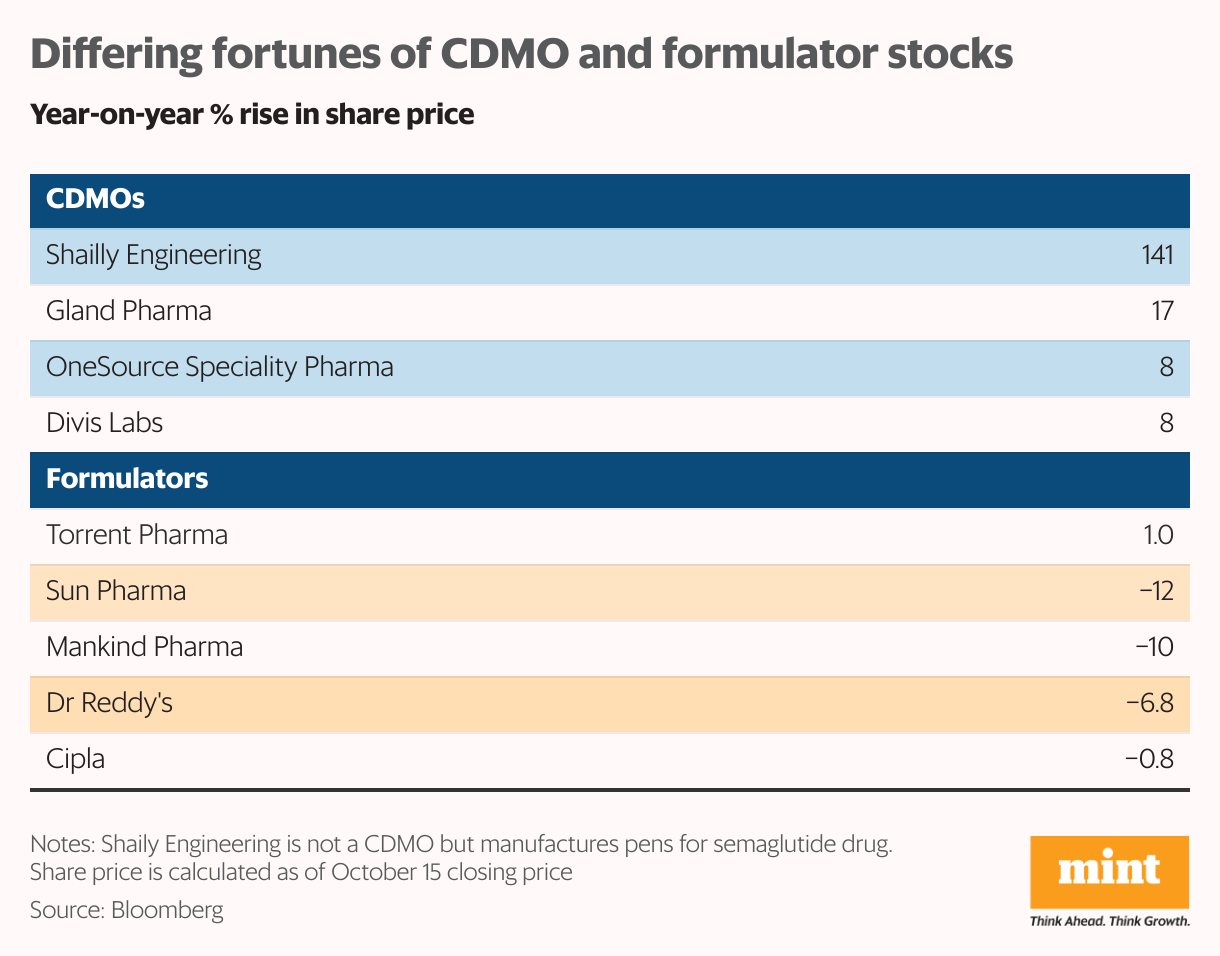

Investors are betting on these CDMOs as they are the earliest beneficiaries of the boom, having already acquired the capacity to produce these drugs. Shares of Indian contract development and manufacturing organisation (CDMO) companies such as OneSource Specialty Pharma, Divi’s Laboratories and Gland Pharma, which have the ability to manufacture these drugs, have jumped between 7% and 141% over the past year.

