Most of these were offer-for-sale issues, where existing investors pared their holdings. Only a handful came with fresh issuances aimed at funding expansion, reducing debt, and future growth.

Among the companies that went public recently, Belrise Industries drew interest after raising ₹2,150 crore in May. A major portion of the proceeds ( ₹1,618 crore) was earmarked for repaying debt, signalling a balance-sheet reset as it entered the listed space.

The stock was listed at ₹100, a 11.1% premium to its IPO price of ₹90 on 28 May 2025, and has since increased by 60% to ₹160.

The rise has been supported by its valuation gap compared to peers, ongoing capacity expansion, and the company’s guidance to double revenue by FY27.

Higher content-per-vehicle and strong financial growth have also shaped the sentiment. But, even after the recent move, Belrise continues to trade at a discount to peers, which keeps the debate open on whether the stock still offers room for further re-rating.

To gain a better understanding, let’s examine Belrise’s business model, financial performance, and how its valuation compares to that of its competitors, such as Minda Corp., Uno Minda and Endurance Tech.

A powertrain agnostic business model

Belrise manufactures safety-critical systems and engineering solutions for two-wheelers (2W), three-wheelers (3W), four-wheelers (4W), as well as commercial and agricultural vehicles.

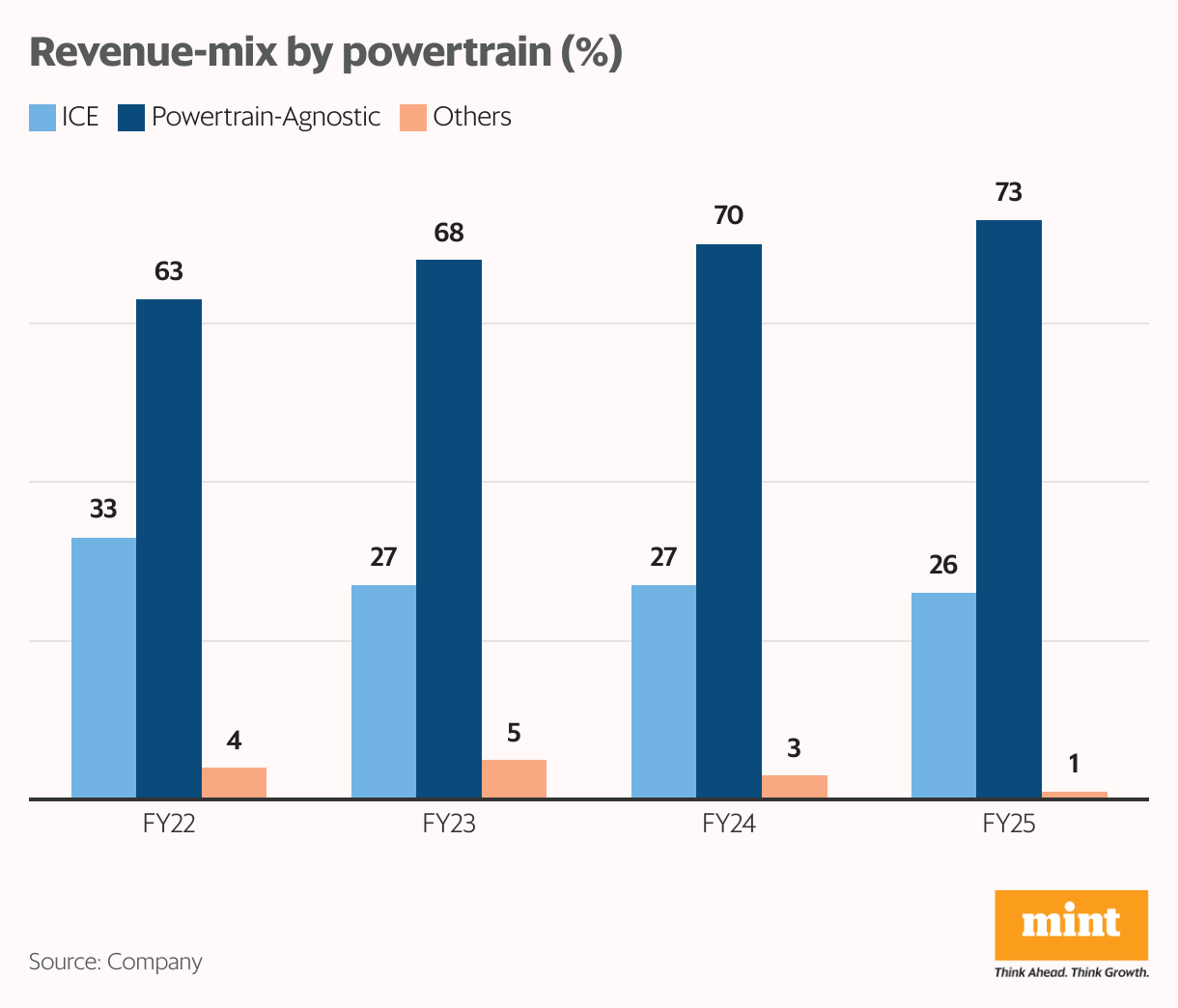

