More than half of FY26 is out of the way, but for India’s information technology (IT) companies, revenue visibility remains murky. Investors are swinging between hope and despair, as a recovery in revenue growth gets delayed.

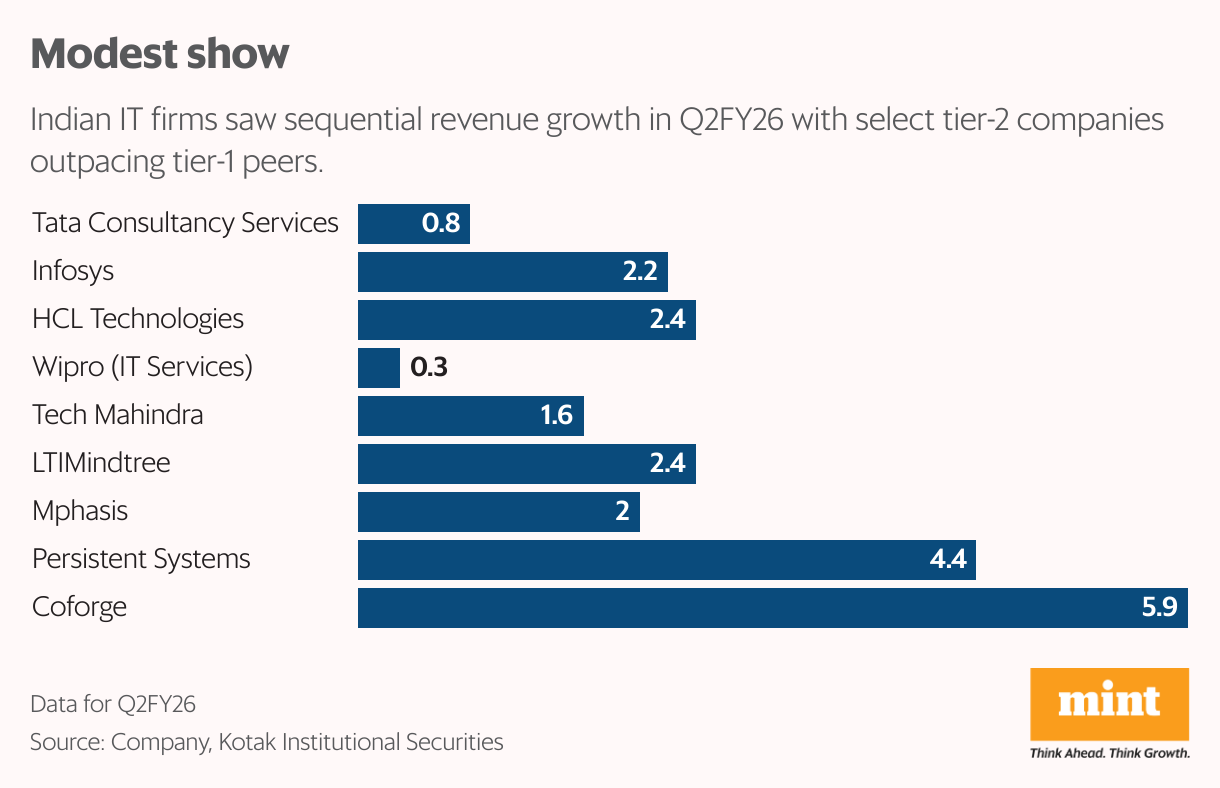

The September quarter (Q2) earnings saw modest sequential revenue growth for most tech firms and a selective recovery in key verticals. Out of 11 companies—five large-caps and six mid-caps—studied by BNP Paribas Securities (India), 64% reported revenue growth that was better than the lowered predictions made by analysts. This is an improvement from the 53% that exceeded expectations in the previous quarter.

On margin, 55% crossed expectations, against 13% last quarter. Infosys Ltd and HCL Technologies raised the lower end of their FY26 revenue growth guidance. As companies executed large deals won earlier, revenues flowed in.

Earnings before interest and tax (Ebit) margin got a push from favourable foreign currency movements (a falling rupee that translates into higher revenue) and cost-saving initiatives. To protect profitability, companies remain focused on cost containment measures, automation, and having fewer costly senior workers. Most IT companies have reduced reliance on H1-B visas, leading to increased investment in offshore offerings and aiding margin expansion.

Recovery in banking, financial services and insurance (BFSI) was a bright spot, while manufacturing and consumer businesses faced uncertainty due to tariffs. Leading IT companies had similar comments to make: clients still take longer to make spending decisions, as the demand environment remains largely unchanged over the last quarter.

Stuck in first gear

On deal wins, companies had a healthy quarter, led by cost takeout deals—contracts where a client wants to permanently cut expenses—as well as AI-led solution projects. On an aggregate basis (excluding small-cap IT), 11 IT companies saw an impressive 25% year-on-year growth in total contract value of deal wins, showed data by Nuvama Research.

However, large cost take-out deals come with low margins; so, companies need a recovery in discretionary spending or further rupee depreciation to offset this risk. Also, competition has increased. According to Kotak Institutional Equities, the number of available cost take-out deals is insufficient to meet everyone’s growth aspirations in the current environment. This may lead to irrational pricing and higher execution risks.

A key highlight was the increased thrust on AI investments by large IT companies. Tata Consultancy Services announced its entry into the sovereign data centre space with an initial 1GW capacity, and HCL Tech disclosed its ‘Advanced AI’ revenue. Some others are enhancing their AI-driven solutions to strengthen their service offerings and bag new deals.

The ongoing December quarter (Q3) is typically slow for IT companies, because employees take holidays (furloughs) and there are fewer working days overall. Many IT company managements expect the impact of furloughs on revenue growth to be similar to the previous year. The impact of wage hikes on the margins of select technology companies will be monitored. In short, Q3 is likely to be a dull quarter.

A swift deterioration in the global macro-economic scenario due to tariff-led uncertainties since the beginning of calendar year 2025 led to earnings downgrades for the sector. This has kept stocks under pressure and valuations cooling off. The Nifty IT index is down 16% in 2025 so far, versus positive returns by the benchmark Nifty50. Kotak is pencilling in 4.6-5.3% revenue growth for top three tier-1 IT companies in FY27, lower than normalized growth. It cautions that another weak year in FY27 could cement the perception, however inaccurate, that IT services face structural headwinds.

{kind=link}