When momentum builds around popular names, investors often overlook steady compounders hiding in plain sight. That is where bottom-up discipline matters.

The focus should be on businesses that generate strong cash flows, operate efficiently and carry little or no debt. Prefer those that remain sensibly valued despite their dominance. Some of the best examples sit among India’s monopoly-style companies that command high market share and possess structural moats.

These are businesses that form the backbone of the economy, whether in capital markets, energy, transport, bioengineering or natural resources. Their scale, regulation-driven entry barriers and balance-sheet strength allow them to compound steadily through economic cycles.

Here are five of the most enduring monopoly-style stocks to watch in 2026.

It is important to note that the monopoly stocks featured here are based on their leadership in the sector, clean balance sheets, strong return ratios and visible growth plans.

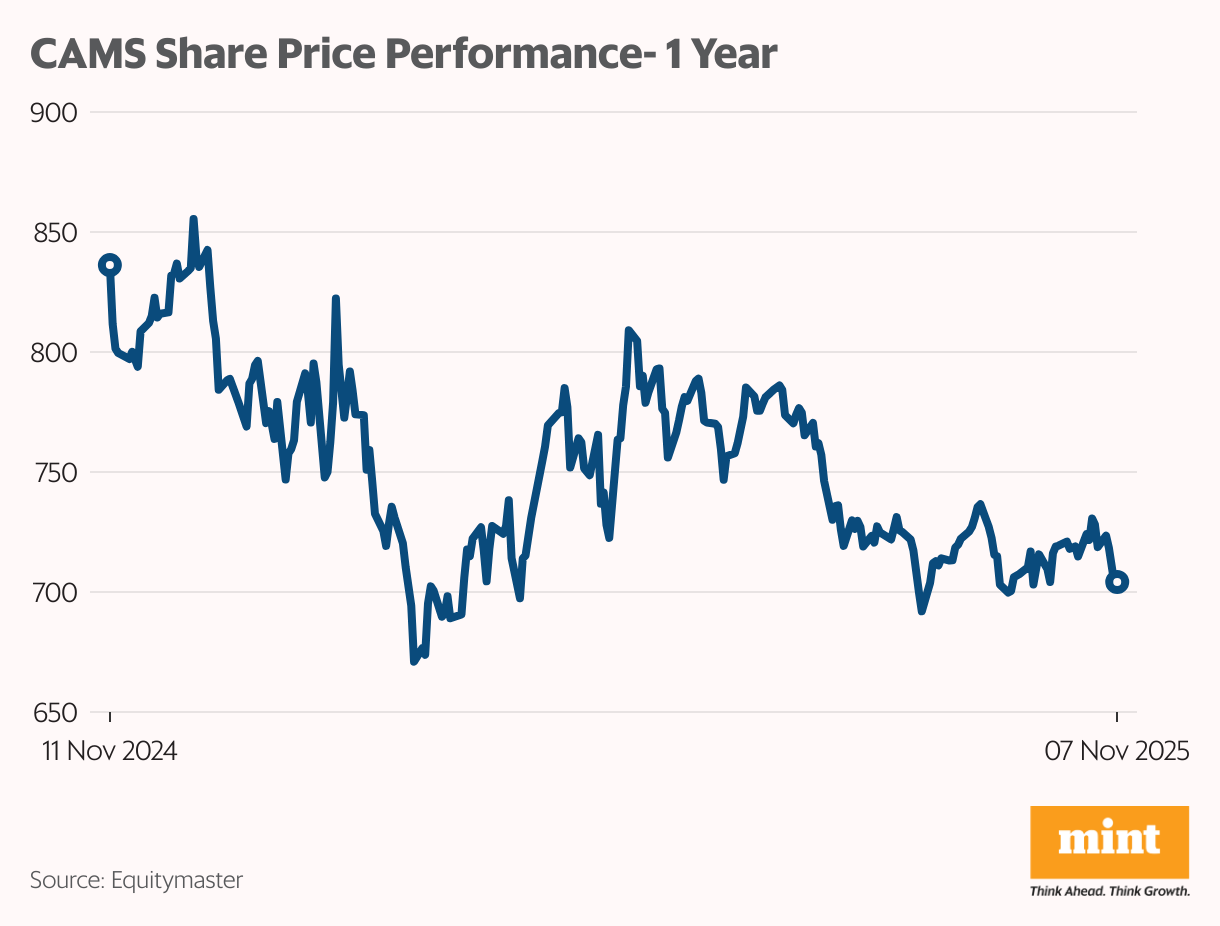

Computer Age Management Services Ltd

Computer Age Management Services (CAMS) is the largest registrar and transfer agent for India’s mutual fund industry, servicing over half of the industry AUM. The company processes millions of transactions daily. This is across mutual funds, insurance and alternative assets, making it one of the most entrenched back-end platforms in India’s financial ecosystem.

For investors tracking monopoly-style stocks, CAMS stands out for its near-unchallenged leadership and its ability to convert industry inflows into steady, high-margin cash flows.

The company’s overall FY25 top line grew about 26.6%, with an Ebitda margin of 46%. Margins benefited from operating leverage in mutual fund servicing and the rapid recovery in CAMSPay and KRA businesses. A minor yield compression earlier in the year, due to repricing by a large client, was offset by scale and better mix.

In Q2FY26, CAMS reported its highest-ever quarterly revenue, led by strong momentum in both mutual fund and non-MF segments. Mutual fund revenue rose 6.4% sequentially and 3.2% year-on-year, while non-MF revenue jumped 17.9% sequentially.

Looking ahead, the management is prioritizing scaling non-MF lines to take that mix to roughly 20% over the next three years and to monetise NSE KRA integration from Q4FY26. The company’s capex remains limited to software and cloud migration. It expects to fund growth from internal accruals rather than large external borrowing.

The stock trades at about 43x earnings, close to its five-year median of 44.8x. For a portfolio built on durable franchises, this monopoly-style compounder offers a steady play on India’s deepening savings cycle.

