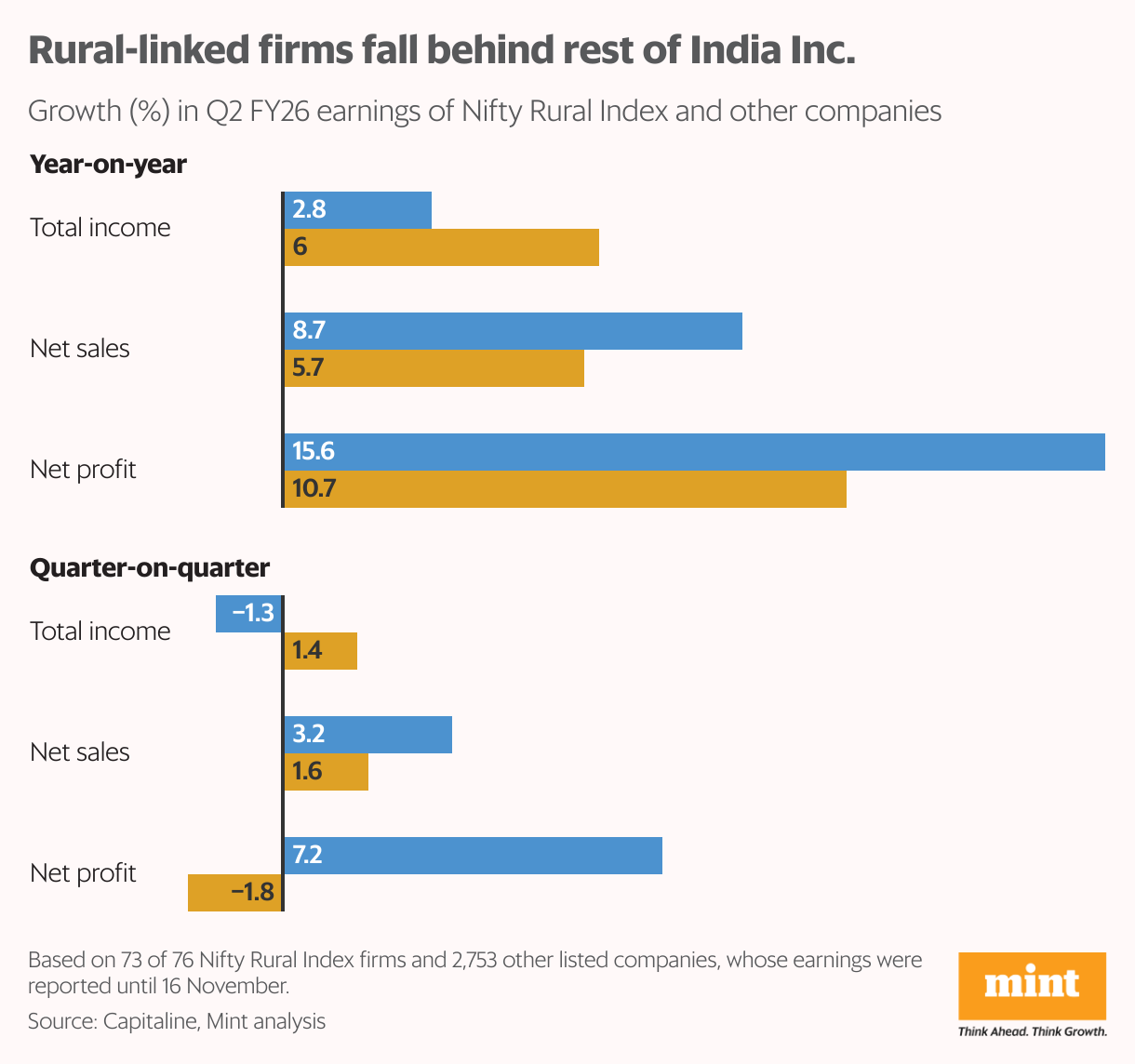

Earnings of 73 Nifty Rural Index companies — whose business models are closely tied to India’s hinterland — revealed that their aggregate growth in total income hit an eight-quarter low of 2.8% year-on-year (y-o-y) in Q2 of FY26, the lowest since Q3 FY24 when it recorded 13% total income growth.

For the first time in two years, aggregate total income of rural-linked firms grew slower than the rest of India Inc (comprising 2,753 companies), which posted a 6% revenue expansion in Q2.

The weakness becomes more apparent when viewed quarter-on-quarter. The headline total income growth of the Nifty Rural Index constituents has fallen 1.3% each for two successive quarters, extending a slowdown that began earlier this year. Meanwhile, the rest of India Inc managed a topline growth of 1.4% on a sequential basis.