Its products are suitable for both electric and internal combustion engine (ICE) vehicles, and this flexibility positions the company favorably to adapt to shifts in the industry.

Belrise operates through two main business areas: manufacturing, which contributed 79.5% of revenue (as of FY25), and a non-core trading business that accounted for the remaining 20.5%.

The manufacturing segment is further categorised into four verticals, with the sheet metal division (covering chassis and exhaust systems) remaining the dominant contributor, accounting for 75.5% of revenue.

Belrise’s market leadership in precision sheet-metal automotive components, backed by a 24% revenue share in India’s 2W metal components segment, remains a core competitive strength. With its market leadership, the company is well-positioned in the 2W metal products market, which is projected to grow at a CAGR of 11-13% over the next five years, until FY30.

The other divisions, including the plastic and polymer segment (2.5%), suspension (0.5%), and e-mobility components such as motors and chargers, remain relatively small contributors.

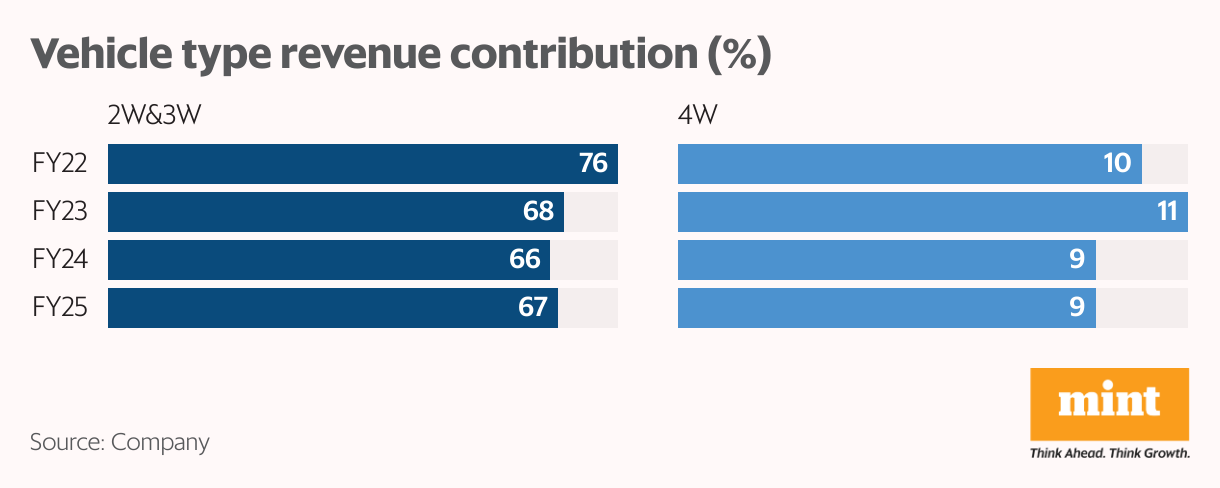

In FY25, 2W and 3W (combined) were the largest revenue drivers, accounting for 67% of revenue, followed by 4W commercial (6%) and passenger vehicles (3%), among others. Belrise serves over 31 global original equipment manufacturers (OEMs), supported by long-standing relationships built over the years.

