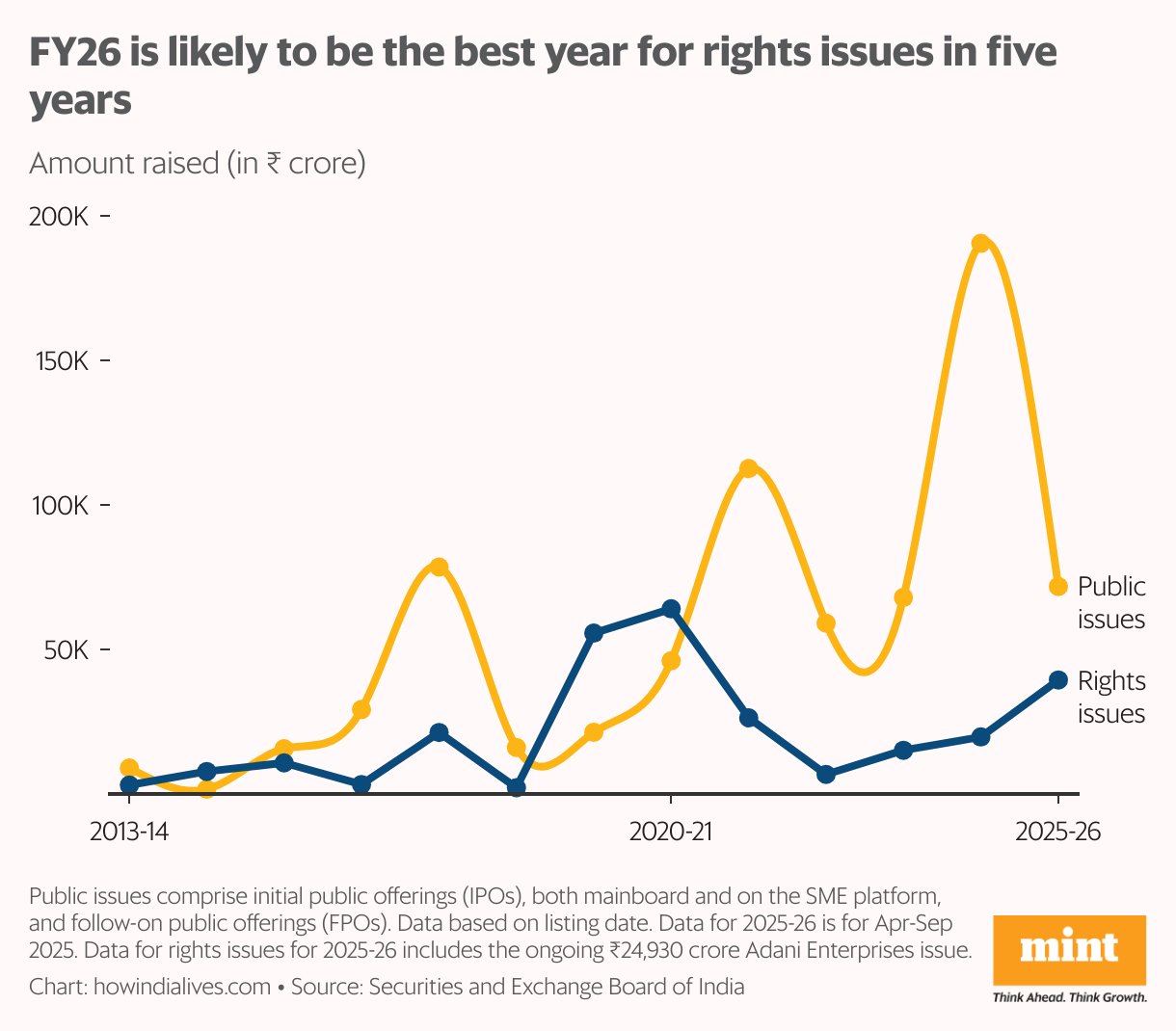

If fully subscribed, the issue’s collections will go a long way in making 2025-26 one of the most prolific years in recent memory for rights issues. Even without the Adani issue, the segment has been doing reasonably well this year. But in comparison to fundraising through the primary market, it remains a less popular route.

Right to buy

A rights issue is a method companies use to raise additional capital by offering new shares exclusively to its existing shareholders. These shares are typically issued at a price below the current market price, giving shareholders a chance to acquire additional shares at a discount to the market price. A rights issue also enables promoters them to maintain their ownership share. It also generates cash for the business, which can be used to fund expansion, repay loans, or strengthen its cash position.