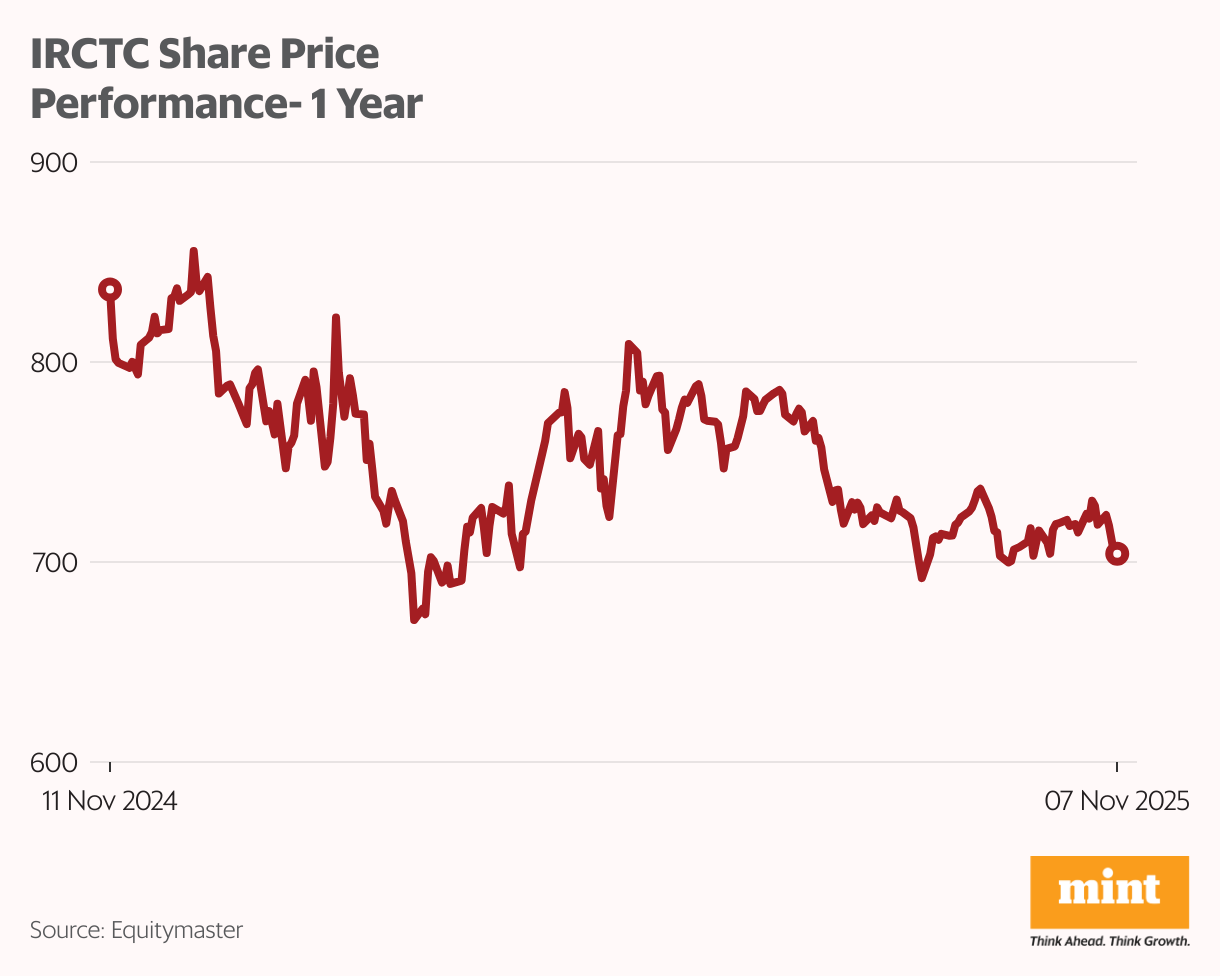

Indian Railway Ctrng nd Trsm Corp. Ltd

Indian Railway Catering and Tourism Corp. (IRCTC) is one of India’s largest integrated travel and hospitality platforms. It covers catering, online ticketing, tourism and packaged drinking water under the Rail Neer brand.

With more than 87% of reserved rail tickets booked through its portal, the company sits at the heart of India’s travel infrastructure.

For a monopoly-style watchlist, IRCTC matters because it converts captive demand into recurring, high-margin cash flows across multiple verticals.

In FY25, IRCTC’s revenue from operations grew 10% and Ebitda margin stood at 33%. In Q1FY26, revenue rose about 4% on-year and Ebitda margin expanded to 34.27% as internet ticketing grew 9% and tourism jumped 21%.

Catering dipped modestly due to election-special base effects and station upgradations even though e-catering volumes were up >30%.

Looking ahead, management aims for Rail Neer capacity additions at Danapur and Ambernath and new plants planned at Prayagraj, Ranchi, Bhagalpur and Mysore.

Management expects final approval for a payment-aggregator licence in about 12-18 months and plans to scale e-catering, tourism and value-added ticketing services.

Capex is limited and focused on plant expansions and tech upgrades; management expects to fund these from internal accruals.

At present, IRCTC is trading near a P/E of 43, a deep discount to its long-term median of 66.

