Max Healthcare Institute Ltd has been in the buzz lately. On Friday, the National Stock Exchange said Max will be included in the Nifty 50 index from 30 September as a part of the semiannual review of index constituents.

When it is included, Max is likely to have more weightage in the index than Apollo Hospitals Enterprise Ltd, going by its current free-float market capitalization of ₹90,000 crore versus ₹79,000 crore for the latter.

There’s also Max’s suspension of cashless treatment across its hospitals for Bajaj Allianz policyholders. This has to do with the tussle between hospitals and general insurance companies over alleged overbilling of customers.

The cashless facility suspension may have dampened the positive sentiment around Max’s Nifty inclusion announcement, possibly explaining the stock’s initial muted reaction. Passively managed funds that replicate Nifty constituents will have to buy shares worth $400 million at the time of the rebalancing, as per Nuvama’s estimates, though it’s still some time away.

Irrespective of the Nifty inclusion, actively managed funds will continue to evaluate Max’s relative attractiveness versus Apollo Hospitals. Max’s shares have risen 43% in the past year, massively beating Apollo’s 14% gains, indicating that the stock has been on the radar of savvy investors for some time now.

PL Capital and Motilal Oswal Financial Services have valued Max’s hospital business at 36x and 35x, based on EV/Ebitda for FY27. Both have assigned a lower multiple of 30x EV/Ebitda for Apollo’s hospital business. The comparison is only for the hospital business and excludes the diagnostic segment, which is smaller. Plus, Apollo has a pharmacy and 24/7 digital businesses.

Bed capacity

So, why is Max’s hospital business getting an almost 20% valuation premium over Apollo’s? To begin with, Max’s bed capacity was 5,200 at June-end versus the much higher 9,463 beds of Apollo. But Max’s occupancy rate in the June quarter (Q1 of FY26) was higher at 76% compared with 65% of Apollo.

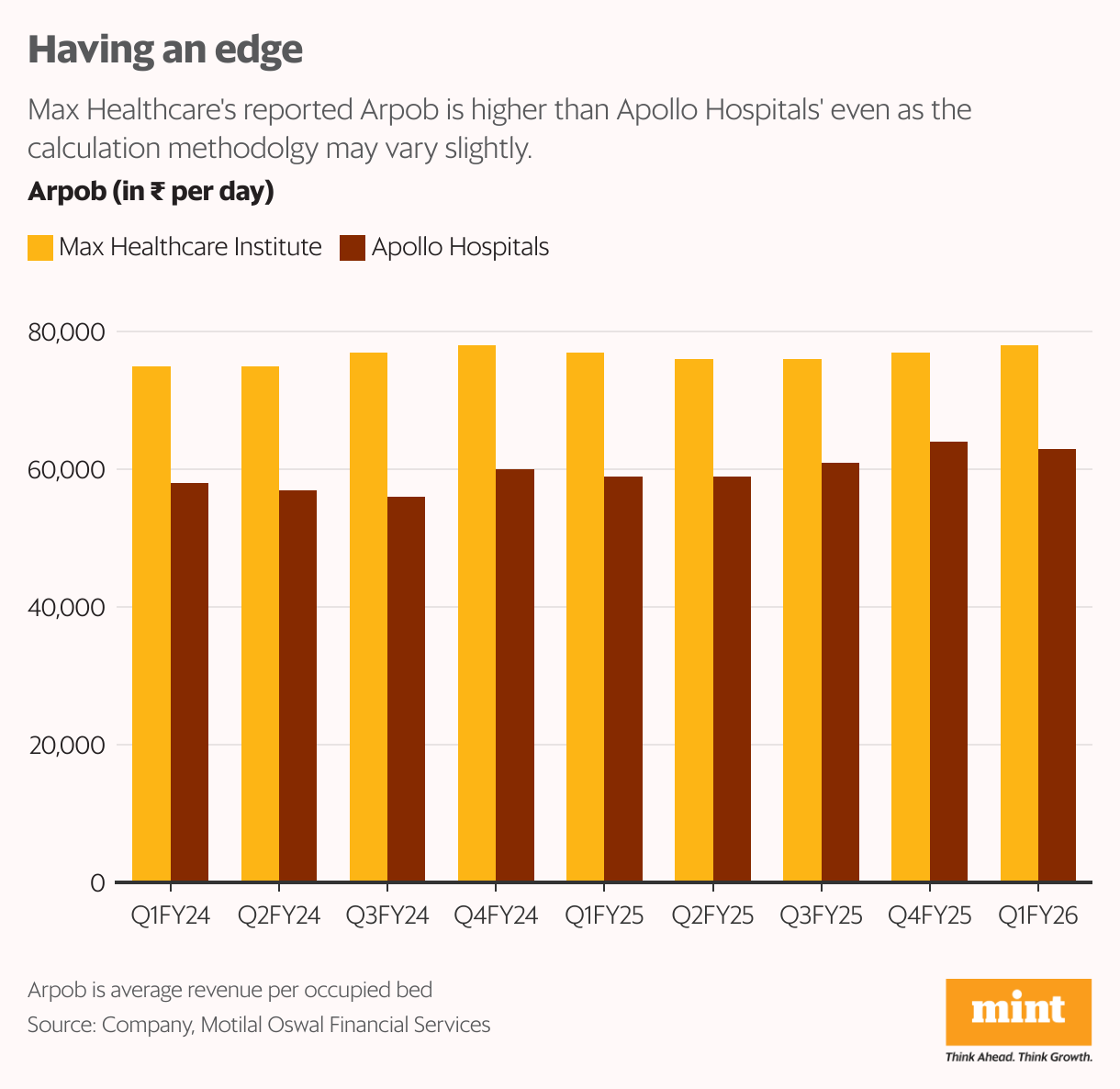

The Ebitda margin for both is similar at 25%. But Max’s reported Arpob (average revenue per occupied bed) was ₹78,000 versus ₹63,000 for Apollo, as per Motilal Oswal. There could be some difference in calculation regarding netting off fees paid to service doctors.

Max’s return on capital employed (ROCE), excluding capital work in progress and new units in Q1, was 32% versus 28% for Apollo (excluding capital work in progress). The gap appeared more glaring considering that Apollo has been in existence for 42 years versus Max’s 24 years, which must have given the former a capital cost advantage in terms of lower real estate cost.

Apollo plans to add 50% capacity over the next five years, while Max aims to double capacity, albeit on a smaller base. Thus, Max is likely to deliver a higher growth rate than Apollo even beyond FY27. This also suggests the FY27 valuations mentioned earlier capture Max’s higher growth until then adequately.

Max plans to use the ‘agreement to lease’ route for almost 30% of its capacity expansion, which is about 1,500 beds. This could potentially widen its ROCE advantage over Apollo. This route involves getting a customized hospital made by a third party and taking it on a long-term lease.

The two broking firms seem justified in assigning higher valuation multiples to Max, given the superior ROCE and higher future growth potential. But as the target prices of both firms show just about 10% upside for Max, the stock’s near-term upside may well be capped.

{kind=link}