According to data from the capital market regulator, excluding the Adani issue, total collections from rights issues for the six months to September 2025 stood at ₹14,509 crore. This amount stood at ₹19,712 crore for all of 2024-25. The Adani issue, if fully subscribed, would take 2025-26 collections to ₹39,439 crore, matching the highs of 2019-20 and 2020-21.

Broad-based market

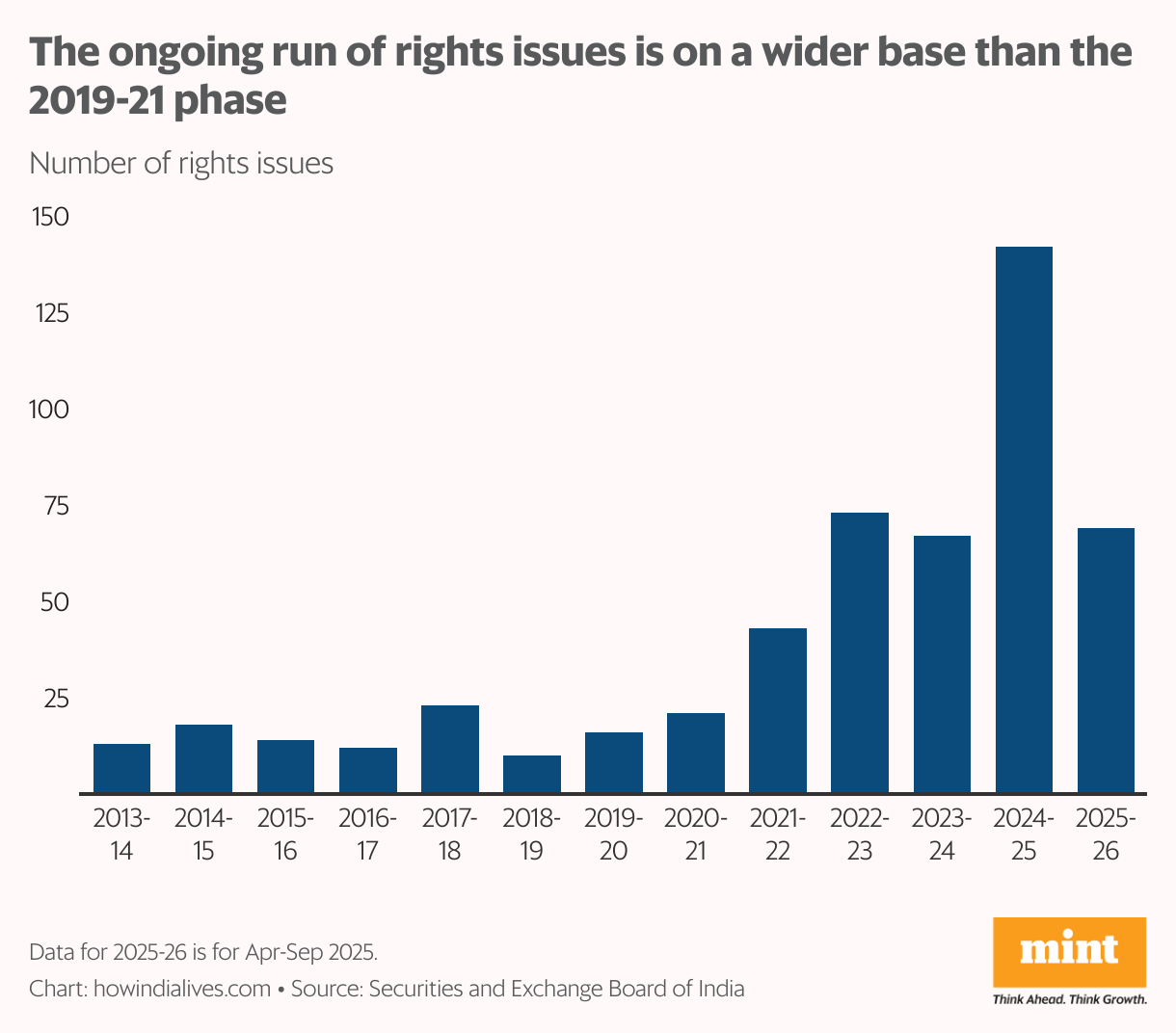

The large collections in 2019-20 and 2020-21 were heavily concentrated among a few companies. In 2019-20, just three companies accounted for 95% of the ₹55,642 crore collected via rights issues. These were telecom majors Vodafone ( ₹25,000 crore) and Bharti Airtel ( ₹24,372 crore), and Piramal Enterprises ( ₹3,430 crore). In 2020-21, four companies accounted for 92% of the ₹64,059 crore collected, with Reliance Industries alone accounting for 83%.

