Exide Industries Ltd is struggling to fuel its core lead-acid business while simultaneously turning its capex-heavy lithium-ion venture into a viable second growth engine.

Investors remain wary—the stock is down 10% in CY25 so far. September quarter (Q2FY26) earnings were soft, hurt by channel destocking across auto replacement, UPS and solar following GST cuts.

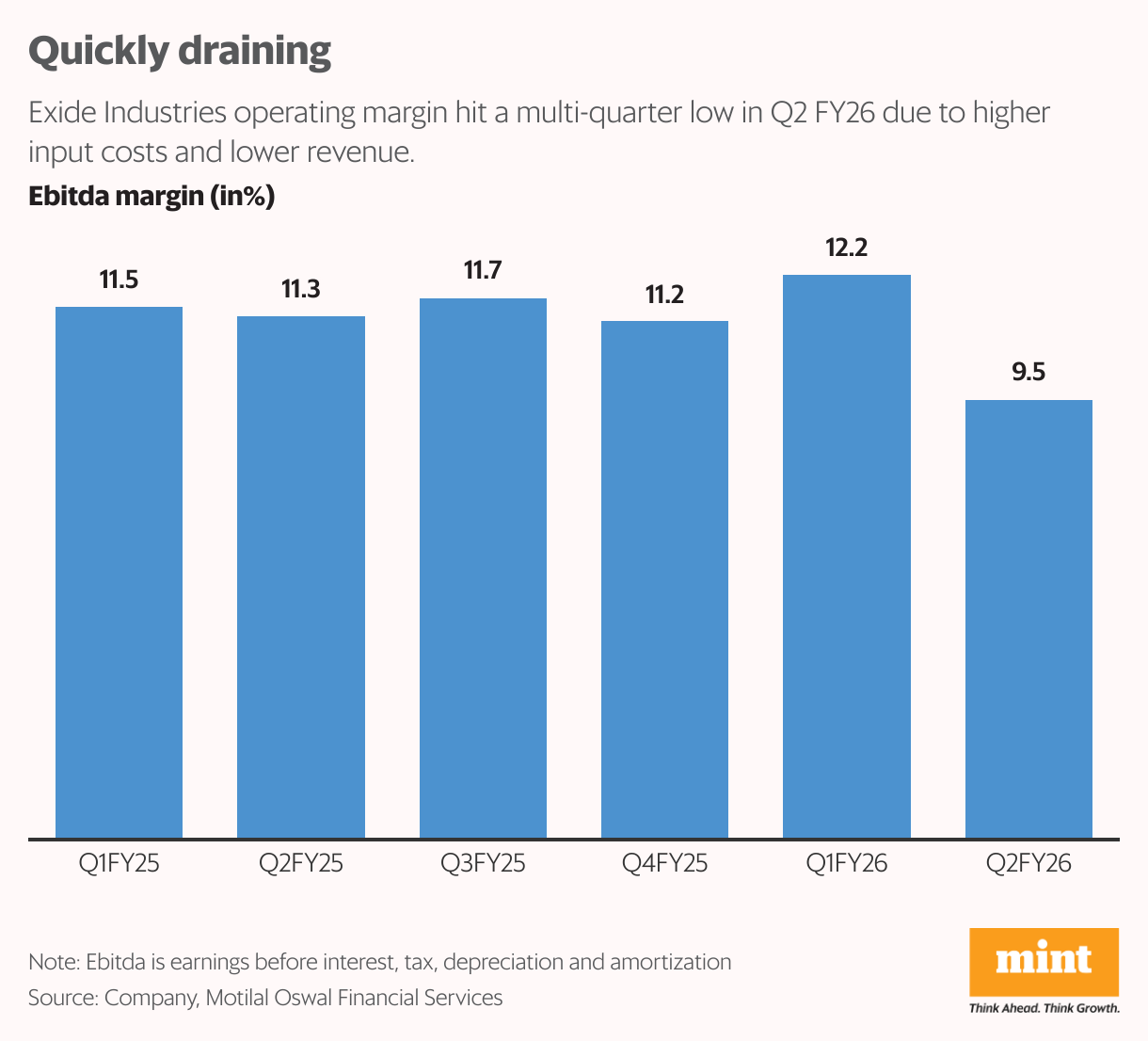

A prolonged monsoon further weakened home-UPS demand. Revenue fell 2% year-on-year to ₹4,178 crore. Exide expects a rebound in H2FY26 as distributors rebuild inventory and OEM demand improves.

Margin strain

Operating margin slipped 180 basis points (bps) to 9.4% in Q2FY26, hit by weak revenue, higher input costs and an extended producer responsibility (EPR) provision.

Achieving the company’s 12–13% margin guidance for H2FY26 now looks challenging and hinges on restocking and planned Q4 price hikes.

In comparison, rival Amara Raja Energy & Mobility Ltd fared better with revenue up 8% year-on-year. Its margins slid 200 bps year-on-year to 12%, but rose 40 bps sequentially. Further, its raw-material costs eased as well, with the raw material/sales ratio falling 330 bps to 67.2%.

Lithium-ion leap

The strategic swing factor for Exide remains progress on its lithium-ion business. Phase 1 of its 6GWh cell plant with SVOLT is nearing trial runs, with production slated for end-FY26. Phase 2 will add another 6GWh.

Together, the two phases involve around ₹6,500 crore in capex, of which ₹3,950 crore has already been invested till date. Early customer wins like Hyundai, Kia, and Atul Auto offer initial demand visibility as Exide tries to expand in mobility and storage.

However, the landscape is crowded.

Reliance, Ola Electric, Suzuki, Tata Sons, Jindal, ACME and steady Chinese imports all tighten pricing pressure. Exide also lacks PLI support, raising the bar on execution and cost discipline.

With utilization in FY27 expected at only 25–30%, the lithium business will scale slowly—and being a low-margin segment, it could dilute long-term return ratios. Rapid technology shifts and potential restrictions on China-linked sourcing pose additional risks, cautions Nomura Global Markets Research.

The weak Q2 print has triggered estimates cuts. Motilal Oswal Financial Services has reduced its FY26/FY27 earnings per share estimates by 9% and 3%, respectively. The stock trades at around 19x FY27 P/E, per Bloomberg. With core margins under pressure and lithium still years from meaningful contribution, the valuation looks reasonable—but not compelling.

{kind=link}