The S&P BSE Capital Goods index gained 21% in the previous six months on the back of some key developments.

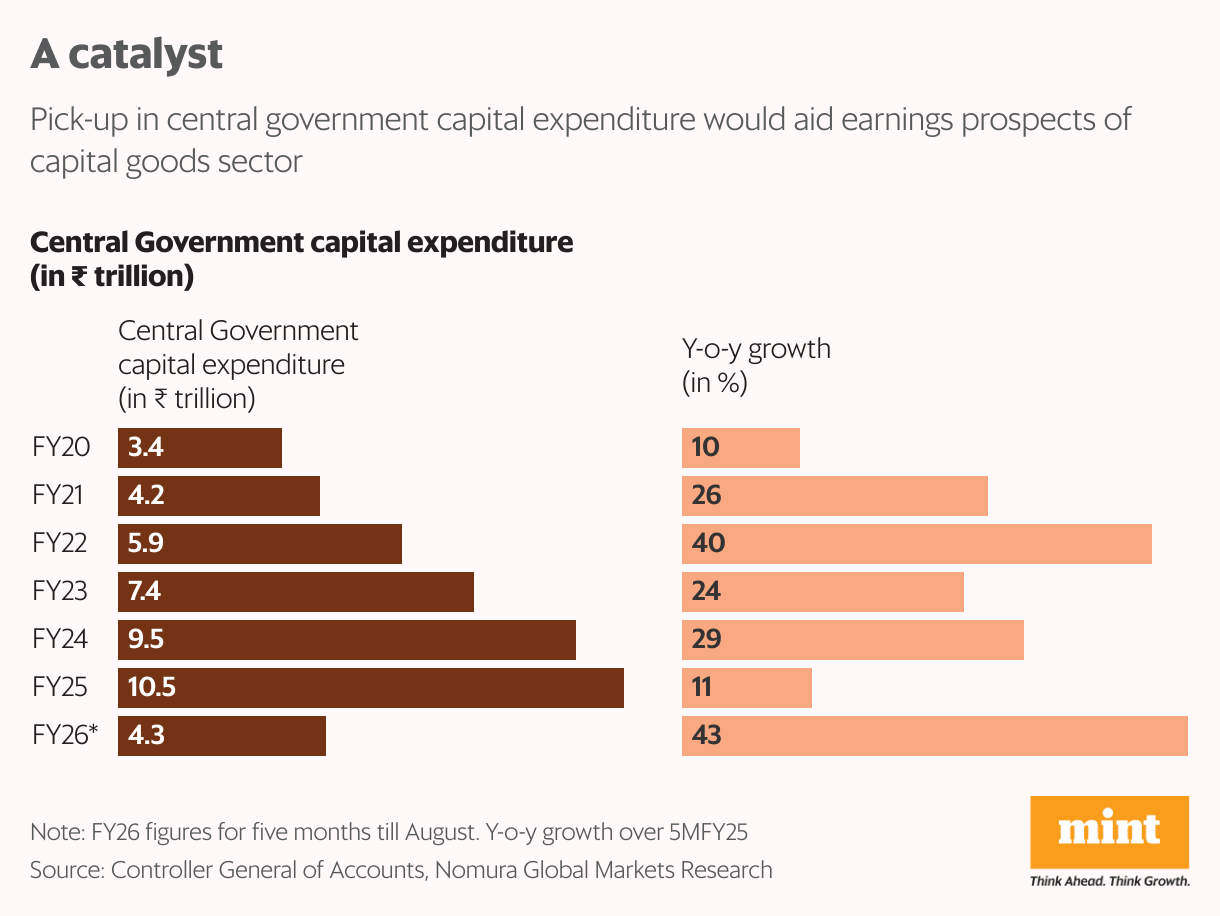

Among those—the Union government’s capital expenditure spending rose 43% to ₹4.3 trillion in the first five months of 2025-26 (April-August), and the ministry of defence has outlined 15-year sectoral needs, targeting annual spending of $25-30 billion ( ₹2.2-2.6 trillion).

Also, strong execution of record-high order books is expected to translate to decent second-quarter (July-September) earnings for some capital goods companies. Improving execution is seen offsetting the adverse impact of lower exports and deferment of new orders due to US tariff-related uncertainties.

Nomura Global Markets Research expects capital goods companies to report 15% year-on-year revenue and Ebitda growth for the second quarter. However, higher prices of some commodities and lower exports could put margins under pressure (exports typically fetch higher margins).

Power transmission

Among segments, solar equipment manufacturers are expected to grow at nearly 40%, accompanied by margin expansion of 500-800 basis points, Nomura said.

Brokerage PL Capital expects healthy revenue growth for transmission and distribution companies as well, at over 20%, led by strong domestic demand. Continued traction from data centers, power transmission and distribution, and electronics would drive order inflows during the second quarter quarter, it said.

Project-based companies, including heavyweights such as Larsen and Toubro Ltd and Bharat Heavy Electricals Ltd, could see decent revenue growth led by healthy order book execution, PL Capital added.

Consumables

Companies that make products such as abrasives, adhesives, and sealants, could be laggards with muted second-quarter revenue growth, weighed by weaker exports and Chinese dumping despite strong domestic demand.

Industrial machinery companies that make products such as turbines, industrial motors, and compressors are also expected to report subdued growth, according to PL Capital.

These two sub-segments may also see a decline in Ebitda margin because of lower exports and pricing pressure, the brokerage added.

Defence sector

Defence companies, despite strong order inflow, are expected to report below-industry-average revenue growth of 11%, and lower margin because of increased material costs, PL Capital cautioned.

While steel and zinc prices have remained largely stable, copper prices increased by about 6% on-year and aluminium prices by about 8% during the July-September quarter.

More importantly, the trend in order inflows—a crucial gauge for revenue visibility—shows a sharp divergence. On an aggregate basis, order inflows for defence companies under Nomura’s coverage grew by a robust 23% to ₹1.8 trillion in the second quarter.

State-owned defence companies Hindustan Aeronautics Ltd and Bharat Electronics Ltd recorded growth of 121% and 114%, respectively, in terms of orders in the second quarter. However, order inflow for other companies in Nomura’s coverage declined 3%.

Private capex

The S&P BSE Capital Goods index has remained flat in the year so far, against about a 4% gain in the Sensex.

Revival of private capital expenditure, a crucial re-rating trigger for the capital goods sector, remains missing. In fact, Nomura noted that the value of new capex announced by private companies declined 46% to ₹5.2 trillion in the September quarter—a five-quarter low.

For now, US tariffs and other uncertainties could delay private capex further.

That said, the recent cuts in goods and services tax and their likely boost to consumption could boost industrial capex in the second half of FY26 (October 2025-March 2026).

{kind=link}