Significantly, though, rural-linked firms recorded higher growth than non-rural peers in net sales (8.7% vs 5.7%) as well as net profit (15.6% vs 10.7%) in the July-September quarter on a y-o-y basis, a ninth straight quarter of outperformance.

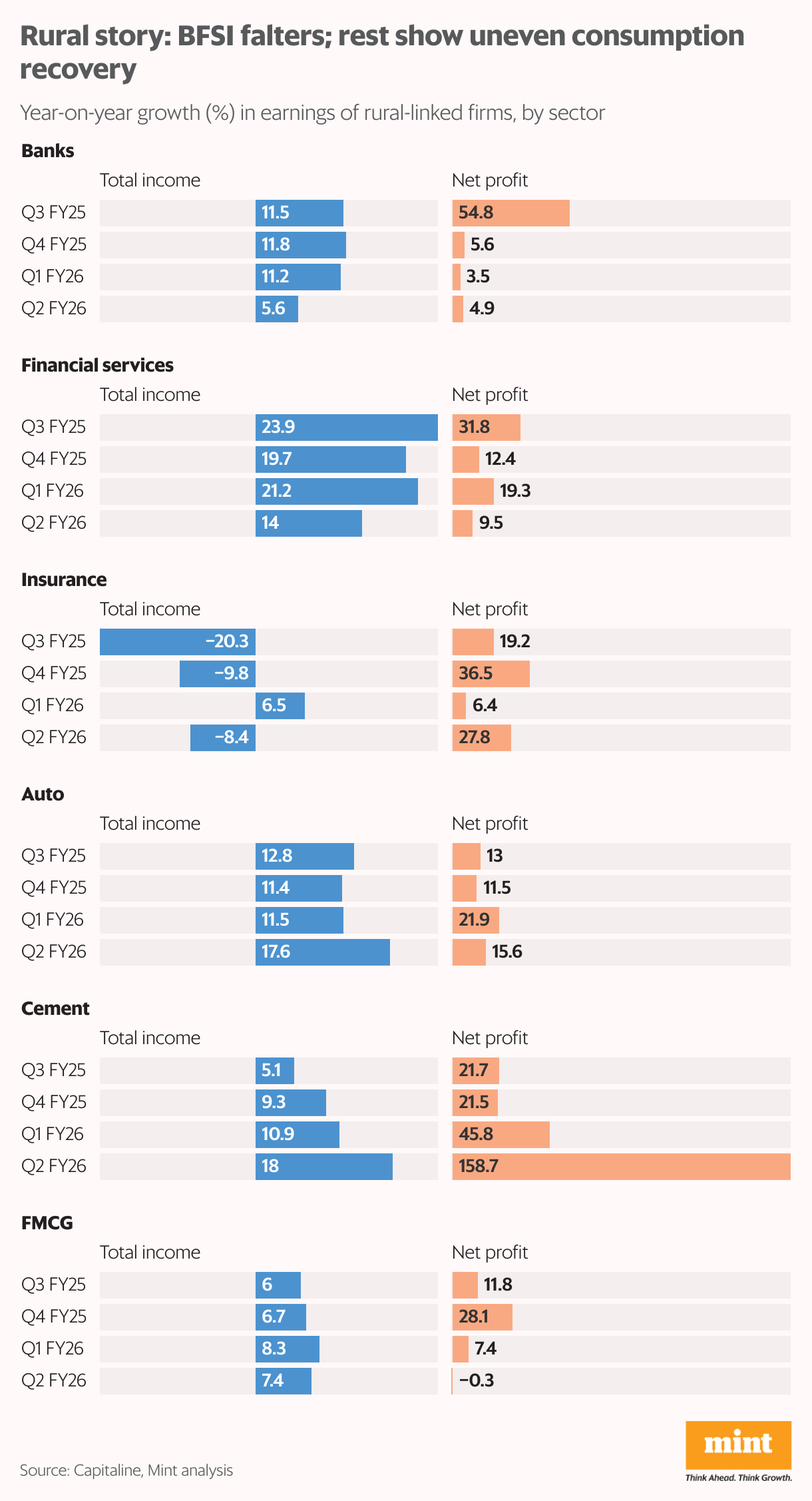

Experts link this resilience to strong auto, FMCG and cement volumes, aided by easing input costs, especially in FMCG. However, banking, financial services and insurance (BFSI) firms, which make up over a quarter of the index and nearly 60% of its total income, pulled down its overall topline growth.

The equity markets remain optimistic. The Nifty Rural Index has returned 15% so far in 2025, comfortably beating the Nifty 50’s 9% gain, suggesting that investors are still staying with the rural consumption story.

A sense of caution

Rural-focused companies are typically more volume-sensitive and quicker to reflect ground-level shifts in purchasing power, experts noted. A two-quarter slide in revenue implies that rural demand has not accelerated even after an ample monsoon and moderating inflation.

