Eternal Ltd (formerly known as Zomato) posted a mixed bag performance in the September quarter (Q2FY26). Year-on-year growth in food-delivery net order value (NOV) recovered to 13.8% from 13.1% in Q1FY26—although it was higher at 21.4% in Q2FY25.

This improvement in the second quarter, albeit marginal, was achieved despite goods and services tax (GST) being levied on food delivery fees, which may have dampened the demand prospects of the food delivery business to some extent.

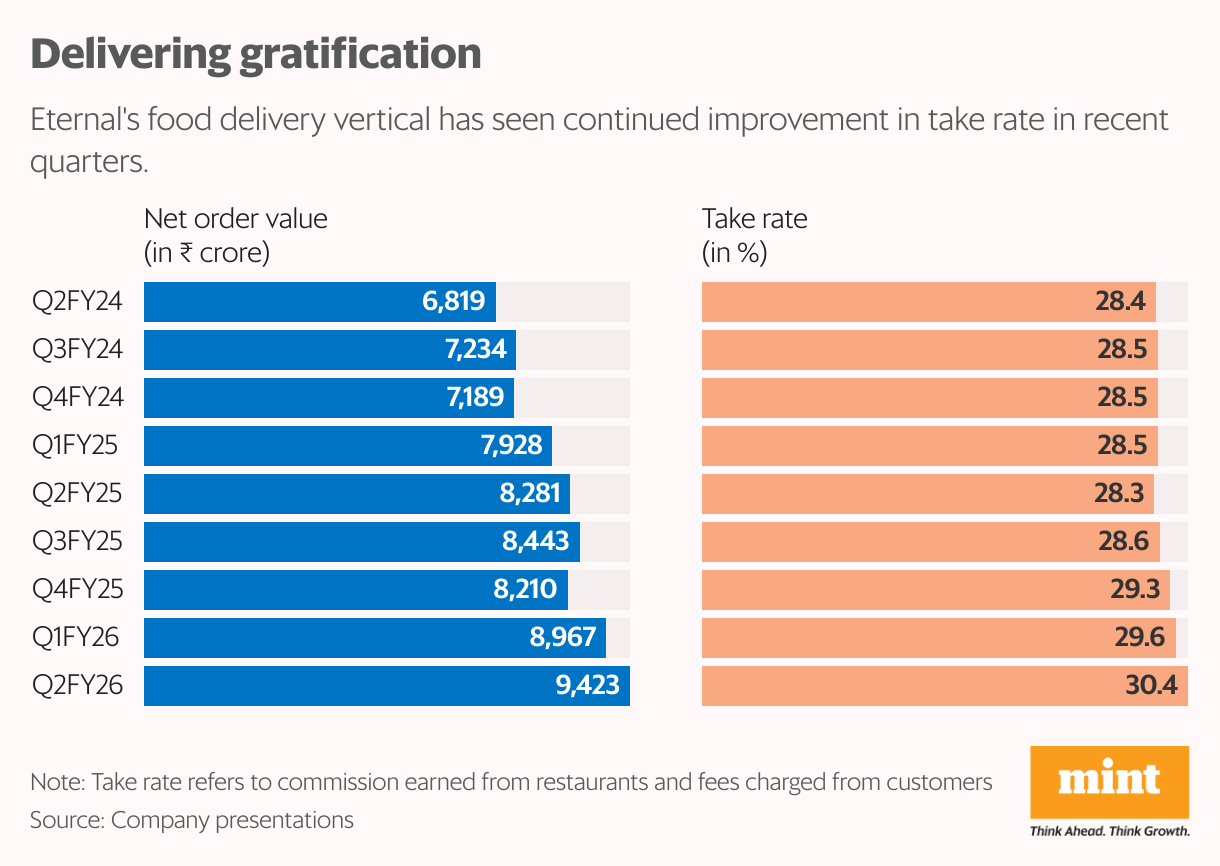

Secondly, the take rate (commissions earned from restaurants and platform fees from customers, etc.) increased sequentially and on-year by 75 basis points (bps) and 212bps, respectively, to 30.4% in the quarter.

It is worth noting that there has been noise about Rapido entering into food-delivery service through the Ownly app, which focuses on a zero-commission model for restaurants and a flat-fee pricing structure for customers to offer lower overall costs.

True, these are still early days before Rapido spreads its reach, but Zomato’s ability to negotiate hard with restaurants and charge more fees from customers has been remarkable. This is reflected in its commission rate, which has risen over the last two years from 28.4% in Q2FY24 to 30.4% in Q2FY26, despite frequent friction with the National Restaurant Association of India (NRAI) that led to a Competition Commission of India (CCI) probe.

The quick-commerce loss

As Zomato’s food-delivery business is likely to generate Ebitda of ₹2,000 crore in FY26 based on annualizing H1FY26 numbers, it is giving the cushion to absorb more losses in the quick-commerce arm Blinkit. Ebitda is short for earnings before interest, taxes, depreciation, and amortization.

This has made Eternal’s management even more aspirational as it has finally raised the dark-store guidance to 3,000 stores by March 2027 from 2,000 stores by December 2025. Ebitda is short for earnings before interest, taxes, depreciation, and amortization.

In view of the aggressive store addition for Blinkit, it is likely that Ebitda loss of ₹156 crore in Q2FY26 could rise. Along with the initial costs of opening new stores, management has clearly stated that their marketing spend could also increase as they expand into more categories. But losses should not be the focus for at least one year, as the business is still in the high-investment and high-growth phase.

Investors should focus on revenue growth rather than the NOV of Blinkit, as 80% of the goods are sold as owned inventory rather than on a commission basis from third parties. Based on the quarterly revenue of nearly ₹10,000 crore in Q2FY26, when the bulk of the transition from NOV to revenue was completed, each store has an average revenue per store of ₹6 lakh per day. Even if we take ₹5 lakh per day as revenue per store for 3,000 stores, Blinkit has the potential to reach ₹50,000 crore revenue by FY28. But it remains to be seen whether Blinkit achieves its stated goal of about 5% Ebitda margin in quick commerce in the long run.

Here, Blinkit’s main disadvantage against modern retailers, such as DMart and Reliance JioMart, could be its ability to compete on price. Thus, it may not be able to achieve Ebitda margin of 7% of the two rivals, but its own target for the margin may be feasible.

As Eternal is not yet profitable at Ebitda level, the relevant metric to value it is EV/sales. As Eternal’s business is tilting more towards DMart with the inventory-led model, its combined EV/sales of 1.5x for the total of Zomato and Blinkit is not expensive considering that DMart is quoting at 3x based on FY28 estimates, according to Motilal Oswal estimates.

So far this calendar year, the Eternal stock is up around 24%, compared to 8% returns by the Nifty 50. A delay in achieving breakeven due to elevated spending in marketing and investments in other businesses could upset the apple cart for the company.

{kind=link}