Ceat Ltd stock hit a new 52-week high of ₹4,350.60 on Tuesday, buoyed by upbeat margin and demand outlook. Stable input costs would keep the tyre maker’s margins comfortable in a seasonally weak December quarter (Q3FY26).

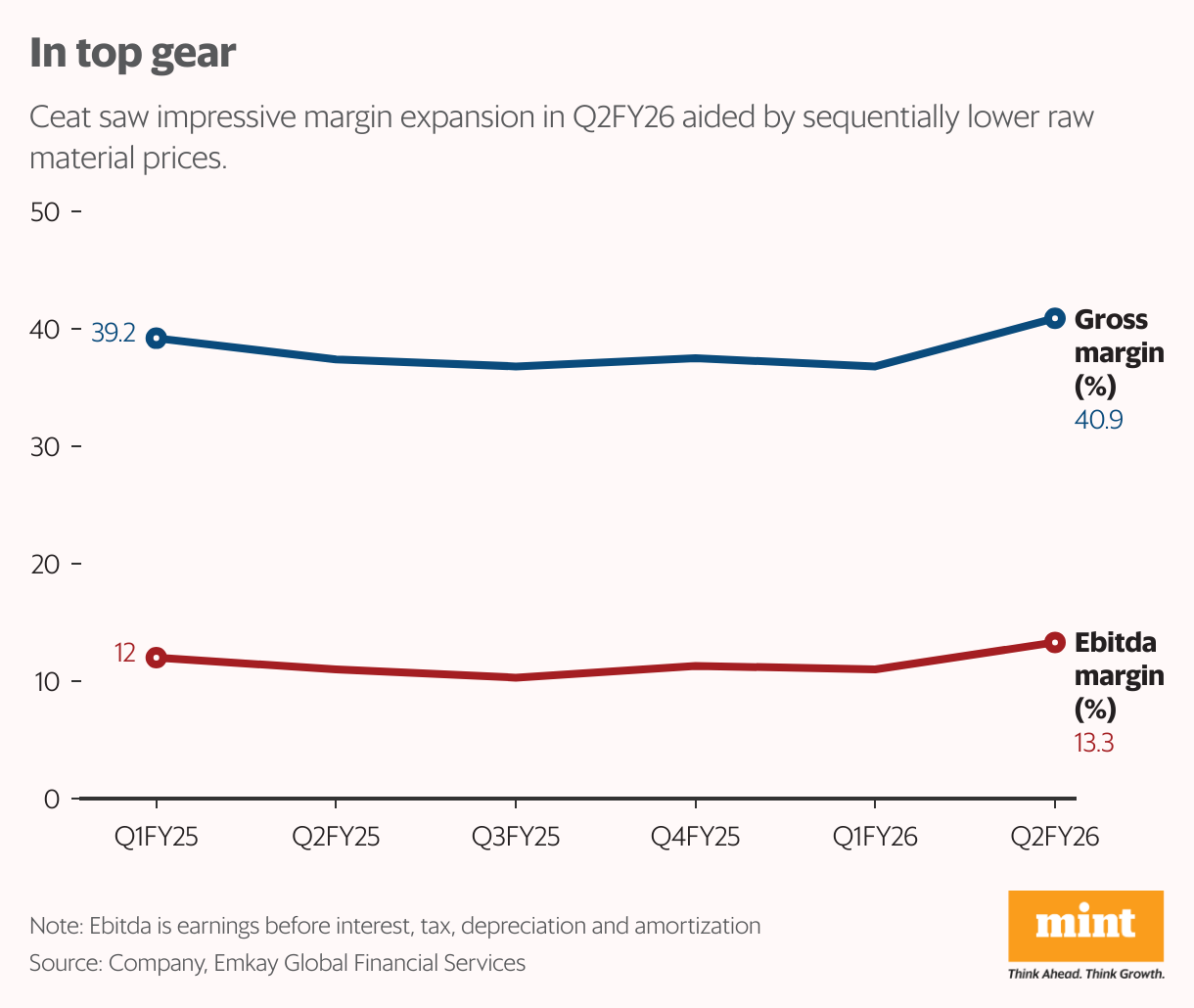

Benign raw material costs pushed Ceat’s operating margin higher by over 200 basis points both year-on-year and sequentially in Q2FY26. Thus, consolidated Ebitda margin at 13.3% beat consensus estimate of 11.6%.

Raw material basket declined 5% sequentially in Q2FY26 with crude oil prices steady at around $65 per barrel, international rubber prices at $1,700–1,750 per tonne, the management said.

Synthetic rubber prices were 3.0-3.5% lower, and nylon fabric prices were 2.0-2.5% lower sequentially. Input costs are expected to remain in a similar range sequentially in Q3.

On near-term demand, two-wheeler segment is likely to grow in high single-digit and truck and bus radial/passenger car radial tyres in mid-single-digit. Ceat is confident of sustaining double-digit growth in the domestic market, aided by goods and services tax rate cut and rising premiumization.

It aims to sustain the current margin profile. In the export markets, demand for agri-radial tyres and off-highway tyres is expected to remain strong in the EU, Africa, and Latin America region.

However, there are some short-term blips such as Camso integration. Ceat completed the acquisition of Michelin Group’s Camso Construction Compact Line Business effective 1 September 2025.

Currently, sales are done through a sales and supply agreement with Michelin, which is expected to shift to direct supply to customers in three-four quarters. Also, Ceat would continue to procure semi-finished goods from Michelin for another five to six quarters until a complete value chain is established.

“We trim FY26E/27E earnings per share by 2/4% on near-term drag from Camso, even as core-business margins improve,” said Emkay Global Financial Services in a report on 18 October.

Further, Ceat’s consolidated net debt rose sequentially to ₹2,944 crore from ₹1814 crore and the debt/Ebita ratio deteriorated to 1.8x from 1.21x. Nuvama Research estimates Ceat’s net debt to rise from around ₹1,900 crore in FY25 to around ₹2,800 crore in FY26 due to the Camso takeover.

Ceat has reaffirmed its FY26 capex guidance at ₹1,000 crore. Ceat’s shares are up 34% so far in 2025. Timely and smooth integration of Camso, which would have a bearing on return ratios and margin trajectory, is key.

{kind=link}