Its key OEM partners include Bajaj Auto (15 years), Honda Motorcycle (12 years), Royal Enfield (14 years), Hero Motocorp (6 years), Tata Motors, and Jaguar Land Rover. However, the business remains concentrated, with the top 10 clients accounting for 63.8% of revenue as of December 2024. Updated figures are not yet available.

How is Belrise planning its next phase of growth?

That said, the company aims to gradually ease this concentration by strengthening its presence in the 4W segment. To support this diversification, Belrise plans to double its revenue from the 4W segments over the next two and a half years. This would help diversify the company’s revenue mix, both by vehicle category and by customer exposure.

As part of its diversification strategy, Belrise acquired H-One in 2024, a subsidiary of a Japanese listed company. H-One specialises in high-tensile steel fabrication, stamping, and complex tool design. The acquisition directly supports Belrise’s 4W expansion by adding three new Japanese 4W OEMs and deepening its penetration with two existing 2W OEMs.

Belrise plans to utilise H-One to expand its presence among Japanese OEMs. The addition has already increased the 4W content per vehicle by 60% to around ₹15,000, and plans to scale to ₹45,000. Revenue from H-One stood at ₹60 crore in Q2 FY26, and management believes this can scale to about ₹450 crore over the next two years without major capex.

Rising content per vehicle and premiumisation

Belrise also aims to improve the 2W content per vehicle from ₹12,500 currently to ₹17,300 per vehicle over the next 18–24 months. The introduction of new components, such as steering columns ( ₹1,500 per vehicle), filters ( ₹800), and brakes ( ₹2,500), will support this expansion.

Belrise is also set to benefit from the rising share of premium motorcycles. The management said a premium 2W chassis carries a kit value of almost ₹5,500, nearly twice that of an economy model ( ₹2,500). This trend, supported by in-house products such as filters, brakes, and new steering columns, is expected to help the company enhance kit value and profitability.

At the same time, Belrise is moving up the value chain from a Tier-1 component supplier to a Tier-0.5 supplier, focusing more on sub-systems and full-system assemblies. This transition enables the company to become part of the customer’s development cycle, thereby increasing both business stickiness and content value per vehicle.

Diversification into defence and renewables

Beyond the automotive sector, Belrise has leveraged its engineering expertise to expand into adjacent industries, including defence and renewables. It has begun supplying solar structures to a global solar tracker manufacturer, with initial orders for North America and discussions underway for India and Europe. In the defence and aerospace vertical, it has secured additional orders for an Indian Defence OEM’s armoured vehicle programme, marking indirect exports.

To meet rising demand, Belrise plans to invest ₹800 crore over the next two years, of which ₹260 crore has already been deployed in the first half of FY26. Several new facilities have come online or are nearing production start. A plant in Chennai began operations in Q1 FY26, while facilities in Pune and Bhiwadi went live in Q2 FY26.

Another plant in Chennai is expected to start production in Q3 FY26. This Chennai facility is dedicated to supplying chassis systems and BIW parts for an EV platform of a leading 2W OEM. In addition, the company has secured multiple new orders from OEMs, which are expected to accelerate revenue growth.