In that sense, in keeping with sentiment in the primary market, the rights issue space has been more broad-based over the past four financial years, with more listed companies taking this route. In 2024-25, 142 companies closed a rights issue, which is 15 more than the sum total for the eight years from 2013-14 to 2020-21. In the first half of the ongoing financial year, 69 companies conducted a rights issue. If the market holds and doesn’t turn skittish, chances are this number will increase.

Fully subscribed

This relatively brisk period of activity in the rights issue space has coincided with a pronounced spurt in initial public offerings (IPOs)—shares offered by companies to the public for the first time — including those of internet businesses such as Urban Company and Lenskart. That rights issues have managed to hold up well is a testament to the liquidity and investor interest on one hand and companies acting on a need and opportunity on the other.

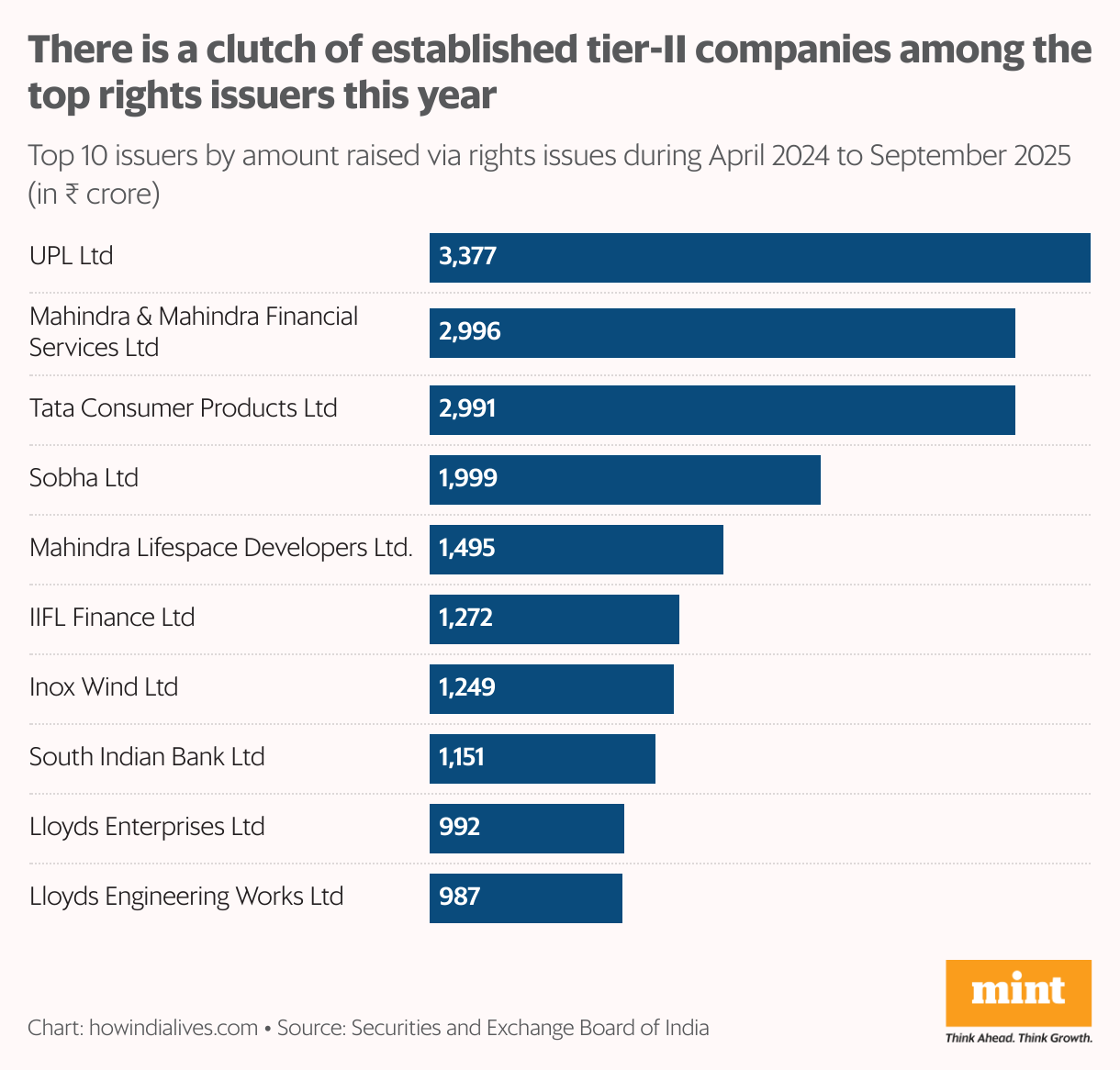

In the 18 months from April 2024 and September 2025, the amounts raised by the 211 companies via rights issues ranged from ₹1.16 crore to ₹3,377 crore. Only 23 of these companies raised less than ₹10 crore, and only 21 did not see their rights issue fully subscribed. The top 10 issuers by money raised included two companies from the Mahindra Group and one from the Tata stable. Each of these 10 issues was oversubscribed.

Time to market

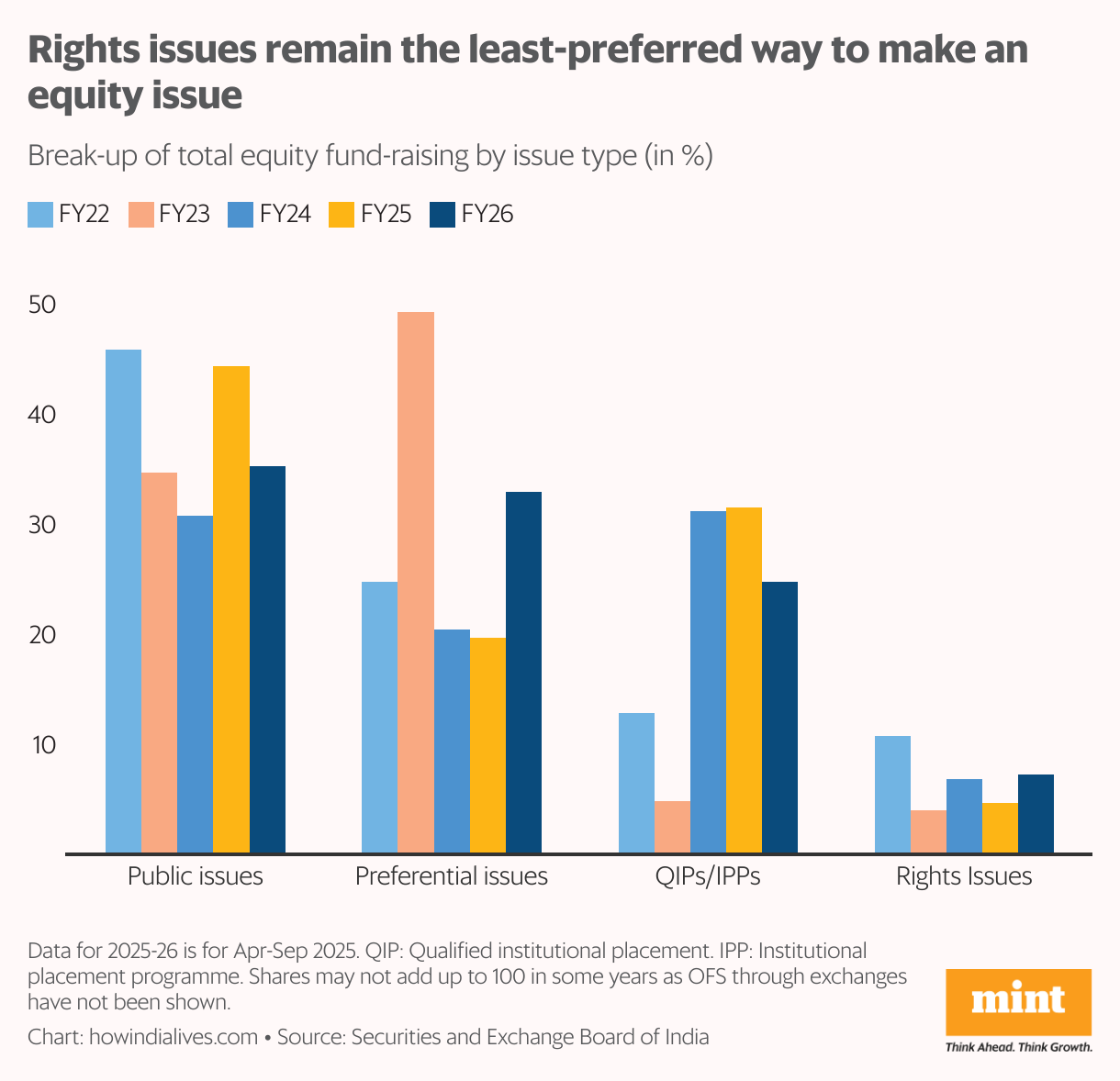

Despite the surge in recent years, rights issues remain the least popular way for companies to raise equity capital. In four of the past five years, the share of rights issues did not even crossed 10%. One reason is the logistics involved, with all shareholders of a company participating. Preferential allotments to promoters themselves, or a small group of investors via a qualified institutional placement (QIP) are typically faster.