Procurement delays and softer food prices hit farm income in Q2, explained Anil Rego, founder and fund manager at Right Horizons PMS. This weighed on rural liquidity and the propensity to consume. As a result, “small-ticket credit demand for consumer durables, microfinance and gold loans has been subdued. This usually signals stress in lower-income cohorts,” he said.

Macroeconomic indicators such as y-o-y growth in passenger vehicle sales, housing loans, personal consumption loans and credit to industry were the slowest in four years in September, DSP Mutual Fund noted in its latest report. The demand lift typical of festive months was muted this year, except for utility vehicles and tractors, which stood out as rare bright spots, it added.

This suggests that rural households are prioritising productive assets over lifestyle upgrades, managing tighter budgets and exercising caution, according to Rego.

CIBIL’s Credit Market Indicator shows a clear softening in rural demand, said Rahul Gupta, chief business officer at Ashika Stock Broking. This translated into slower loan origination and muted banking and financial services earnings in Q2, he added.

BFSI drag

BFSI firms were the main drag on rural-linked companies’ earnings. The total income of banks in the group of 73 firms slumped to a nine-quarter low of 5.6% y-o-y in Q2, compared with more than 11% y-o-y growth in the previous three quarters.

Financial services companies grew their total income a healthy 14% y-o-y, but that paled compared to the 20-30% topline growth posted for eight straight quarters.

Insurance firms continued their fall, recording a y-o-y total income growth of -8.4%. Barring Q1 of FY26, when the segment recorded 6.5% growth, the previous two quarters also saw negative growth of topline of 10-20%.

“The broader slowdown in banking and financial services income was partly driven by a sharp deceleration in rural credit growth, which remained below overall systemic credit expansion,” said Rego of Right Horizons PMS.

Increasing write-offs in microfinance and small and medium enterprise portfolios, especially in flood-hit regions, has raised asset quality concerns among financial institutions, further choking disbursements, said Vinod Nair, head of research at Geojit Investments.

With rural liquidity tightening, growth in non-life insurance premiums like crop insurance, micro-insurance, and government-linked schemes which form 15-20% of rural-linked premiums, slowed further, noted Gupta of Ashika Stock Broking. This compounded challenges for an insurance sector already battling a weak product mix, a normalising base, and distributor adjustments after regulatory changes, he added.

Hence, slower retail loan growth, weaker agricultural disbursements, softer insurance premiums and muted deposit flows resulted in a muted September-quarter for BFSI, dragging down the Nifty Rural index, experts noted.

FMCG breather, sort of…

Significantly, FMCG (fast-moving consumer goods) companies saw a contraction in total income growth after rising for three straight quarters, recording 7.4% y-o-y growth in Q2, compared to 8.3% in Q1. Net profit growth, too, went into negative territory (-0.3%) for the first time in four quarters.

Still, FMCG sales growth of 7% came as rural volumes expanded twice as fast as in urban areas, said Nair from Geojit Investments.

Rego from Right Horizons added this steadiness masks weak rural incomes and stressed household budgets, which are prompting downtrading and softening volumes in mass-market categories.

“Rural demand is stabilizing, not accelerating, leaving FMCG prints steady but not broadly strong,” he added.

Uneven recovery

Other than FMCG, automobiles and cement sectors also emerged as the rural index’s core stabilisers in the September quarter, offering encouraging, although patchy, signals of recovery in the rural economy.

Auto sales climbed 18% year-on-year to a seven-quarter high in Q2, the analysis showed. Robust tractor sales, pent-up replacement demand and improved financing facilities for two-wheelers in rural and tier-3 markets boosted auto volumes, noted Right Horizons PMS’ Rego.

Even as consumption softened, rural and semi-urban construction stayed resilient on the back of housing demand, government infrastructure work and active individual homebuilders, Rego noted. As a result, the cement sector enjoyed volume growth of 18% year-on-year, albeit on a low base, the analysis showed. Yet, the sector’s sales grew the fastest in at least nine quarters and anchored the Nifty Rural Index’s earnings in Q2.

“While monsoons hit sequential volumes, underlying demand held up, supporting strong year-on-year growth,” he said. “Cement is effectively riding capex- and housing-led demand that’s less vulnerable to short-term consumption weakness.”

Tempered hopes

Although rural India ended the first half of FY26 on a muted note, experts remain optimistic that momentum will improve in the second half.

Rego said the worst of the slowdown is behind, as improving rabi crop prospects, easing inflation, and steady housing and road spending by the government should help stabilise rural incomes. He anticipates an uneven recovery in rural demand, with staples, building materials and two-wheelers likely to rebound earlier than discretionary or durables.

Even so, Geojit Investments’ Nair said that rural demand will lift India Inc only if it aligns with steady urban consumption and softer financial conditions, especially as food price deflation risks a hit to farm incomes unless crop output improves.

{kind=link}