India’s paint industry is shifting gears. With capex spending cooling, the battle for distribution, brand recall, and customer trust is intensifying. Established players and new entrants are vying for market share ahead of the festive season.

“For incumbents, utilisation is around 70%, while new entrants are still scaling up, so overall, the sector’s capital expenditure is expected to normalise from this fiscal. The focus has now shifted to distribution, with both incumbents and new entrants aggressively strengthening dealer networks and even directly engaging with painters,” said Poonam Upadhyay, director, Crisil Ratings.

Brand wars intensify

Paint companies are investing in product upgrades, innovation, backward integration, and advertising to boost brand presence.

Asian Paints Ltd, in an interaction with Nuvama Research, noted that competitors targeted small and medium dealers with higher margins last year. In response, it formed a dedicated team to win back dealers, already seeing some return. Berger Paints’ management in the June quarter (Q1FY26) earnings call noted that reduced incentives are hurting dealer margins and pushing them back to established brands. Kansai Nerolac India and Akzo Nobel India also report similar trends.

The paint industry’s high entry barriers— such as startup costs, complex regulations, and strong established brands— prevent new competitors from easily entering an industry and gaining grip. This means pricing alone cannot be a growth lever for newcomers. So, while a new company could get an initial distribution push by offering incentives, long-term prospects hinge on brand recall value.

Here, Birla Opus seems to be going full throttle.

“The company continues to expand its dealer network month-on-month and has seen enrolment of large dealers,” said Elara Securities (India) report dated 8 September. It is scaling-up with new initiatives, such as: paint assurance for one year (getting good acceptance among contractors and architects; PaintCraft, a painting service is launched and likely to scale-up across India; introduction of financing scheme to consumers, a first-of its-kind initiative; and exploring UltraTech’s network selectively, added the Elara report.

Festive season test

Usually, paint demand remains soft in the September quarter (Q2) due to rains, however this time the festival of Diwali is early versus last year. So, a lot of painting is expected to occur in the month of September.

In short, the run-up to the upcoming festive season would be a litmus test as paint makers woo dealers and potential customers. On the flipside, operating margin could come under further pressure.

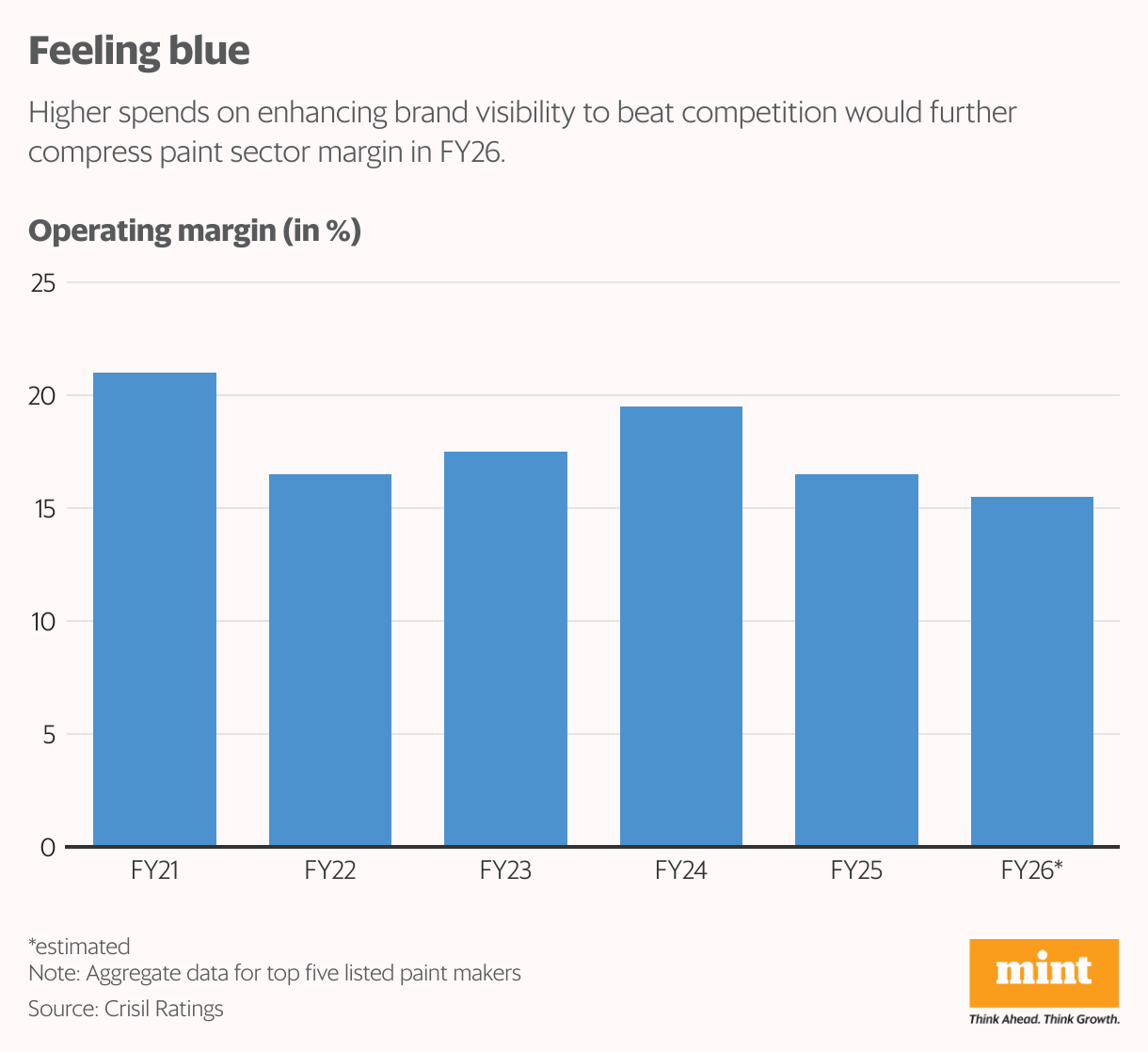

Margins in this sector are no longer just about fluctuations in crude-linked costs; intense competition has taken over as main pressure point, said Upadhyay. Operating margins dropped 300 bps in FY25 to about 16.5%, and Crisil sees another 100 bps fall in FY26 as companies spend heavily to defend market share, assuming input costs remain benign.

After a lacklustre Q1FY26 earnings season where paint companies saw muted volumes and margin, revival in volume depends on festive season demand. Q1FY26 gross margin impact was limited for paints as key input costs have remained benign.

“However, anti-dumping duty of 15-30% on Chinese titanium dioxide (TiO2) imports would have an adverse impact of 150-200 bps on gross margin from Q2FY26, which could be partly offset by deflationary TiO2 prices,” says Ambit Capital.

In this backdrop, shares of Asian Paints, Berger, and Kansai have taken a beating in the last one year, declining by 13-24%. Valuation multiples have also moderated, but they are not attractive yet.

{kind=link}