What the Numbers Say About Belrise

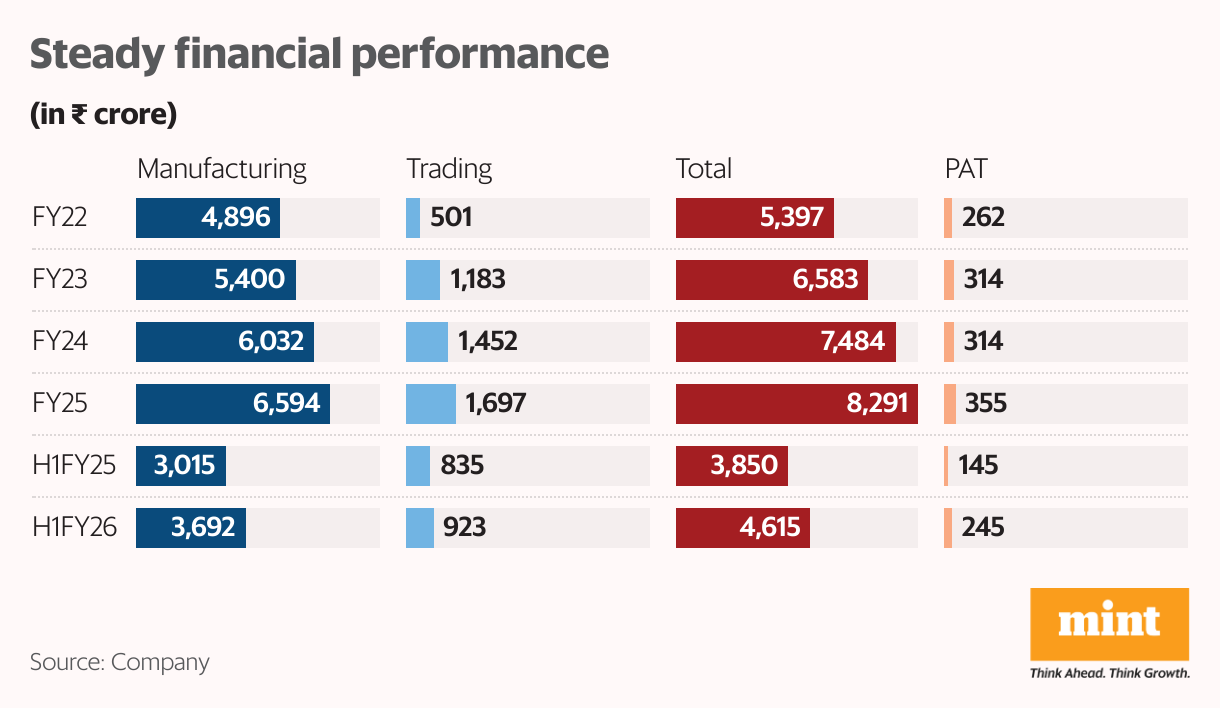

Belrise’s revenue has grown at a CAGR of 15% over the last three years, rising from ₹5,397 crore in FY22 to ₹8,291 crore in FY25. Within this, manufacturing revenue increased at a slower 10% CAGR to ₹6,594 crore, while the trading business grew much faster at a 50% CAGR, reaching ₹1,697 crore in FY25.

The momentum continued in the first half of FY26. Revenue increased 20% year-on-year to ₹4,615 crore, supported by a 22% rise in manufacturing revenue and an 11% increase in trading. Within the mix, ICE revenue grew 16%, powertrain (+17%), and by vehicle category, 2W+3W revenue rose 12%, 4W passenger (+26%), and 4W commercial (+34%).

Brokerage Sunidhi Securities noted that the company delivered a performance that exceeded expectations.

