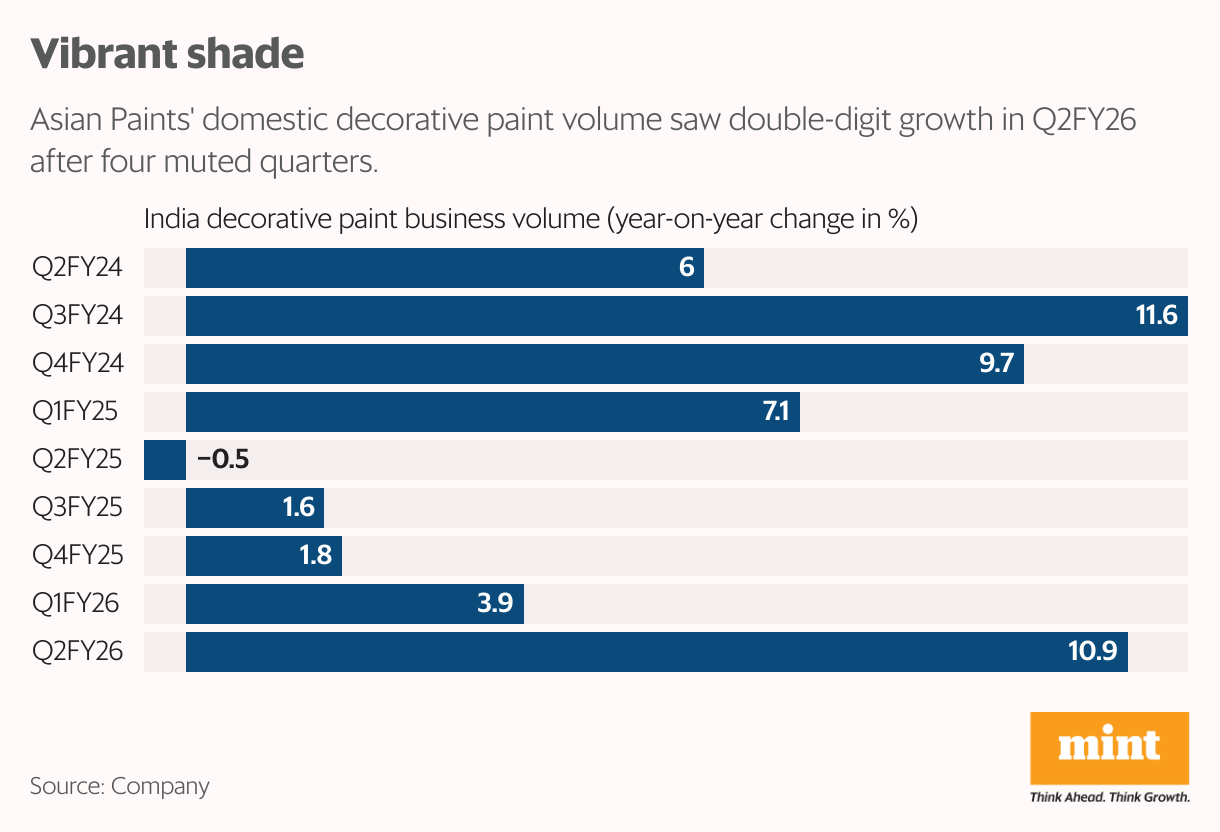

Asian Paints Ltd’s shares rose 3% and hit a new 52-week high of ₹2,897.10 on Thursday, following its stellar September quarter (Q2FY26) results. Decorative paints volume growth rebounded to double digits, up 10.9% year-on-year, after four quarters of muted show.

Despite a challenging industry environment, value growth was relatively healthy at 6%, beating analysts’ expectations. Apart from a low base, an early festive season and better execution aided this recovery.

In comparison, close competitor Berger Paints India’s decorative paint volumes grew 8.8% in the quarter, but value growth was only 1.1%, with consolidated revenue up just 1.9% on-year.

Demand boost

Demand, which had looked uneven for much of the year, improved sharply through September and early October as the festive mood set in. While some paint makers pushed higher grammage, Asian Paints stuck to premiumization. Also, its ad spend was higher than peers as it focused on micro-regional campaigns. Its strong brand recall value, along with distribution strength, has come in handy for Asian Paints.

Consolidated revenue rose 6.3% on-year to ₹8,531 crore, led by broad-based gains across decorative, industrial, and international businesses. Margins held up well, exceeding estimates. Gross margin expanded 242 basis points (bps) to 43.2%, aided by soft input costs and operational sourcing efficiencies, while Ebitda margin improved 220bps to 17.6%. This rebound is comforting given that elevated competition kept profitability under pressure lately. The company has retained Ebitda margin guidance of 18-20% for FY26. Ebitda is short for earnings before interest, taxes, depreciation and amortization.

Raw material prices are expected to remain stable; however, geopolitical uncertainties and exchange rate volatility could pose upward risks to input prices. For FY26, Asian Paints expects mid-single-digit value growth and high-single-digit volume growth, with the 4-5 percentage point gap between value and volume likely to persist.

Improved earnings

A solid comeback in the September quarter has led to upgrades in earnings estimates for FY26 and FY27 by various brokers. However, what may also be fuelling optimism among Asian Paints’ investors is the recent exit of the Birla Opus chief executive officer. “We note the exit of the CEO at Birla Opus competitor may potentially result in a pause in the aggression of the new competitor. Reduction in competitive pressures, green shoots in the paint industry and a favourable base may allow Asian Paints to report stronger revenue growth in H2FY26,” said ICICI Securities in a report on 13 November.

But one should not get complacent about this, as competitive intensity may not have peaked yet. “While Asian Paints outperformed the industry in Q2, we believe it’s too soon to call out an industrywide demand recovery as H1 was weak for all players, including Birla Opus,” said Incred Research Services Private Ltd in a report.

As for other segments, the industrial and automotive coatings businesses delivered 12% on-year revenue growth in Q2FY26. The international portfolio grew 9.9% in rupee terms and 10.6% in constant currency, led by Nepal, Sri Lanka, and the UAE, with profit before tax margin up 450bps to 9% after exiting loss-making Indonesia. The Dubai white cement plant is operational, and the VAM-VAE project is on track for Q1FY27, aiding long-term cost efficiency. But the earnings outlook hinges on the domestic decorative paints business.

Meanwhile, in the last month only, the stock has rallied more than 20% and trades at around 59x FY26 earnings, which is rich in the current backdrop of the paints industry. Asian Paints’ Q2FY26 performance showed that execution strength and brand equity are critical in this business, but sustaining it will require consistent, volume-led growth and strong margins.

{kind=link}