Coforge Ltd, which has emerged as a growth leader among mid-cap IT firms, delivered another quarter of robust numbers post market hours on Friday. Revenue increased 6% sequentially in constant-currency terms to ₹3,986 crore, even as rupee depreciation pushed growth further to 8.1%.

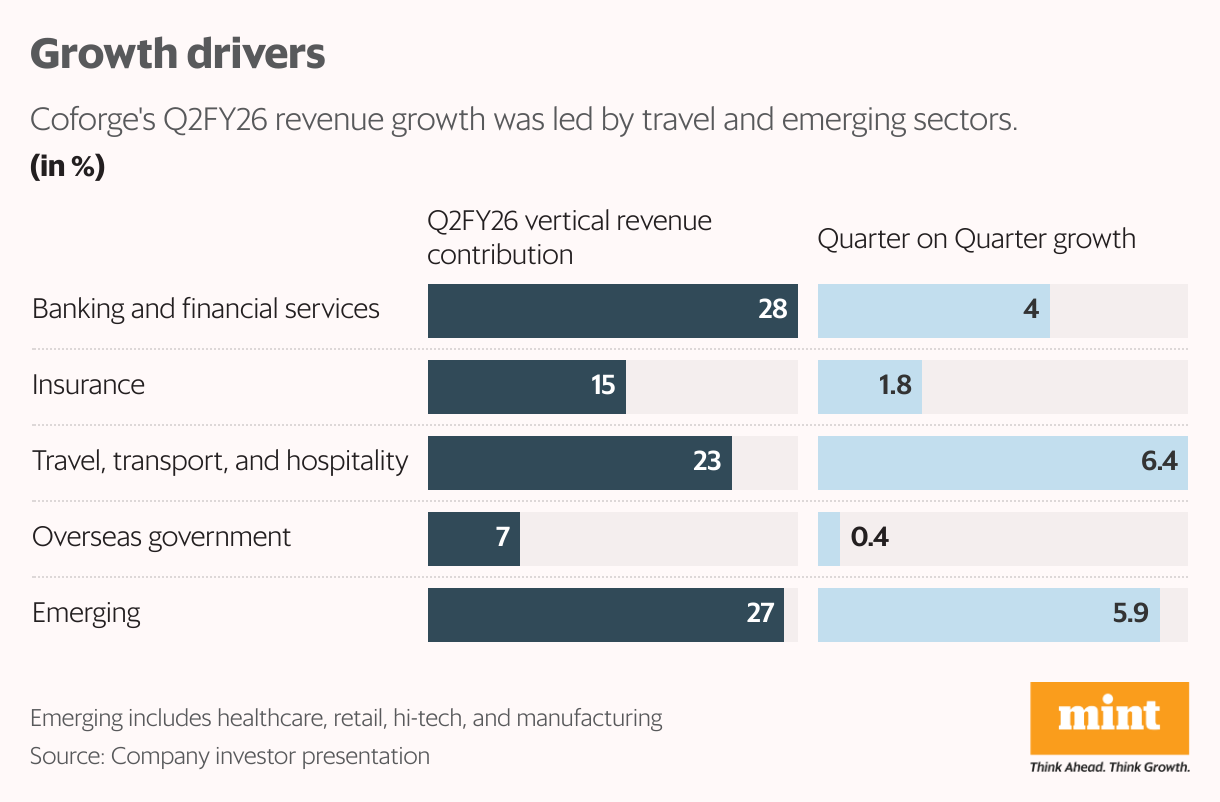

Coforge’s BFSI (banking, financial services and insurance) exposure at over 40% is among the highest in the industry. With lower interest rates and a growing need for real-time payments, growing IT spends have continued to benefit Coforge, which saw BFS revenues increase 4% sequentially. But following the divestment of its insurance product, AdvantageGo, to Sapiens UK, revenue growth from insurance was muted at 1.8% sequentially.

Overall growth kept pace with travel, transport and hospitality growing 6.4% sequentially and 61% year-on-year, for which the mega $1.56 billion 13-year deal signed with Sabre is to thank. While the deal was expected to contribute $120 million in incremental revenues annually, there were fears that financial struggles from Sabre would spill over to Coforge. But the latest reported numbers alleviated concerns—days sales outstanding was only three days higher over last year, and free cash flow to profit after tax has improved from 50% to 86%.

Coforge had carved a specialized niche for itself in travel and insurance. But for its next leg of growth, diversification will be key. The 5.9% quarter-on-quarter growth in emerging verticals, including healthcare, retail, hi-tech and manufacturing, puts it on the right track. The management expects healthcare to touch $100 million annualized run-rate by Q4.

Last year’s Cigniti acquisition has been successfully integrated and margins have surpassed expectations. Coforge’s gross margin expanded 31 basis points (bps) quarter-on-quarter as utilization improved, thanks to automation and AI-led benefits, which complemented a persistent focus on large, high-margin projects. Slower growth in other people costs on lower ESOPs, along with operating leverage and a drop in bad-debt provisions, led to a 251 bps sequential expansion in Ebit—earnings before interest and tax, a measure of profitability—to 14%. Higher forex gains and slower-than-topline growth in interest expenses have meant a 342-bps expansion in pre-tax earnings.

Uncertain environment, but promising prospects

Coforge has refrained from talking AI numbers, unlike peers Tata Consultancy Services Ltd and HCL Technologies Ltd, which have drawn out a tangible AI roadmap and started quoting AI revenues, respectively. Amid the higher new H-1B fees in the US, which contributes 58% of Coforge’s revenues, its 52% offshore revenue mix can play spoilsport. It filed 65 new H-1B Visa petitions in FY25. Q2FY26 sub-contractor costs have increased 15% sequentially, indicating that this may be how the company plans to navigate the tighter immigration policies.

Deal wins have moderated to the $500 million levels—at $507 million in Q1FY26 and $514 million in Q2, after spiking to $2 billion aided by the Sabre deal in Q4FY25. Synergies from Cigniti are visible in Coforge, having brought in two large deals since the acquisition.

Attrition, at 11.4%, remains among the lowest in the industry. The order book executable over the next 12 months stands at $1.63 billion, up 27% year-on-year. Despite wage hikes announced on 1 October, management expects lower ESOP and depreciation costs to help sustain the Ebit margin at 14% for FY26. Any upsides due to a seasonally strong Q4 will be reinvested in AI and delivery capabilities to drive growth.

But the stock is trading at 41 times its FY26 earnings estimates, as per Emkay Global Financial Services. Having already gained over 10% in the past month, it has steeply outperformed the Nifty IT index’s 4% return.

{kind=link}