India’s hotel industry has been having its moment in the sun. Revenues of hotel companies are rising, margins are near all-time highs, and stock prices have been on a dream run.

In the three years to 23 September, shares of The Indian Hotels Co. Ltd (IHCL) recorded a compound annual growth rate (CAGR) of 32%, EIH Ltd 27%, and Chalet Hotels Ltd an impressive 43%.

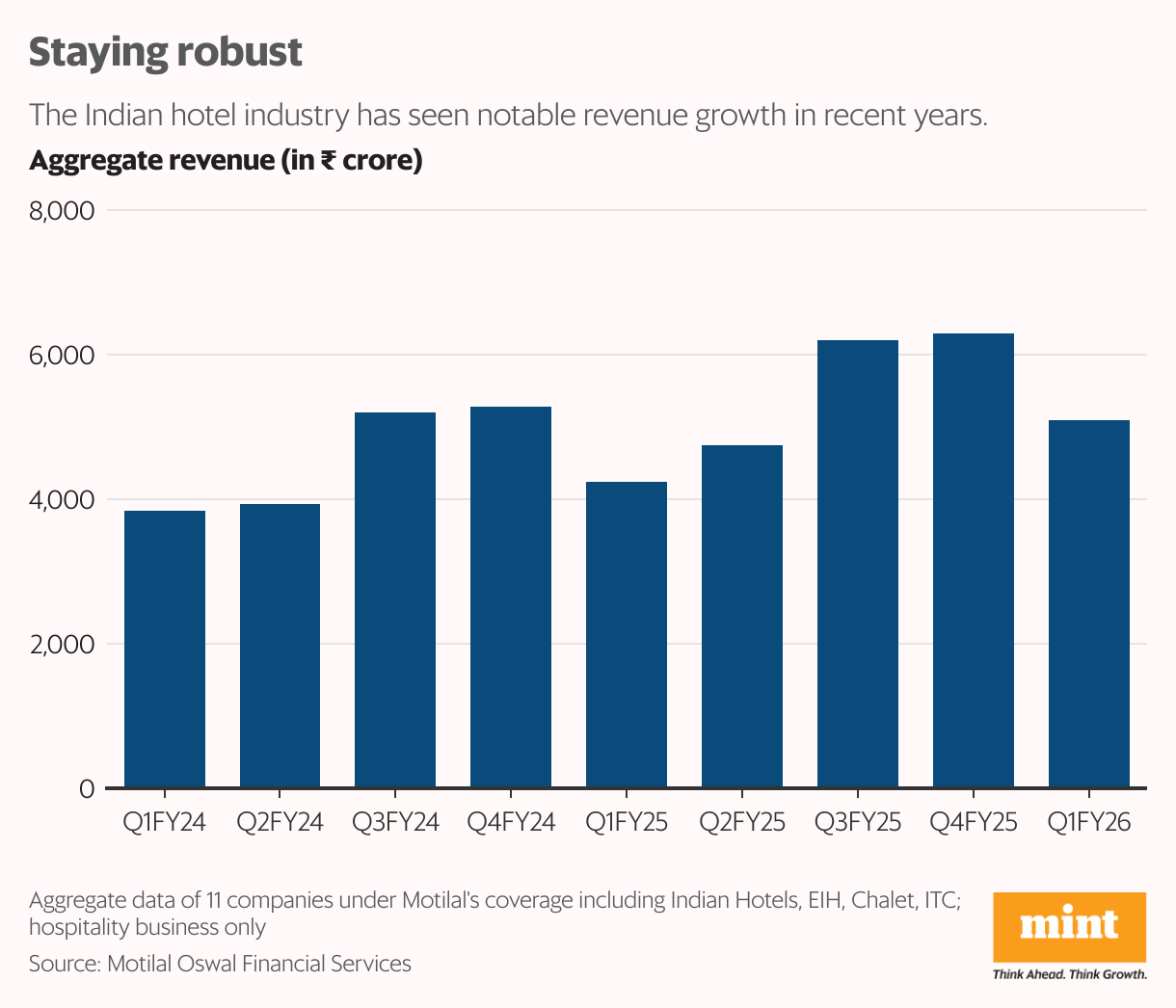

Growth delivered, too. IHCL’s consolidated revenues have increased at a 40% CAGR in three years to FY25, with Ebitda margin jumping from 13% to 33%, while Chalet’s hospitality revenue is up by 55% CAGR. EIH’s turnaround has been impressive, with 40% CAGR in revenue and margin improving from -3% in FY22 to 37% in FY25.

The momentum continued in the June quarter (Q1FY26) for most—Chalet’s Q1FY26 revenues rose 18% year-on-year, aided by expansion and higher average room rate (ARR). ITC Hotels Ltd and IHCL revenues rose 16% and 32% respectively, while EIH’s growth was slower at 9%. “The Indian hotel sector posted a resilient Q1FY26, with about 12% RevPAR growth led by ARR gains and stronger occupancy despite softer air traffic,” said a Motilal Oswal Financial Services report on 24 September. RevPAR is revenue per available room.

What gives?

The hotel industry is asset-heavy; building and running hotels requires a lot of money. So, when demand shoots up and supply can’t keep pace, a demand-supply mismatch happens. Room rates rise, occupancy rates improve, and margins increase. This has been playing out for the last three years.

Factors aiding growth include rising middle-class spending, destination weddings, corporate off-sites, and foreign tourists flying in (15% growth expected in FY26). Plus, hotel rooms costing up to ₹7,500 will now attract only 5% goods and services tax (GST), which should support demand.

Companies have solid expansion plans. IHCL (Taj Hotels) has an ambitious target of operating more than 700 hotels by 2030, up from 565 now. To meet this goal, it is buying new properties, building greenfield projects, and expanding its footprint across popular destinations such as Goa and Lakshadweep.

EIH (Oberoi Hotels) plans to reach 50 hotels in the next few years, up from 30 now. This includes openings in international destinations like London and Bhutan that will strengthen its global appeal.

ITC Hotels is pursuing a slightly different strategy, going asset-light to scale faster and improve returns. It is currently adding more than one hotel per month and aims to surpass 20,000 rooms by 2030—a significant leap that signals its intent to be a key player across segments while keeping capital efficiency in mind.

Together, these moves reflect how Indian hotel chains are increasing their supply and positioning themselves to capture the long-term tourism boom.

While it lasts

But all this seems good until the favourable supply scenario suddenly turns unfavourable. Moreover, the sharp rally in stocks means valuations have climbed along with earnings. Thus, if one is not early to the party, one is late—a key problem with cyclical industries such as hotels.

So, buying at potentially peak margins or peak valuations does not make sense. Sure, margins may still inch higher from here, but the downside risk is now far greater than the upside.

To be sure, the medium-term structural story for Indian hotel companies is intact, as demand should stay upbeat and supply is still catching up. But in the short term, investors are better off skipping this party.

{kind=link}