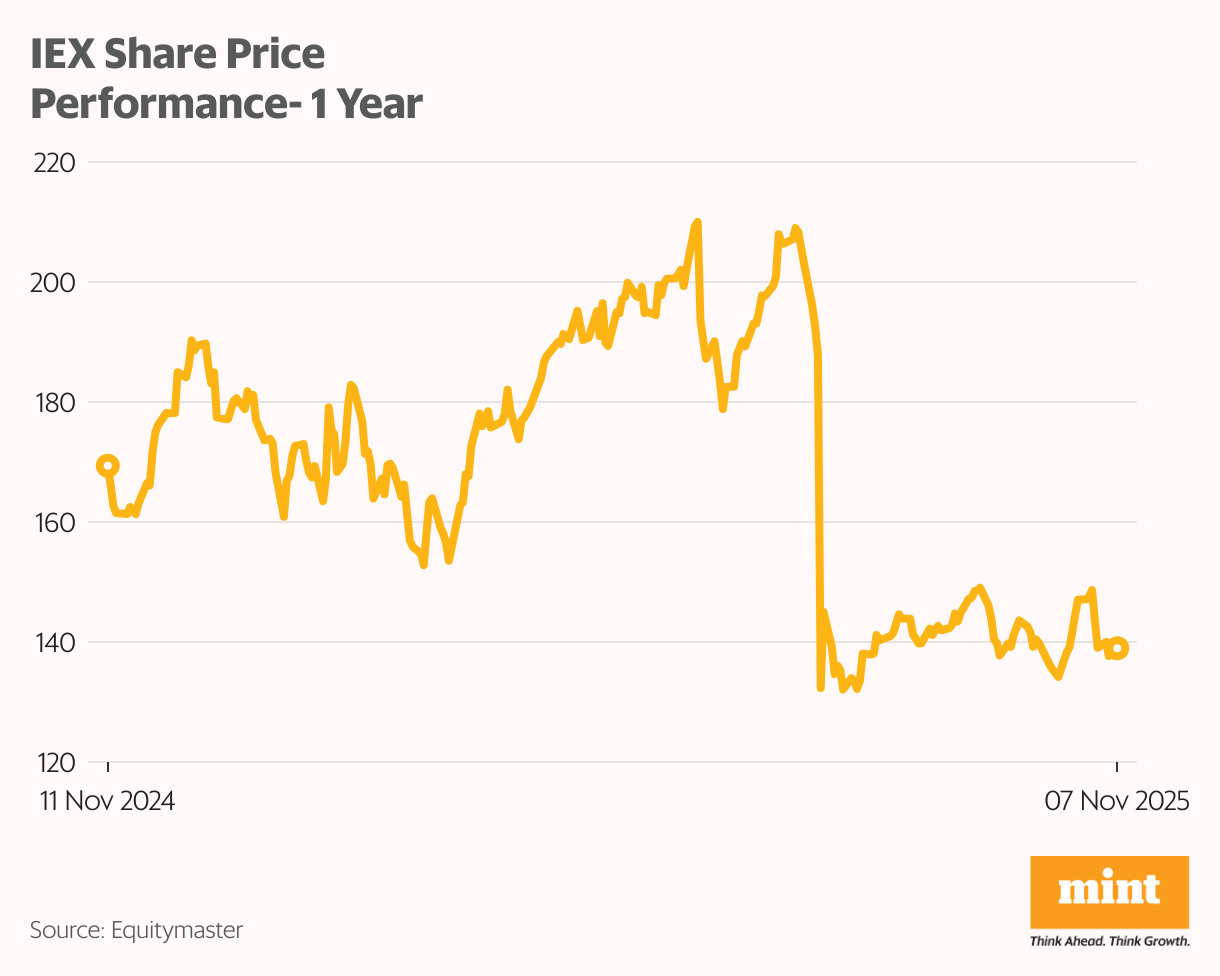

Indian Energy Exchange Ltd

Indian Energy Exchange operates the country’s largest power trading platform. It enables transparent and automated electricity, green energy and certificate trading. The exchange handles more than four-fifths of India’s short-term power market volumes and serves as the benchmark for price discovery in electricity.

For a monopoly-style watchlist, IEX stands out for its dominant franchise, asset-light model and strong operating leverage within a regulated market framework.

In FY25, IEX’s revenue rose 19.6% on-year, while Ebitda margin stood at a robust 84%.

The margin resilience reflects higher traded volumes of 121 billion units and improved liquidity in green and real-time markets.

During Q2FY26, revenue grew 9.3% on-year, supported by a 16% increase in electricity traded volumes. Ebitda margin expanded to nearly 87%, aided by cost discipline and increased sell-side participation that kept prices stable.

