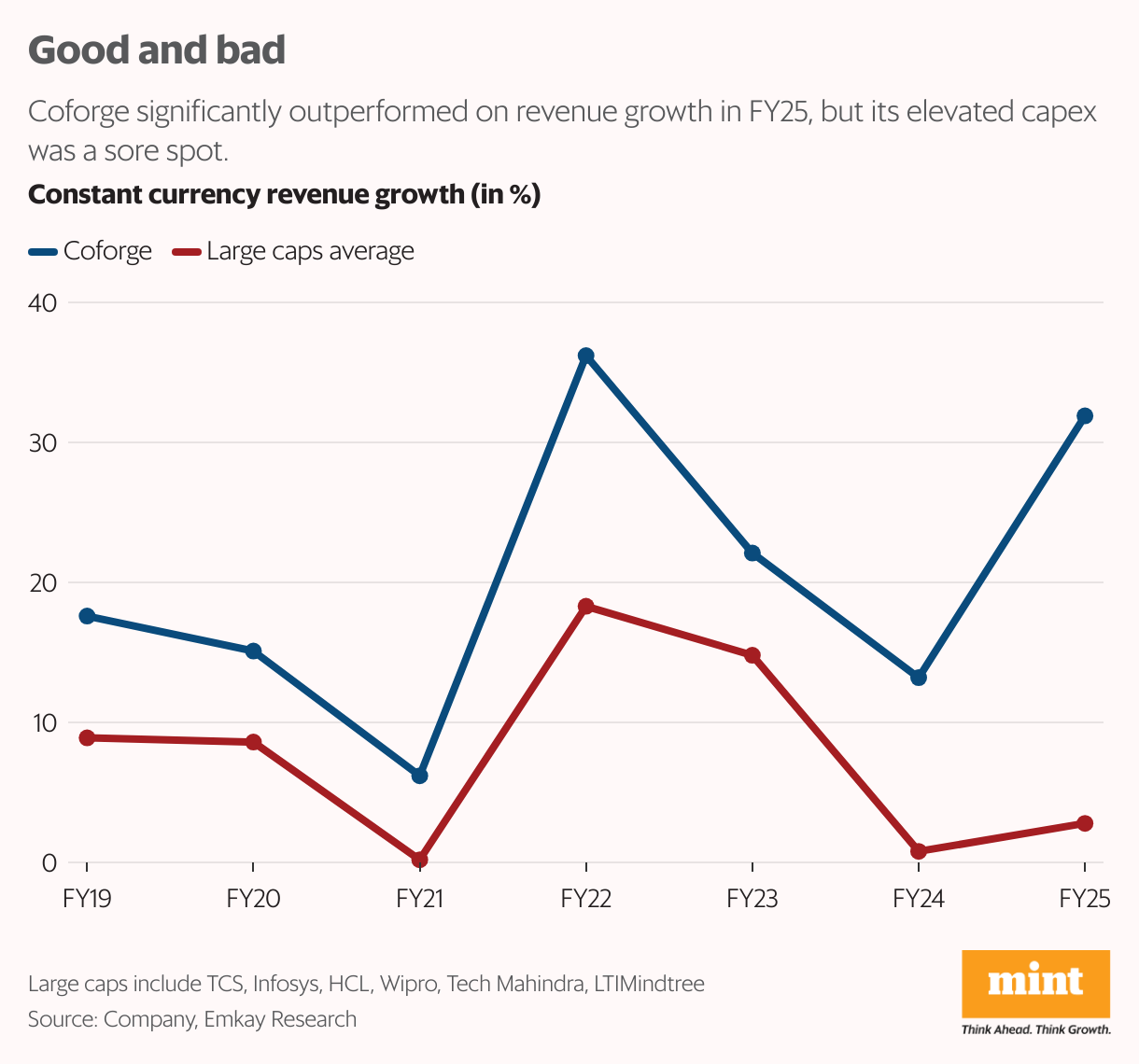

Coforge Ltd’s shares have now recouped a large part of their losses seen after its June quarter (Q1FY26) results were announced, when the stock had tanked 9.4% in a single day. Investor concerns were mainly pertaining to the company’s heavy capex and profitability falling short of expectations, even as revenue growth was splendid at 8% sequentially in constant currency (CC) terms.

