In the backdrop of a prolonged, dismal financial performance, Blue Dart Express Ltd’s price hike announcement could usher in hopes of a revival.

The logistics company has implemented general price increases of 9-12% across shipments for the calendar year 2026. While this development did trigger some excitement in the share price, it fizzled out. Investors would want to see at least one quarter of decent earnings performance, which is crucial for sustainable share price gains.

The stock hit a peak of ₹9,531 on 4 October 2022 and has since failed to reclaim that level. It is down 38% based on rolling three-year returns (from 10 October 2022 to 10 October 2025) calculated using the current market price of ₹5,499.

Weak financials

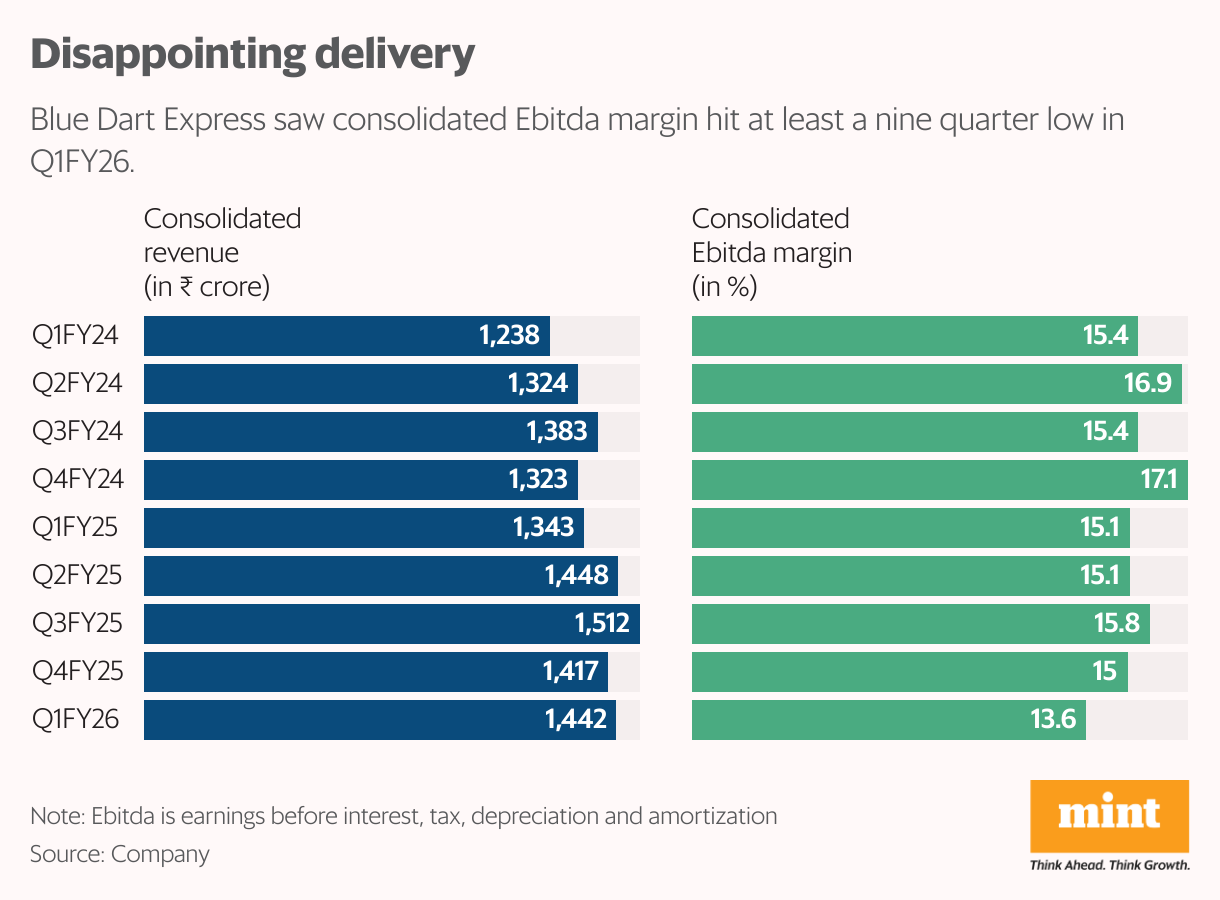

Its financials mirror a similar pain. Consolidated Ebitda slipped from ₹938 crore in FY23 to ₹873 crore in FY25. The consolidated Ebitda margin, too, slid from 18.1% in FY23 to 15.3% in FY25. Both these trends indicate that annual price increases in the past have not always yielded the desired outcomes. Ebitda is short for earnings before interest, taxes, depreciation, and amortization.

The June quarter (Q1FY25) results were also unexciting, with pricing pressure evident from revenue growth being lower than volume growth. Despite an 8.6% year-on-year growth in shipment tonnage to 340,000, income growth was 7.4% on-year at ₹1,442 crore. In the September quarter (Q2FY26), the company could clock 11% on-year volume growth, driven by surface and business-to-consumer (B2C) segments; however, blended realizations are likely to decline by around 1% on-year, said Emkay Global Financial Services.

“Ebitda margin is expected to remain flat on-year as optimal utilization of freighters would be offset by higher contribution from the low-margin surface business,” added the Emkay report dated 8 October.

Pricing discipline

Although business-to-business (B2B) remains the main source of revenue at 70% for Blue Dart, with the rest coming from B2C, the incremental growth rate in the latter stood at 20% versus 2% for the former. As B2C logistics remains more fragmented and has more competitive intensity, it was critical for Blue Dart to take corrective pricing action. Will the price increase make Blue Dart less competitive?

Unlikely, as Allcargo Gati, the rival of Blue Dart, has also announced a price increase of around 10% effective from CY26. Even Delhivery, the other rival, is unlikely to engage in a pricing war, based on its chief executive Sahil Barua’s statements to avoid the current state of “irrational pricing”, despite no formal announcement of a shipment price hike. He commented that the current pricing is unsustainable due to the ever-increasing costs of manpower and infrastructure needed for logistics.

If industry discipline in pricing leads to a recovery in profitability, Blue Dart could once again come on investors’ radar. According to ICICI Securities’ estimates, Blue Dart trades at a P/E of 27x, compared to 40x for Delhivery. Such a sharp relative valuation discount for Blue Dart seems excessive, even when considering Delhivery’s asset-light model, strong foothold in the e-commerce segment, and new-age technology backbone for logistics solutions.

{kind=link}