{kind=link}

From January to September, the Nifty 50 has returned just 4.09%, per Bloomberg.

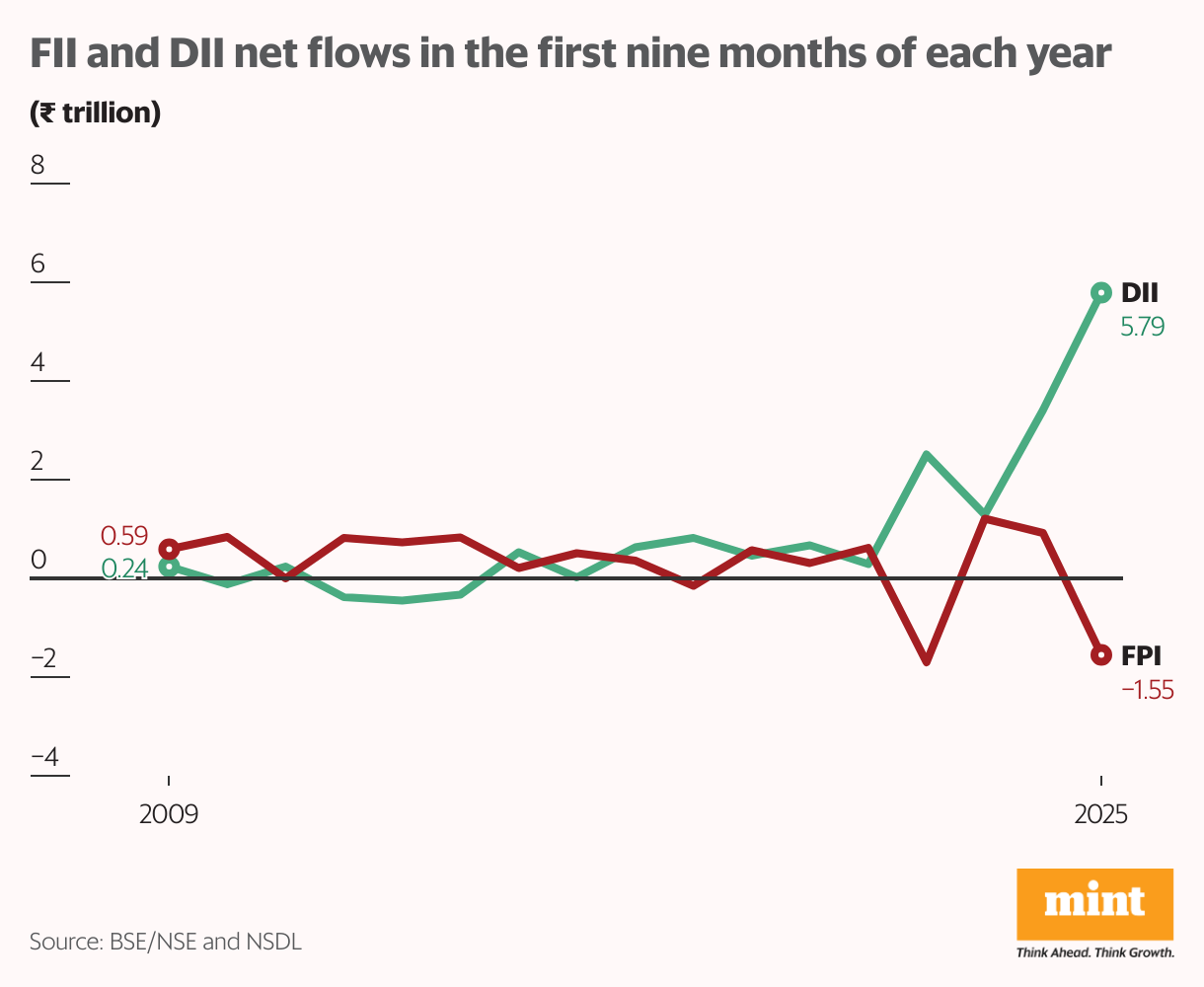

In contrast, foreign investors have net sold Indian stocks worth ₹1.5 trillion during the same period—slightly lower than their record sell-off of ₹1.7 trillion in the corresponding period of 2022, as per National Securities Depositories Limited (NSDL), National Stock Exchange (NSE), and BSE.

“(Domestic) flows are primarily driven by steady SIP (systematic investment plan) inflows rather than volatile lump sum investments. This regular, disciplined investing behaviour has helped cushion sentiment even when markets have been range-bound,” said Sahil Kapoor, head of products, financial services provider 360 ONE Wealth.

SIP contributions rose 28% year-on-year to ₹2.46 trillion during the nine months, according to the Association of Mutual Funds of India (Amfi).

Moreover, higher equity allocations from long-term pools such as the National Pension System (NPS), limited opportunities to diversify globally, and relatively sub-optimal post-tax returns from debt have all contributed to sustained equity flows, Kapoor added.

To be sure, Indian mutual funds are subject to an overall industry-wide investment limit of $7 billion for overseas securities, as well as a separate $1 billion cap for international exchange-traded funds (ETFs). This limit is already breached, and it only opens up if an investor withdraws money.

The NPS’ equity assets under management (AUM) stood at ₹1.41 trillion as of the end of August—the latest available data. The estimated NPS investments in equities are based on Scheme E (Tier I and Tier II) allocations. The NPS Trust, however, does not disclose data on monthly or annual inflows into equity markets.

No other choice

Foreign institutional investors (FIIs) have turned heavily underweight on India. Their exposure to the country, relative to its weight in the MSCI Emerging Markets Index, is close to a 16-year low, according to Alok Agarwal, head-quant and fund manager at portfolio management services provider Alchemy Capital Management.

On the other hand, domestic institutional investors (DIIs) continue to invest on the back of strong retail flows, as their universe is usually limited to Indian markets, which sustains their buying momentum, in our view, Agarwal added.

Also, apart from weak markets, DIIs have little choice but to continue investing, as holding back and allowing FIIs to also stay out would likely lead to significant market weakness and, consequently, redemptions, said G. Chokkalingam, founder of equity research and advisory firm Equinomics.

If DIIs stay on the sidelines now when FIIs sell, the erosion in valuations would hurt them the most, he added.

However, going forward, some caution may set in, which may dampen the sentiment for DII flows, said Sudeep Shah, head of technical and derivatives research at financial services provider SBI Securities.

“The lingering US-India trade uncertainties, especially around tariffs and technology transfers, could weigh on export sentiment and investor confidence,” he said.

“Secondly, the energy cooperation uncertainties with Russia, coupled with rising crude oil prices, can pose inflationary and fiscal challenges for India. Lastly, corporate earnings failing to meet expectations can make near-term positioning more selective,” he added.