Ambuja Cements Ltd is chasing both volume growth and operational efficiencies. It now plans to scale cement capacity from around 97 million tonnes per annum (mtpa) in FY25 to nearly 155mtpa by FY28, versus the earlier target of 140 mtpa.

The incremental capacity of 15 mtpa will be achieved through debottlenecking at existing plants at a lower capital expenditure of $48/tonne.

Ambuja’s capacity addition target implies a 17% compound annual growth rate (CAGR) in capacity over FY25-FY28. However, ramping up this target would remain challenging in the backdrop of potential cement demand CAGR of 7-7.5% during the same time, and existing low utilization level of around 64%, said a DAM Capital report.

As rival UltraTech Cement Ltd goes full throttle in adding new capacities, Ambuja’s move to defend its market share is understandable. But, given the industry’s demand-supply dynamics and weak pricing trends, a concern is whether Ambuja can achieve this ambitious plan without compromising on its profitability.

Q2 performance

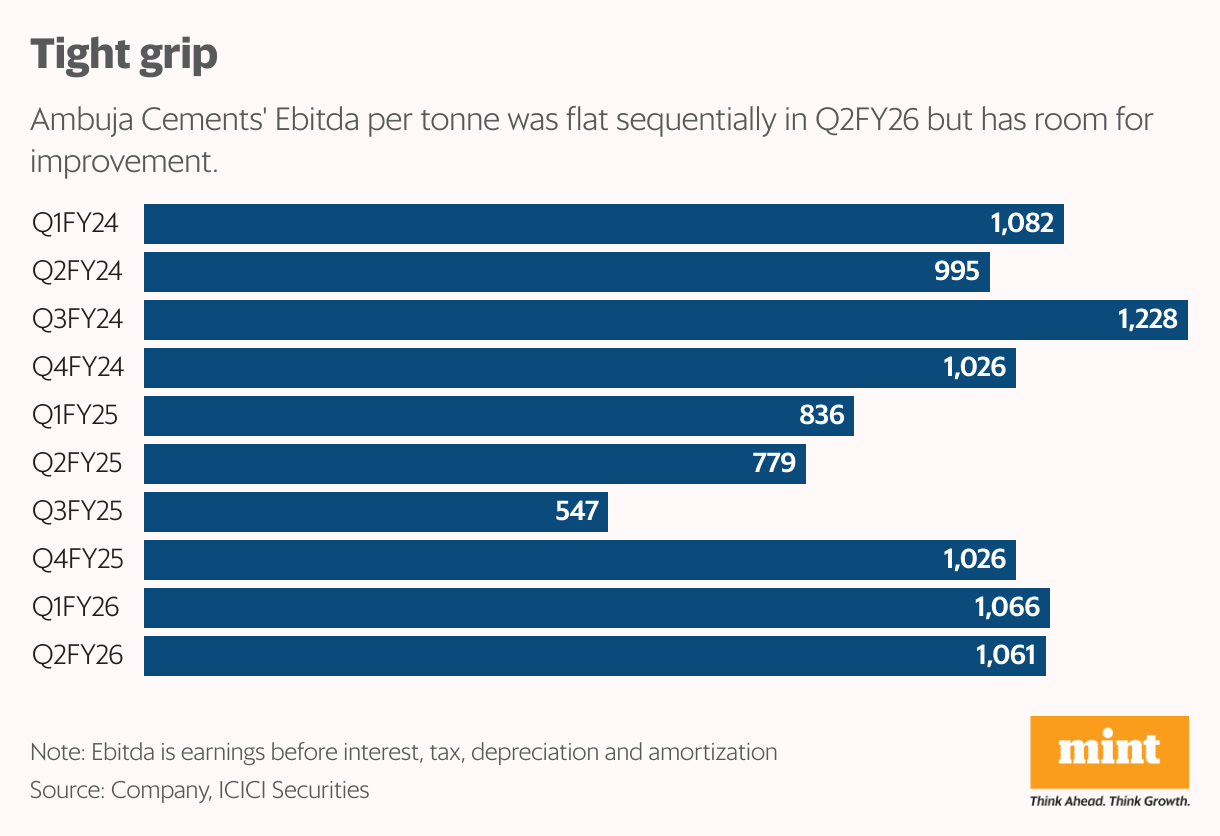

Ambuja’s Ebitda per tonne in the September quarter (Q2FY26) at ₹1,061 was flat sequentially versus a 20-25% drop reported by cement majors, according to an ICICI Securities’ 4 November report. Cost optimization and favourable product mix are expected to drive a further improvement in Ebitda per tonne, Ambuja eyes at ₹1,450- ₹1,500 by FY28. Ebitda stands for earnings before interest, taxes, depreciation and amortization.

Ambuja’s organic volume (excluding recently acquired Penna Industries, Sanghi Industries, and Orient Cement) rose 11% year-on-year in Q2FY26, ahead of the industry. The management is confident of sustaining double-digit volume growth in FY26 versus the industry’s estimated growth of 7-8%. Ambuja’s market share increased by 100 basis points on-year to 16.6% as of Q2, and it targets 20-22% by FY28 through capacity expansions and increased branding.

Cost-cutting goal

It has also outlined a multi-year cost reduction roadmap from the operating cost of ₹4,200 per tonne currently to ₹4,000 by FY26, ₹3,800 by FY27, and ₹3,650 by FY28. Ongoing cost-saving initiatives and synergies benefits have helped lower total operating cost, and further reduction is likely through optimized fuel mix, higher green power use, and logistics gains.

Renewable capacity is expected to reach 900mw/1,122mw by the end of FY26/FY27 from 673mw now. The share of green power would reach 60% by FY28 from the existing 33%, which will help reduce power costs.

Ambuja’s shares are up 7% so far in 2025 and trade at 15 times EV/Ebitda based on FY27 estimates, showed Bloomberg data. Timely execution of capacity addition plans and smooth integration of acquired units are critical for re-rating.

{kind=link}