The stock came under sharp pressure in July 2025 after the Central Electricity Regulatory Commission approved a market-coupling framework that will unify prices across power exchanges. The move raised concerns that IEX could lose part of its pricing advantage and volume leadership, prompting a near-term correction.

While regulatory change introduces uncertainty, IEX’s early lead in technology, liquidity depth and green-market participation continues to support its franchise strength.

Going forward, the management aims to include new regulatory products like the Green Real-Time Market, Carbon Credit Certificates and Virtual Power Purchase Agreements, all of which could deepen liquidity and sustain double-digit volume growth.

It remains debt-free and expects only modest technology-linked capex, funded entirely through internal accruals.

The stock trades around 26 times earnings, a deep discount to its median PE of 42 times. With its commanding market share, digital infrastructure and early lead in emerging green-energy products, IEX remains a steady monopoly-style play for the 2026 watchlist.

Praj Industries Ltd

Praj Industries is a leading bioengineering company with expertise spanning biofuels, sustainable aviation fuel, compressed biogas and high-purity water systems. Its proprietary technology base and process know-how have made it India’s most trusted partner in the ethanol and green-fuels value chain.

For investors tracking monopoly-style opportunities, Praj remains the country’s dominant technology supplier in bioenergy, with over four decades of engineering leadership and a growing international footprint.

In FY25, revenue stood at ₹3,228 crore and operating margin was about 10%. The performance reflected execution delays in domestic ethanol projects and under-absorption of fixed costs at the GenX facility. In Q2 FY26, consolidated revenue rose 3% on-year and 31% sequentially, while Ebitda margin moderated to around 7%. The margin pressure was linked to muted ethanol demand after achieving the 20% blending target, and fixed-cost drag at GenX, which is yet to reach optimal utilization.

Management commentary points to improvement in the second half as customer-side liquidity normalises. The company expects traction from new areas such as diesel blending, sustainable aviation fuel and bioplastics, along with stronger international momentum under US IRA 45Z tax credits and projects in Latin America and Indonesia. Capex remains modest and fully funded through internal accruals.

Currently, Praj trades at about 58 times earnings, a premium to its five-year median of 45. With policy tailwinds in clean fuels and a proven technology edge, Praj Industries continues to rank among the most compelling monopoly-style plays for a 2026 watchlist.

