Nestle India Ltd’s return to double-digit growth after eight quarters in the three months ended September (Q2FY26) gives investors reason to cheer, but it also raises the bar for what comes next.

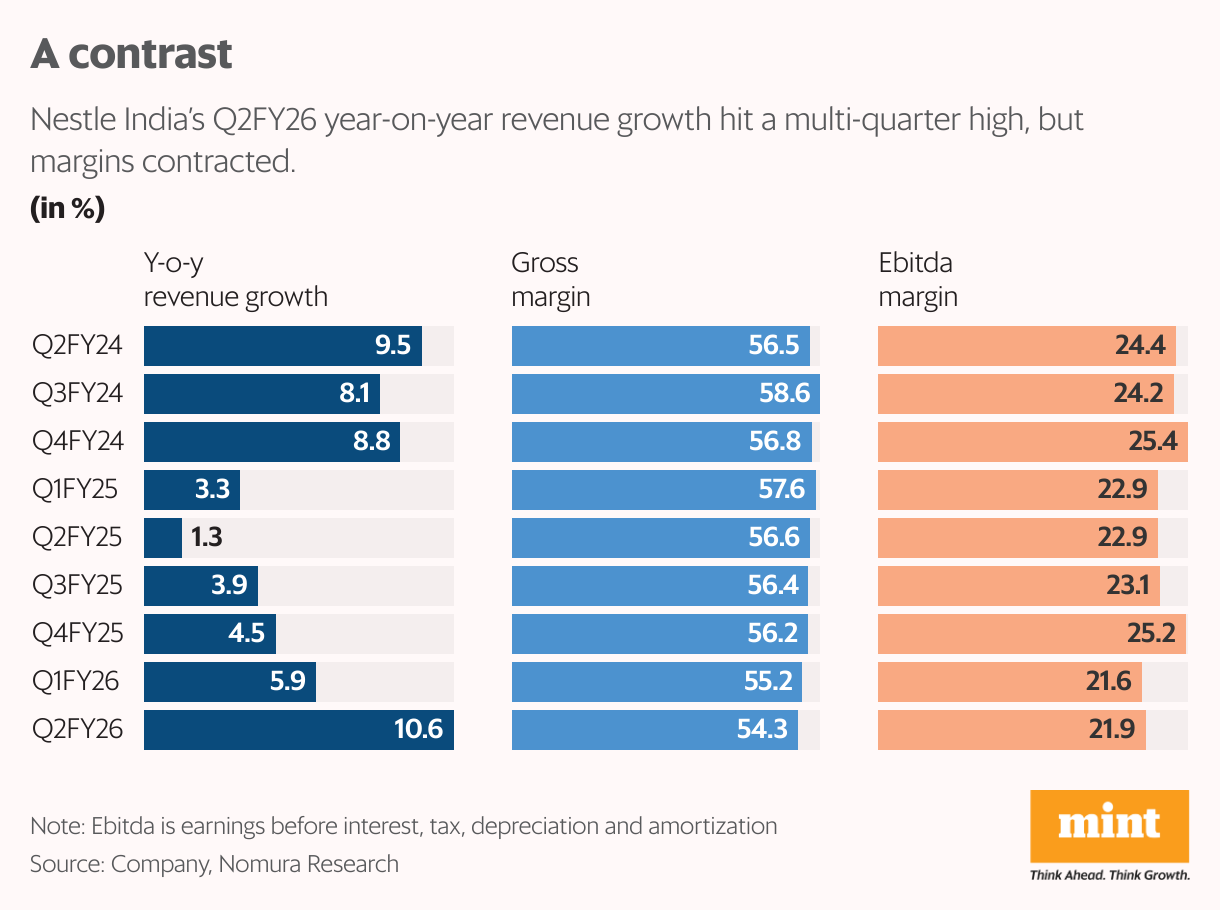

The stock touched a new high of ₹1,311.60 on 17 October after Q2 total operating revenue rose 10.6% year-on-year to ₹5,644 crore (domestic sales stood at ₹5,411 crore), ahead of most estimates.

The rebound was broad-based, led by prepared dishes, confectionery and beverages, each gaining ahead of the festive season. “We believe Nestlé’s new leadership will prioritize reviving topline growth; we evidenced this in Q2FY26, with domestic sales growth at 11% (driven by high single-digit volume growth; increased promotional activity likely supported the performance),” said Emkay Research. Q2 exports rose 14%.

Margins, however, tell a more tempered story. Gross margin slipped to 54.3% from 56.6% in Q2FY25 due to elevated input costs and lack of price hikes. However, a slower pace of growth in staff costs and other expenses meant the Ebitda margin drop was contained to 100 basis points year-on-year to 21.9%. Earnings before exceptional items and tax increased just around 1% to ₹1,029 crore.

The management expects easing inflation and a likely correction in milk prices after the festival season to offer some respite. While coffee prices could stabilize and cocoa may see a demand-led balance, edible oils are likely to stay firm. Emkay notes the company’s current margins are healthy and are unlikely to see material expansion ahead.

Gaining flavour

Meanwhile, the government’s GST 2.0 rollout, expected to simplify rates and lower levies on packaged foods, could boost consumption through the second half of FY26 (H2FY26). “About 85% of the company’s portfolio has benefited from the GST rate cuts,” pointed out Motilal Oswal Financial Services.

With pricing pressures abating, Nestle India’s next phase of growth would depend more on volumes than price hikes. With prices of three of the four key commodities turning favourable, Nomura Research expects quarter-on-quarter margin improvement from Q3 onwards, driving high-single-digit Ebitda growth in H2FY26.

The company is expanding across price points and geographies through a mix of affordability and premiumization. Smaller packs and targeted pricing strategies have helped increase market share in rural areas, while digital-first launches such as Maggi double masala and premium coffee offerings like Nescafe Gold and Nescafe Roastery continue to drive urban demand.

Confectionery grew at a strong double-digit rate, led by KitKat’s market-share gains, rural acceleration, premiumization, and higher in-home consumption via quick commerce.

Maggi spicy, masala-e-magic, and new launches under Purina Friskies (pet food) and Polo Sharebag added to the momentum. Pet food continued to post high double-digit growth, while ready-to-drink beverages sustained strong growth.

Nespresso’s availability on Amazon, alongside its website and Delhi boutique, reflects the company’s effort to enhance accessibility in the premium coffee segment. A new Maggi noodles production line at Sanand in Gujarat reflects Nestle’s confidence in India’s long-term growth story.

However, with a leadership transition following nearly a decade, all eyes will be on chairman and managing director Manish Tiwary’s strategy — how Nestle drives volume growth, protects margins, and scales newer categories such as pet food and ready-to-drink beverages.

The catch, of course, is valuation. At around 70 times FY27 estimated earnings, much of the optimism appears to be priced in. The company’s double-digit comeback may justify the current premium, but sustaining it will need consistent volume growth and stronger profitability in the coming quarters.

{kind=link}