The global frenzy has also caught the attention of several large Indian drugmakers including Sun Pharma, Dr Reddy’s, Mankind Pharm and Cipla, which soon plan to launch copycat versions of semaglutide, which goes off-patent in several markets in March 2026. However, investors are betting that CDMOs will benefit first, and sentiment around these formulators appears muted, going by their share prices. Over the past year, shares of India’s top drug formulators have returned between -12% and 1%.

While drug formulators manufacture and market generic and specialty drugs, CDMOs partner with drugmakers to aid in research, development and manufacturing of drugs. Note that several large Indian pharma companies such as Dr Reddy’s have contract manufacturing capabilities as well.

How big is the opportunity?

Glucagon-like peptide-1 (GLP-1) agonists are a class of drugs used to treat type-2 diabetes and obesity. The most famous of these is semaglutide, which was launched by Novo Nordisk under brand name Ozempic in 2017 as an anti-diabetes drug. Researchers had observed significant weight loss as a side effect during trials. This discovery led to the development of higher-dose versions specifically for weight management, branded as Wegovy. Approved by the FDA in June 2021, it established semaglutide as a leading pharmaceutical treatment for obesity.

Both drugs have since driven a massive, global shift in the medical approach to treating both diabetes and obesity. GLP-1s are expected to become the biggest class of drugs in history, with annual sales projected to top $100 billion over the next five years, according to a September 2025 note by Morgan Stanley.

Novo Nordisk’s patent on semaglutide is set to expire in key international markets, including India and Canada, in March 2026, while the US patent is expected to expire around 2032. This has prompted major Indian drug manufacturers to prepare for the production of affordable versions, including the pen injectors used to administer them. Earlier this month Eli Lilly, maker of weight-loss drugs Mounjaro and Zepbound, announced a $1 billion investment in India, where it plans to tie up with contract manufacturers to expand global supply chains.

The global opportunity for GLP-1 contract manufacturing is expected to be worth $5-10 billion at its peak, Nuvama analysts wrote in a report on GLP-1s in April. “We have accounted for more than $40 billion of fresh global capex in GLP-1 manufacturing. This includes capex for manufacturing of drug substance, pens, packaging and fill-finish. Additionally, we observe innovators turning to CDMO players to secure supplies as stakes are high,” the Nuvama report said.

The market in India is expected to hit ₹2,000-3,000 crore in the next fiscal year as generics are launched, according to Nuvama analyst Shrikant Akolkar. “In India, most domestic formulators will largely make the drugs in-house or get APIs (active pharmaceutical ingredients) from Chinese players,” he said.

To be sure, there are other tailwinds for contract manufacturers, especially those engaged in early-stage research and development. The US Biosecure Act, a piece of legislation aimed at curbing American companies’ ties to certain Chinese biotechs, is back in focus. If passed, it could benefit Indian companies in the long run. Indian CDMOs are already investing in growing capacity and tech capabilities to position themselves against rival Chinese firms, anticipating a shift in global supply chains.

Why are CDMOs expected to be the early winners?

Vipul Bhowar, senior director, head of equities at Waterfield Advisors, said, “CDMO players are likely to be the first beneficiaries of the semaglutide opportunity because they are better prepared in terms of scale and capabilities. Most CDMOs have already undertaken aggressive capex and built up manufacturing and finishing capabilities, making them ready to capture the initial wave of demand once patents expire.”

“They have also been investing in new technologies and R&D to meet future requirements, giving them an edge over traditional formulators,” he added.

Generics companies currently lack supply visibility and will need time to develop semaglutide as they need regulatory approval first, said Sagar Lele, executive director at Paterson PMS. While they could start seeing healthy growth in the next few years, CDMO players stand to benefit the most until then, he added.

Bhowar of Waterfield Advisors said CDMO companies’ stocks aren’t expensive, but rather priced for perfection as the size of the opportunity justifies higher valuations. “If the story plays out they will be the actual beneficiaries. Select CDMO companies are not leveraged,” he added.

