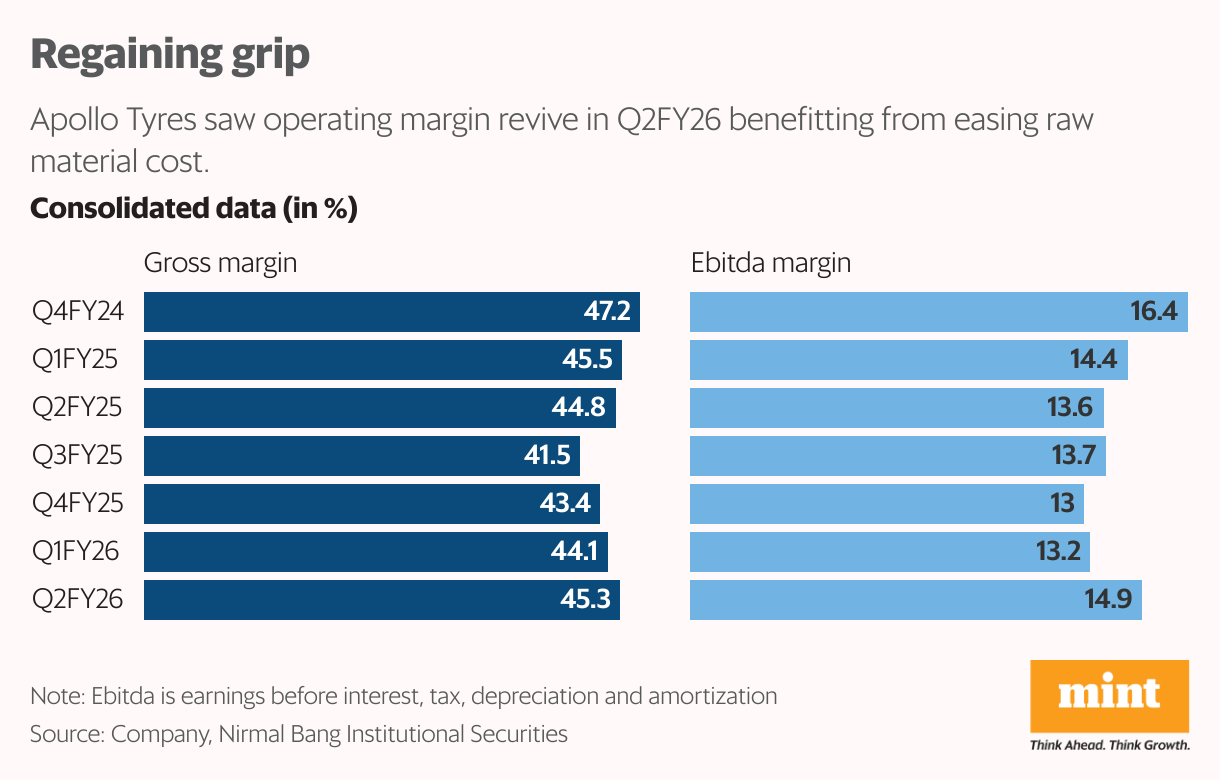

Apollo Tyres Ltd saw a higher-than-anticipated improvement in profitability in the September quarter (Q2FY26), buoyed by easing raw material costs.

Consolidated Ebitda margin expanded 90 basis points (bps) sequentially, led by 170 bps sequential gross margin increase to 14.9%. It exceeded the consensus estimate of 14% on this metric.

On a sequential basis, raw material cost declined 3% in Q2FY26. Benefits from lower input costs are likely in Q3FY26 as the company expects these costs to remain stable or even move slightly lower.

Benign raw material cost, an improving mix towards replacement and exports and closure of Enschede plant in Netherlands by June 2026 should unlock structural cost benefits. All these together should brighten Apollo Tyres’ profitability prospects.

In India, volumes were up 4%, with original equipment manufacture (OEM) and replacement segments up 4% and 2%, respectively. Agriculture, two-wheelers, and three-wheelers product categories saw healthy growth.

Export volumes rose by double-digits in Q2FY26. Volume growth is likely to be supported by a strong export recovery and balanced growth in both replacement and OEM channels.

Replacement segment is poised to record mid-to-high single-digit volume growth in H2FY26. Demand from original equipment manufacturers (OEM) is seen picking up from commercial vehicles compared to passenger vehicles, the management said.

However, Nomura Global Markets Research cautions that commercial vehicles replacement demand recovery, which is around 55% of Apollo’s standalone revenue, remains slow.

This could keep volume and revenue growth modest. “We maintain around 6% India volume growth over FY27-28F, driving around 6% revenue CAGR over FY25-28F,” added the Nomura report dated 16 November. European demand remains muted, but it is better than the previous two quarters, the management said. It expects growth to come back, though could be limited to low single digit.

Intense competition

Trouble is also brewing elsewhere. With Balkrishna Industries Ltd’s entry into Apollo’s key segments of TBR (truck, bus, radial) and mid-premium PCR (passenger car radial), competitive pressure is seen intensifying in FY27/FY28. This could lead to higher discounting and marketing spends by the industry, thus putting pressure on the margins.

“We have accordingly cut our volume and profitability estimates for standalone operations for FY28, leading to an 11.5% EPS cut,” said HDFC Securities in a report dated 17 November.

In calendar 2025 so far, the stock has declined around 4% versus positive returns by the Nifty Midcap 50 index. It trades at FY27 price-to-earnings multiple of 15x, which is reasonable, but unattractive.

{kind=link}