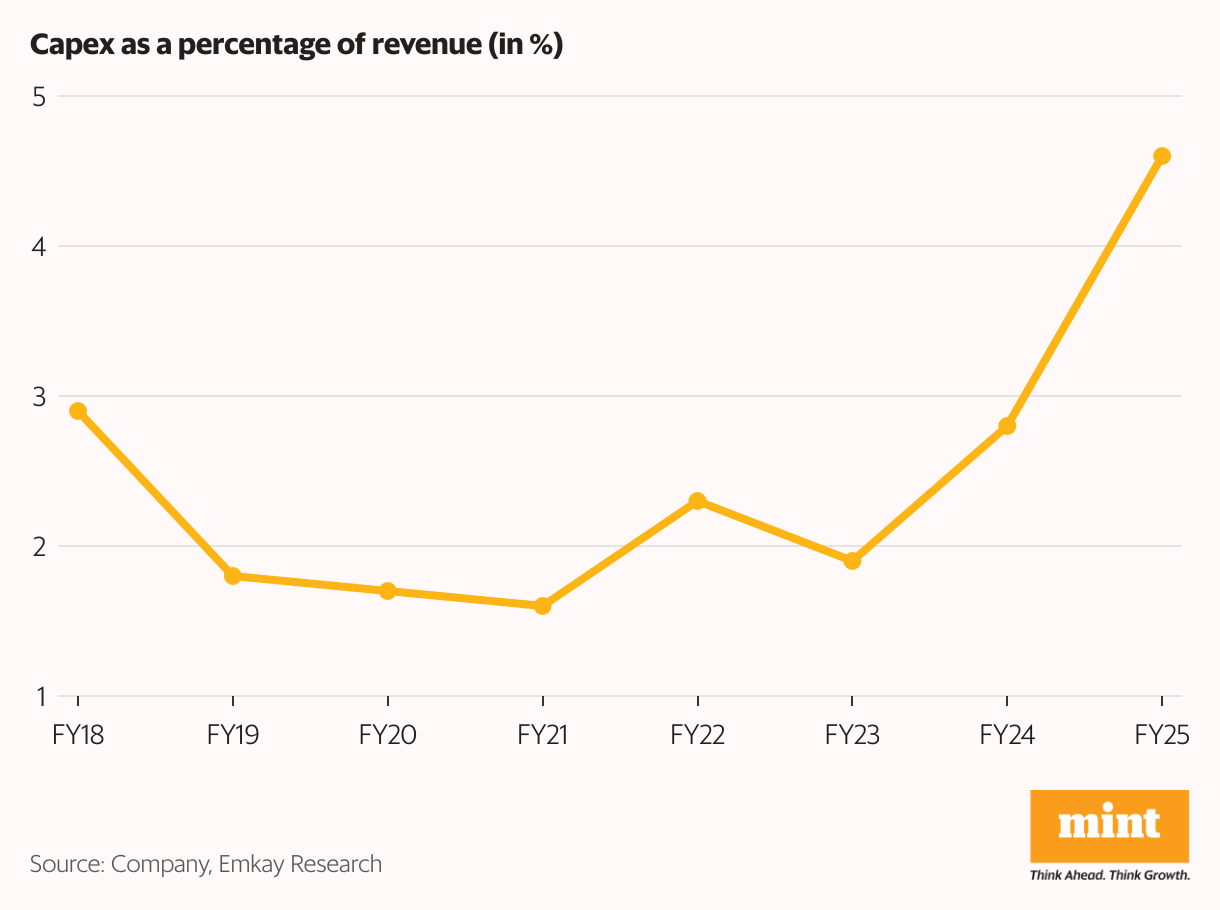

Notably, the mid-sized information technology (IT) company clocked an enviable 32% year-on-year CC revenue growth in FY25, aided by acquisitions; organic revenue growth was strong at about 15%. At the same time, FY25 capex surged 114% year-on-year to ₹557 crore. Capex as a percentage of revenue was 4.6% in FY25 versus 1.7% in FY20. The increase in capex can be largely attributed to the Cigniti acquisition and investment in a data centre for a client. Q1FY26 capex was high too, but is expected to taper ahead.

Some argue that worries about Coforge’s capex and cashflow profile are overdone. For perspective, “While headline FCF/PAT looks volatile, dipping to negative territory in FY25, the distortions are largely attributable to inorganic investments and elevated data-centre capex rather than structural weakness in operations,” said Emkay Global Financial Services analysts in a 16 September report. “Stripping these out, the company’s FCF conversion has been consistently healthy, sustaining in the 80-115% range, a level that reflects disciplined cash management even during the expansion phase,” added the report. FCF is free cash flow; PAT is profit after tax.

Read more: TTK Prestige singed by competitive heat, eyes comeback through strategic bets

Coforge’s FY25 was also remarkable as it signed a 13-year deal valued at $1.56 billion with a leading US-based travel technology firm, Sabre Technologies. The other notable event in FY25 is that Coforge has integrated the Cigniti Technologies business operationally from Q2FY25.

Strategic deals

In its latest annual report, Coforge points out, between FY17 and FY25, the company has moved from being the eighteenth largest Indian IT services firm to the eighth largest. Coforge believes three key factors have helped it over the past eight years to build a strong differentiation: execution intensity, hyper-specialization in select industries and deep engineering capabilities.

Coforge is aiming for its Ebit (earnings before interest and tax) margin to reach about 14% for FY26, aided by drivers such as lower Esop-related expenses, sustained revenue growth momentum and absence of one-offs. Q1FY26 Ebit margin came in at 13.2%, missing estimates and flat sequentially, primarily due to higher amortization of intangibles from recent acquisitions, higher depreciation related to the AI-powered data centre deal, large deal ramp-up and visa costs.

After signing 14 large deals in FY25, it aims to close at least 20 large deals in the current financial year. Five large deals were signed in Q1FY26. Coforge’s executable order book, which reflects the total value of locked orders over the next 12 months, stood at $1.55 billion at Q1-end, up 47% year-on-year.

Read more: How KRBL’s mistakes are helping LT Foods win the race

To be sure, Coforge’s growth outlook is promising, but some worries remain. “While the Sabre deal was one of the largest contracts won across the industry, it carries risks as Sabre is going through a tough operating and financial phase,” said HSBC Securities and Capital Markets (India). “Consensus expectations, in our view, do not factor in the execution risk in large deals and the integration risk of Cigniti, implying downside risk to the company’s FY26-27 estimated margins,” said HSBC.

Coforge’s stock trades at 34 times FY27 estimated earnings, as per Bloomberg. Valuations could find support if the company’s growth momentum continues and it delivers on margin.

Key Takeaways

- Coforge posted 32% constant currency revenue growth in FY25, with 15% organic growth.

- Capex rose 114% YoY to ₹557 crore, driven by acquisitions and infrastructure.

- Q1FY26 Ebit margin missed estimates at 13.2%, flat sequentially.

- Sabre deal and Cigniti acquisition add scale but introduce execution risks.

- Stock trades at 34x FY27 earnings; margin delivery is key to sustaining valuation.

{kind=link}