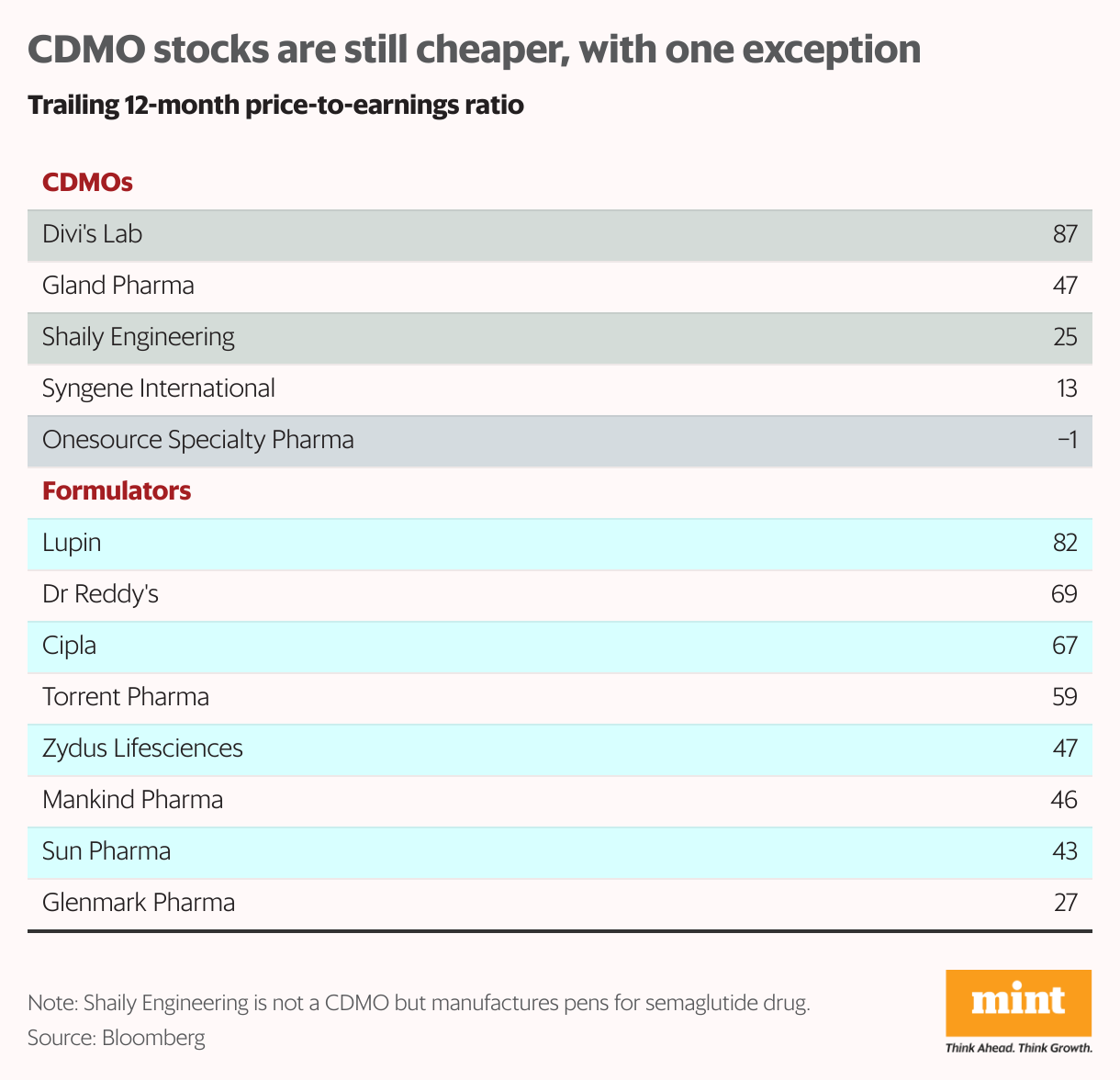

In fact, most CDMO companies’ stocks are trading at lower valuations than those of drug formulators. The exception is Divis Labs, which is trading at a trailing price-to-earnings ratio of 86.87. Elara Capital said in a report dated August 7 that while Divis remained the best-quality Indian CDMO firm, its valuation builds in narratives that are unlikely to materialise at the pace that investors expect. “The stock has run ahead of what the company can achieve in terms of growth in its existing business plus potential growth from GLP-1 agonists and the US Biosecure Act,” it added.

