{kind=link}

The Street reacted differently to the September quarter (Q2FY26) results of India’s top private sector banks, HDFC Bank and ICICI Bank. HDFC Bank’s stock remained flat, while ICICI Bank’s shares fell 3%. Investors may have been drawn to HDFC’s seemingly stronger net profit growth of 10.8% year-on-year, compared with ICICI’s 5.2% increase.

However, this market response may have overlooked three key factors.

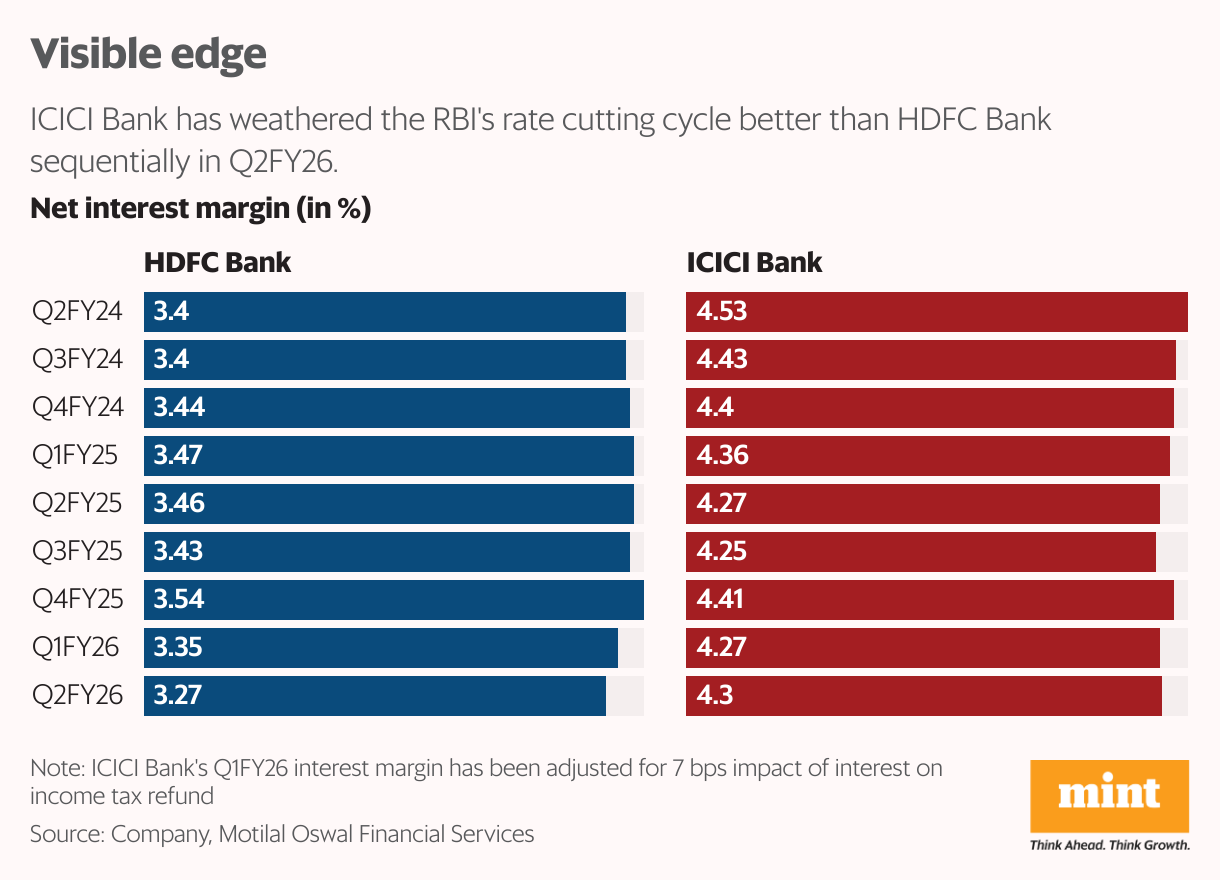

The first is the quality of earnings, where ICICI Bank outperformed HDFC Bank in core operations. Adjusted for interest on income tax refunds, ICICI Bank’s net interest margin (NIM) rose 3 basis points (bps) sequentially to 4.3% in Q2FY26, while HDFC’s NIM slipped 8 bps to 3.27%. ICICI’s margin expansion stems from the relatively faster repricing of liabilities on the lower side compared with HDFC.

As HDFC’s treasury gains, a volatile stream of income for banks, grew almost eight times year-on-year (YoY) on a smaller base to about ₹2,400 crore, its net profit growth reached double-digit. In contrast, ICICI’s treasury gains declined a steep 68% YoY to ₹220 crore, weighing on profit growth.

The threat of NIM compression still looms large as there could be further rate cuts by the Reserve Bank of India (RBI). While the inflation forecast has turned more benign in view of the goods and services tax (GST) rate cut, opening up space for monetary easing, the RBI might be prompted to act if it sees any threat to the GDP growth rate. In such a scenario, ICICI Bank appears better positioned than HDFC Bank to absorb additional rate cuts, based on its current NIM trajectory.

The second factor is the loan-deposit ratio (LDR). HDFC Bank faces pressure to bring its LDR down. The bank’s intention is to reduce its LDR over the long term to about 87%, even as the ratio jumped 300 basis points sequentially to 98% in Q2FY26. To achieve this, HDFC will need to either slow loan growth or boost deposits—both of which could weigh on net interest income. ICICI, by contrast, faces no such constraint, with its LDR already at 87%.

The third factor is ICICI’s return on average assets (RoAA), which is estimated at 2.3% for FY26—significantly higher than HDFC’s 1.8%, according to Motilal Oswal Financial Services. This not only justifies ICICI’s premium valuation, but also positions the bank to grow earnings more rapidly in the future, given its balance sheet of ₹21 trillion—roughly half the size of HDFC’s. A smaller balance sheet inherently provides ICICI Bank with greater flexibility and agility to scale its operations and capture growth opportunities.

Premium pressure

Recently, ICICI Bank’s valuation premium over HDFC Bank has narrowed, with the former trading at 2.6x compared with the latter at 2.5x, based on Motilal Oswal’s FY26 estimated price-to-adjusted-book-value (P/ABV), which accounts for the valuation of subsidiaries. This narrowing of the valuation gap enhances ICICI’s relative attractiveness.

In the lending business, the book value continues to grow as long as no losses are reported, which can make the price-to-book-value (P/BV) appear cheaper over time. However, FY26 earnings growth for both banks is expected to moderate to around 10%, well below the high growth rates seen in the past. As a result, price-to-earnings multiples—again adjusted for subsidiary valuations—of 18x for HDFC and 16x for ICICI may offer limited upside.