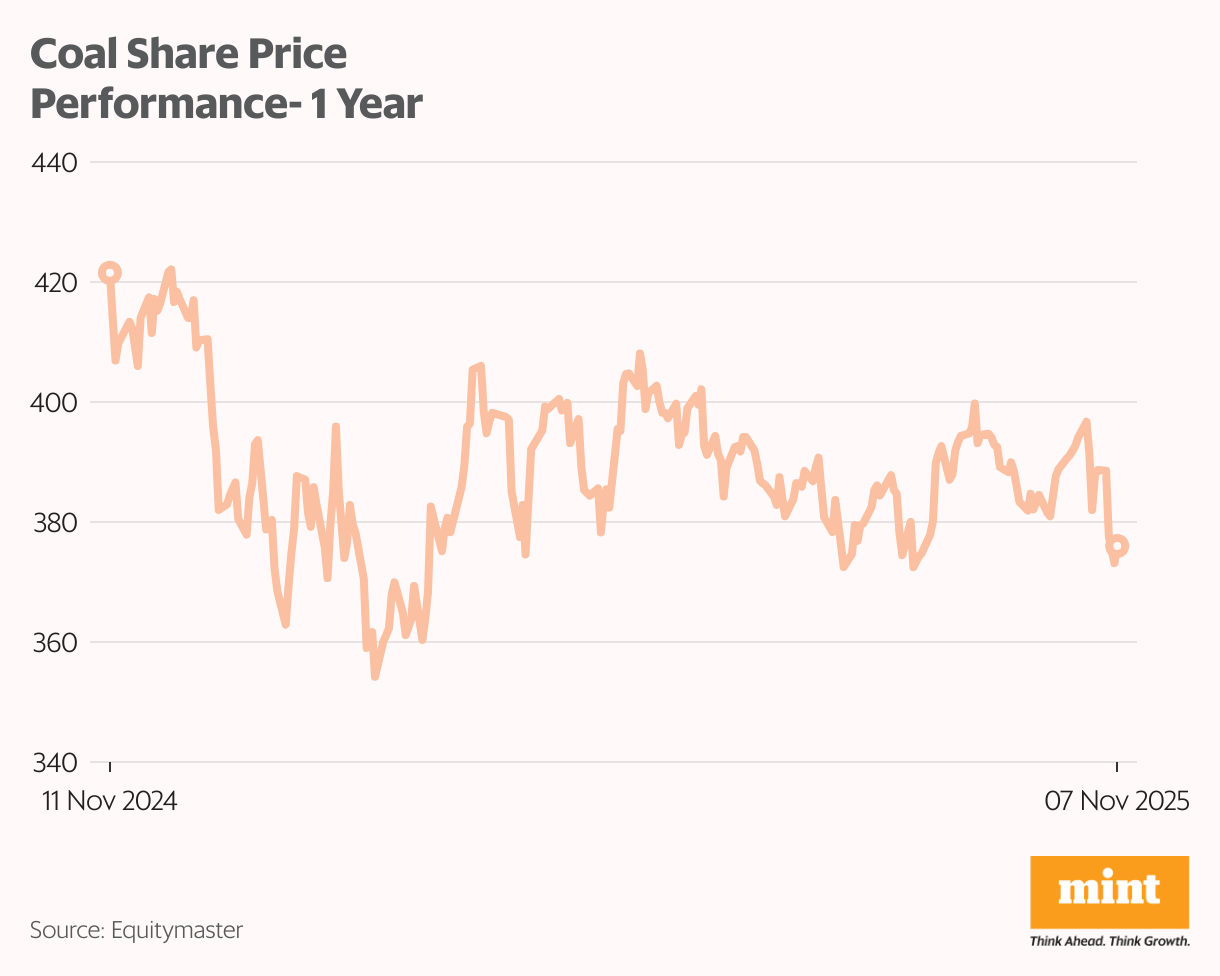

Coal India Ltd

Coal India is the world’s largest coal producer and the backbone of India’s energy supply chain. The company supplies more than four-fifths of the nation’s coal requirement, keeping power plants and heavy industries running. It has also begun diversifying into renewables and critical minerals to align with India’s long-term energy transition goals.

For investors tracking monopoly-style stocks, Coal India is among the rare few that combine dominance, strong cash flows and dividend visibility.

In FY25, Coal India reported revenue was stable year-on-year, with an operating margin of 33% driven by higher e-auction realizations and steady power-sector offtake. In Q2 FY26, revenue slipped around 3% and Ebitda margin moderated to 22% as extended monsoon conditions, lower e-auction prices and higher stripping-cost adjustments weighed on performance. The company remains net-cash positive with more than ₹40,000 crore in reserves and no debt.

Looking ahead, the company plans to spend ₹15,000-20,000 crore annually through FY28 to enhance output and efficiency. It expects production to rise around 3% each year as new MDO-based mines ramp up and washeries expand. Coal India is also investing in a 500MW solar venture and partnering with Hindustan Copper for critical minerals exploration. Funding for these projects is through internal accruals, with debt reserved for large coal-gasification initiatives.

Presently, the stock trades around 7.5 times earnings, a slight premium to its long-term median. With stable cash flows and a 6-7% dividend yield, Coal India remains a dependable, income-generating monopoly-style PSU for the 2026 watchlist.

Conclusion

Even in a volatile market, India’s monopoly-style franchises offer stability. These companies may not deliver flashy growth, but their steady cash flows, strong balance sheets and predictable dividends provide an anchor for long-term portfolios.

With capex visibility improving and most balance sheets debt-free, they remain relevant long-term plays. Valuations have rerated, but select dominant businesses still trade below intrinsic value. For investors, patience is key.

Monopolies may not sprint, but their consistency, earnings visibility and yield make them dependable wealth builders over time.

Happy Investing.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com