What are some prominent companies in the space?

Few companies have the capability to offer end-to-end services for manufacturing pen devices, which include drug product formulation and sterile filling into cartridges, followed by the highly specialised assembly, labeling, and final packaging of the complex electromechanical pen injector device itself, ensuring all processes meet stringent global regulatory standards.

OneSource Specialty Pharma is one of the few CDMOs with the ability to do this. “Our ongoing capacity expansion will allow us to scale from 40 million doses to over 220 million doses, depending on demand. We have already guided that our overall revenue in FY28 from organic route will be $400 million and drug device combination including GLP1s will be a significant contributor to this growth,” Neeraj Sharma, the firm’s CEO and managing director told Mint in an emailed response.

Brokerage Investec expects OneSource to increase revenue at 32% compound annual growth rate (CAGR) and profit after tax at a 100% CAGR over FY25-FY28, driven by strong growth in semaglutide.

Meanwhile, Shaily Engineering Plastics stands out as a maker of pen devices used to deliver these drugs. It isn’t a contract manufacturer but owns the intellectual property for these pens. Two-thirds of the players filing for generic semaglutide approval worldwide will be doing so in partnership with Shaily Engineering, chief strategy officer Sanjay Shah told Mint. “We are expecting substantial expansion in our healthcare vertical in the next three years,” he added.

The company can currently manufacture around 70 million pens a year? and aims to add capacity for another 50 million a year by the first quarter of FY27, according to domestic brokerage Dalal and Brocha.

Shaily Engineering said last quarter it was investing a total of ₹125 crore in capital expenditure for semaglutide pens. “We’re in discussions with multiple customers regarding volume commitments and capacity requirements for the next three to five years and will align our manufacturing capacity and global manufacturing footprint accordingly,” managing director Amit Sanghvi told investors in an August call.

Other players are also rapidly expanding capacity to make room for incoming GLP-1 demand. Gland Pharma is increasing its GLP-1 pen and cartridge capacity from around 40 million to 140 million units, while Syngene International, the contract research and manufacturing arm of biopharma giant Biocon, set up a dedicated lab for peptides in the previous quarter.

“Peptides are a fast-growing interventional modality, witnessed by the rapid emergement of the GLP class for the treatment of diabetes, obesity and a widening range of comorbidities,” managing director and CEO Peter Bains told investors in a July post-earnings call.

Dr Reddy’s has also indicated plans to act as a contract manufacturer for semaglutide in addition to selling its own generic product in several markets. “Dr Reddy’s will be the jack of the pack… if they start contract manufacturing for others, it could be sizable for them,” said Akolkar of Nuvama.

What’s the next milestone?

The next phase for GLP-1s is expected to be oral medicines. Several companies are working on developing effective oral versions of their weight-loss drugs, widening the scope for CDMOs to enter the fray.

Divi’s Laboratories is already believed to be working on ingredients for Orforglipron, Eli Lilly’s oral anti-obesity medicine under development, according to recent brokerage reports.

It has set up a small amount of capacity, which can be expanded multi-fold in future, Nuvama said in an August 28 note. “We believe CMOs have a $500 million to $1 billion peak opportunity, with Orforglipron peak sales likely to be $13-25 billion. We forecast Divi’s current capacity will add around $60 million of revenue, but at peak can be scaled up to $200-300 million,” the note read.

Divi’s has not confirmed its Orforglipron plans and did not respond to Mint’s queries on this.

“Divi’s Laboratories is working with several multinationals on peptide projects including GLP-1s, leveraging its strong backward integration as a key differentiator, with commercialisation expected within 12-14 months, subject to regulatory approvals,” said Nitant Darekar, research analyst at Bonanza.

{kind=link}