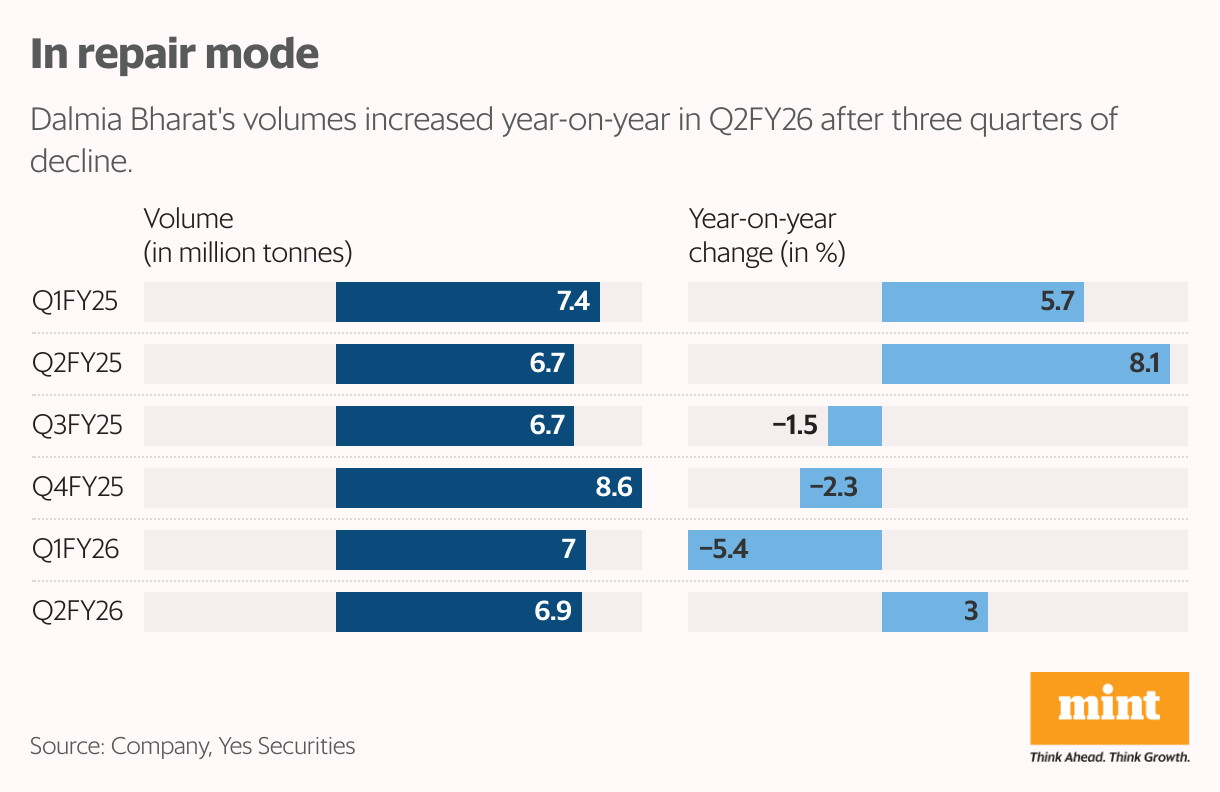

Dalmia Bharat Ltd’s focus on capacity expansion could help it regain lost ground. The company’s volumes had declined year-on-year from Q3FY25 to Q1FY26 amid muted cement demand and rising competition in its core southern and eastern markets.

However, in the September quarter (Q2FY26), volumes rose about 3% year-on-year to 6.9 million tonnes (mt), broadly in line with industry growth. The ramp-up of recently added capacities and the completion of ongoing projects provide visibility for medium-term volume growth.

Projects on track

According to the Q2 earnings call, capacity addition projects in Belgaum, Pune, and Kadapa are progressing as planned. These will together add about 12 mtpa of new capacity, reinforcing Dalmia’s presence in the west and south. A 3.6 mtpa clinker line in Umrangso, Assam has begun trial runs, with commercial production expected in Q3—supporting 2–2.5 mtpa of future grinding capacity in the east and northeast.

The company is also pursuing a greenfield project in Jaisalmer (Rajasthan), with land acquisition and approvals expected by March 2026. Overall, Dalmia targets a total installed cement capacity of 75 mtpa by FY28, up from 49.45 mtpa currently.

Rising competition

The road isn’t smooth. UltraTech Cement Ltd has announced a fresh capacity addition plan where it will add 18 mtpa capacity in the north. Dalmia is planning to foray into the north via Jaisalmer. The likely increase in competitive intensity post UltraTech’s capex in this region could deteriorate margin profile and further suppress potential internal rate of return at Jaisalmer, which already faces structural freight disadvantages, says DAM Capital.

Also, robust supply additions in south and east, along with any delay in demand revival could cap pricing and profitability improvement for Dalmia.

Management expects H2FY26 to be stronger, aided by better consumer sentiment and pent-up demand. The company has passed on the full GST cut benefits to customers and is optimistic about price stability if demand improves. It has also guided for ₹150–200 per tonne cost savings over the next two years. However, rising petroleum coke prices and rupee depreciation could offset some of those gains.

The market is also watching for updates on Dalmia’s proposed acquisition of Jaiprakash Associates’ cement assets in central India—a critical piece in its growth puzzle. The management expects clarity this quarter. The stock has already gained 22% in 2025, but the acquisition outcome will be key for Dalmia to achieve its 75 mtpa capacity target.

{kind=link}