% in FY24. During the same period, new business premium or retail weighted received premium (RWRP), though up from ₹55,000 crore to ₹1.09 trillion in absolute terms, has shown a CAGR of only 5%.

In short, India’s life insurance industry has failed to sustain its once-lofty growth expectations. Against this backdrop, ICICI Prudential will need more sustainable growth levers to regain investor confidence.

“On a 12-month rolling basis, (ICICI Prudential) IPRU’s individual rated new business de-grew 4% versus a 9% growth for private life insurers, as IPRU has struggled to find a stable product mix. We revise our FY26E/FY27E APE growth forecasts to 1% (from earlier 11%), on the back of a weak H1,” said HDFC Securities report dated 15 October.

Despite the stock’s underperformance, ICICI Prudential quotes at a price-to-VNB—an economic profit substitute for accounting profit that is used for calculating P/E—of 26x based on FY27 estimates of Motilal Oswal Financial Services.

In comparison, HDFC Life trades at 30x and SBI Life at 22x. After a lacklustre Q2FY26, ICICI Prudential could face further de-rating, which may narrow the valuation gap with SBI Life.