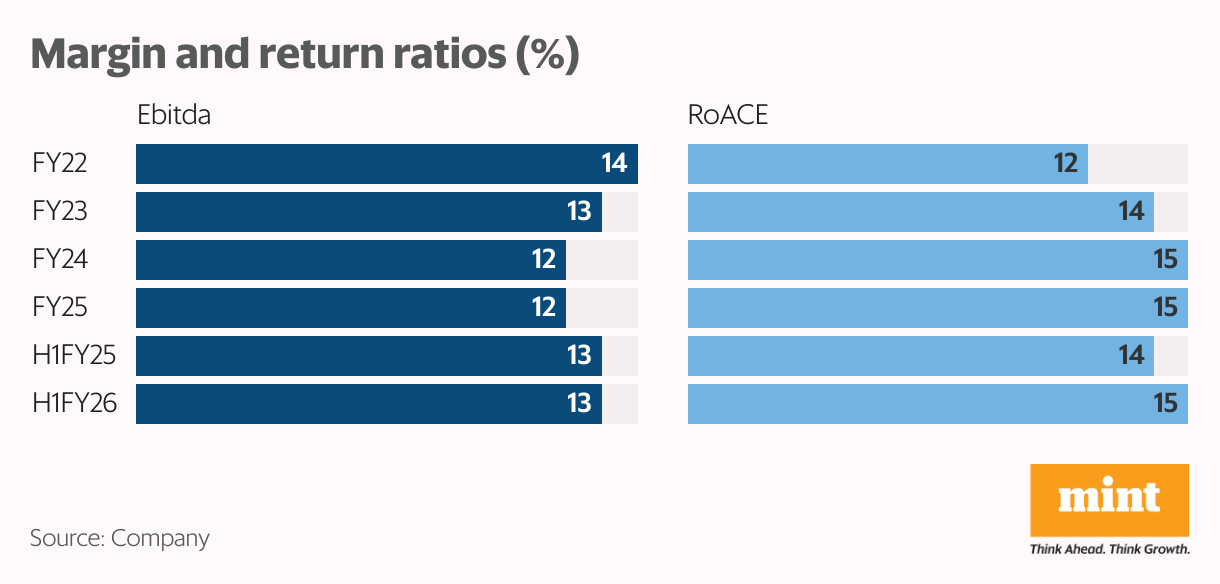

The company’s Ebitda margin stands around 12-13% (comparable to peers), primarily due to the underutilization of new capacity and a lower 6% margin in the trading business. Management is evaluating whether to hive off this non-core segment to support a margin recovery. In line with revenue trends, profit after tax grew at an 11% CAGR, reaching ₹355 crore in FY25, and the same surged by 69% year-on-year to ₹245 crore in H1 FY26, helped by a 25% reduction in interest costs to ₹95 crore.

Return ratios remain healthy, with a return on average capital employed of 15% and a return on average equity of 14%. The net debt-to-equity ratio inched up to 1x, although the company has since reduced this by repaying part of its borrowings using proceeds from the IPO.

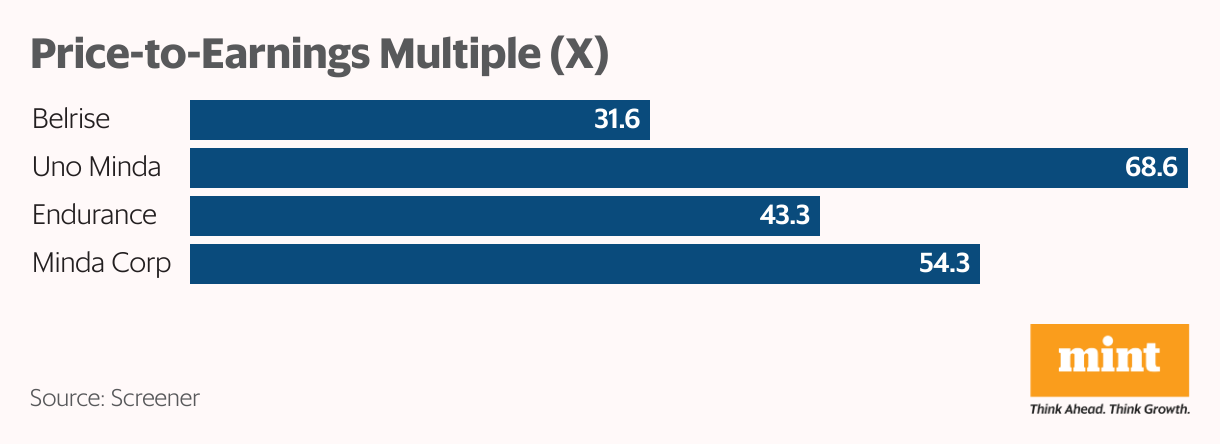

Can Belrise close the valuation discount?

At ₹161 per share, Belrise is trading at a price-to-earnings multiple of 31.6 times, which is a discount to its peers: Uno Minda (68.6), Endurance Tech (43.3), and Minda Corp (54.3).

Belrise appears positioned to sustain its growth momentum driven by rising content per vehicle, a gradual shift toward premiumization, and its entry into the defence and 4W verticals, as per brokerage Phillip Capital.

Other brokerages share a positive view on the company, with Investec valuing it at ₹185, LKP Research at ₹192, and Sunidhi Securities at ₹197.

Profitability, too, is likely to improve at a quicker pace as the mix evolves and operating leverage kicks in. If these trends materialise as anticipated, return ratios are expected to strengthen, and the valuation discount to peers is likely to narrow over time.

Sector slowdown, failure to diversify customer concentration, including execution delays, are key risks to watch.

For more such analysis read Profit Pulse

Madhvendra has over seven years of experience in equity markets and writes detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

{kind=link}