The Securities and Exchange Board of India (Sebi) has been working to change that. For example, it revised a set of rules in March that would speed up rights issues from 4-6 months to 23 working days. Key changes included eliminating the draft filing with Sebi (going via stock exchanges instead), relaxing the minimum subscription requirement to 75% (from 90% under certain conditions), and allotting unsubscribed shares to select investors.

Market murmurs

On paper, a shorter time frame should make promoters who don’t wish to dilute their stakes take the rights issue route to raise more capital. Alternatives such as a QIP to external investors would dilute promoters’ shareholding, while a preferential issue to themselves would require them to bring in the entire capital. A rights issue offers a middle ground, allowing promoters to contain their capital contribution while maintaining their shareholding.

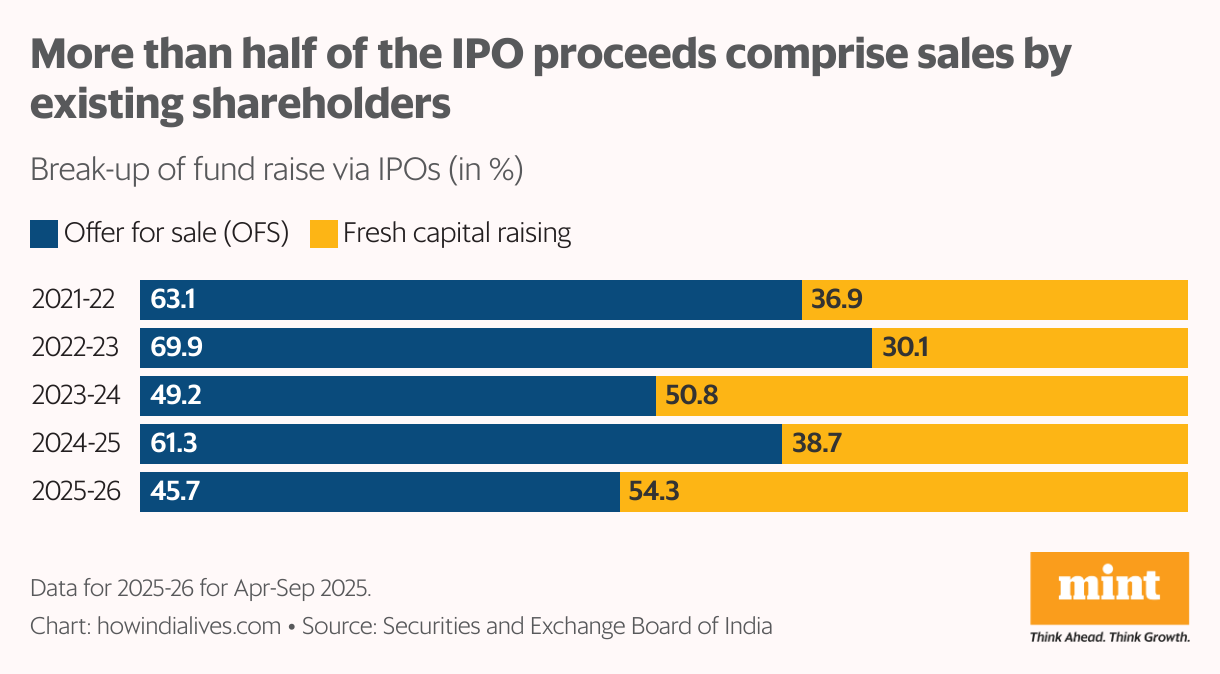

Looking ahead, market sentiment will play a crucial role in fundraising. Amid high valuations, there are murmurs of the market unravelling, triggered by a correction in companies driving the spending frenzy in artificial intelligence (AI). There are other signs, too. In the past five years, more than half of IPO proceeds have not gone into companies but to promoters and investors selling via the offer for sale (OFS). It’s partly about promoters and investors cashing in, but is also a sign of stretched valuations.

www.howindialives.com is a database and search engine for public data

{kind=link}