India’s home décor sector, which includes companies that produce plastic pipes, ceramic tiles, and wood panels, is currently facing significant challenges. Weak consumer demand, lower realizations, and margin pressure have depressed earnings and the industry’s performance.

Over the past year, shares of companies like Finolex Industries, Prince Pipes & Fittings, Kajaria Ceramics, Somany Ceramics, Greenply Industries, and Greenpanel Industries have fallen 20-42%.

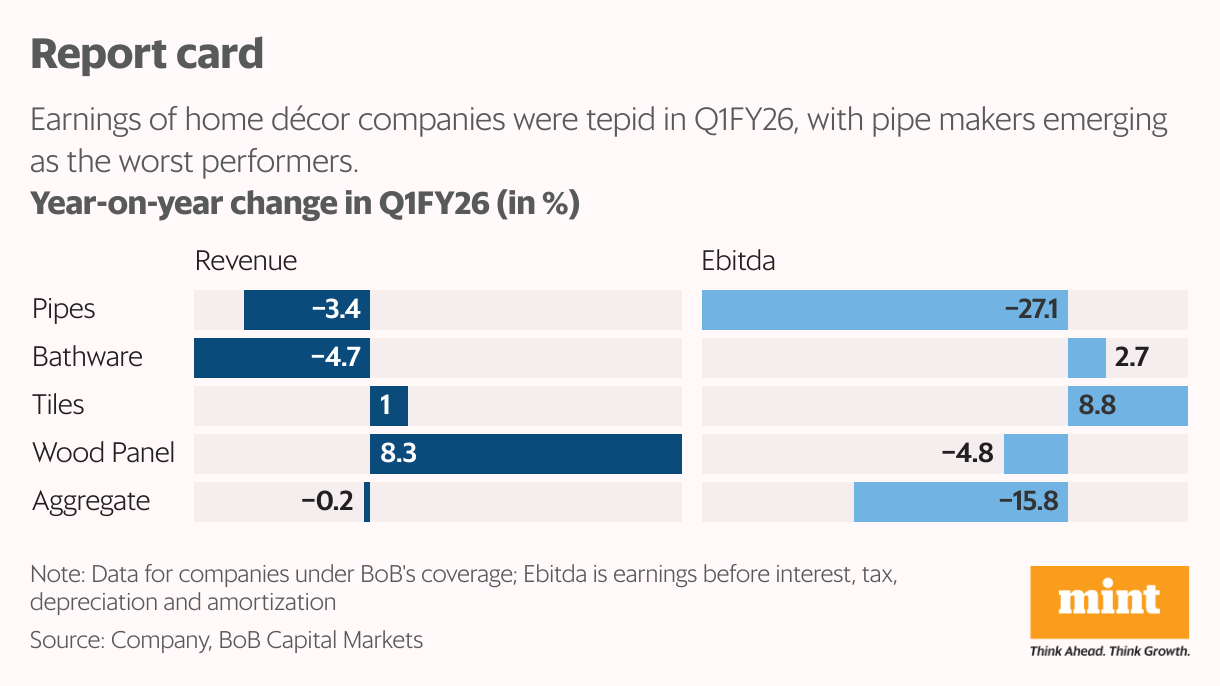

On an aggregate basis, 13 building materials stocks under the coverage of BOB Capital Markets saw muted revenue performance for the tenth consecutive quarter, down 0.2% year-on-year in the June quarter (Q1FY26). Ebitda margin compressed 204 basis points to 11%. High discounts offered to dealers across segments amid elevated competitive intensity in a soft demand environment hurt the sector’s margins.

The plastic pipe segment took a hit following the early onset of the monsoon, reduced government spending on infrastructure, and a high base effect from the previous year. Weak resin prices also played a role. However, the likely imposition of an anti-dumping duty on imported polyvinyl chloride (PVC) resin, a key raw material for plastic pipes, could drive re-stocking among pipe dealers. This could temporarily boost sales volumes and improve margins.

Movement of PVC prices is crucial for plastic pipe companies, as dealer decisions to destock or restock inventory are directly influenced by them. Despite the potential for a temporary boost from the anti-dumping duty, a lasting earnings recovery is unlikely without a significant increase in overall demand. Consequently, expectations from Q2FY26 are low, and it remains uncertain whether competitive pressures have reached their peak.

For wood panel companies, some relief comes from softening timber prices and reduced imports of medium-density fibreboard (MDF) due to stricter quality control regulations from the Bureau of Indian Standards.

However, new MDF capacity addition announcements are crucial. “We believe wood panel companies have near-term headwinds in the MDF segment due to high domestic competitive intensity,” said an ICICI Securities report dated 31 August.

Gradually, with better utilization of facilities, competitive intensity could reduce and profitability may improve. However, valuations here are full and offer limited upside, ICICI cautioned.

Amid weak retail demand and stiff competition from Morbi tile companies due to muted exports, listed ceramic tile makers are focusing on cost rationalization. The anticipated recovery in the individual home building segment from H2FY26 could aid demand, but margins could remain weak unless exports improve.

{kind=link}