SBI Cards and Payment Services is seen as a potential beneficiary of the Reserve Bank of India’s (RBI) revised risk weight-based capital adequacy norms. A draft circular in this regard was released on Tuesday. In reaction, SBI Cards rose intraday on Wednesday. The proposed rules aim to reduce capital requirements for all credit card issuers.

Currently, credit card outstanding dues worth ₹100 are treated as ₹125 by applying a uniform risk weight of 125%. Then, the Capital to Risk-Weighted Assets Ratio (CRAR) rate of 15% is applied to ₹125 to arrive at a capital requirement of ₹18.75. There is no bifurcation of ₹100 into dues from transactors and revolvers. Transactors are credit card users who use the card for transactions and pay their dues by the due date. Revolvers, on the other hand, try to pay only a partial amount or a minimum amount due and are willing to pay interest and late payment charges on the remaining dues.

RBI has proposed that the risk weight on transactor dues be reduced to 75%, as they do not pose as much credit risk as revolvers, whose dues should continue to attract a risk weight of 125%. For this purpose, transactors can be identified as those who fully paid their dues by the due date in the last twelve months. For SBI Cards, transactors accounted for 40% of outstanding dues for Q1FY26 and have remained steady for the last four quarters. Therefore, their blended risk weight will decrease to 105% (75% on ₹40 and 125% on ₹60), down from 125%, resulting in a minimum capital requirement of ₹15.75, or 15% of ₹105, compared to ₹18.75 calculated earlier. With lower capital requirements for transactors, card issuers will focus on high-quality customers with clean credit histories.

Shadow of bad debt

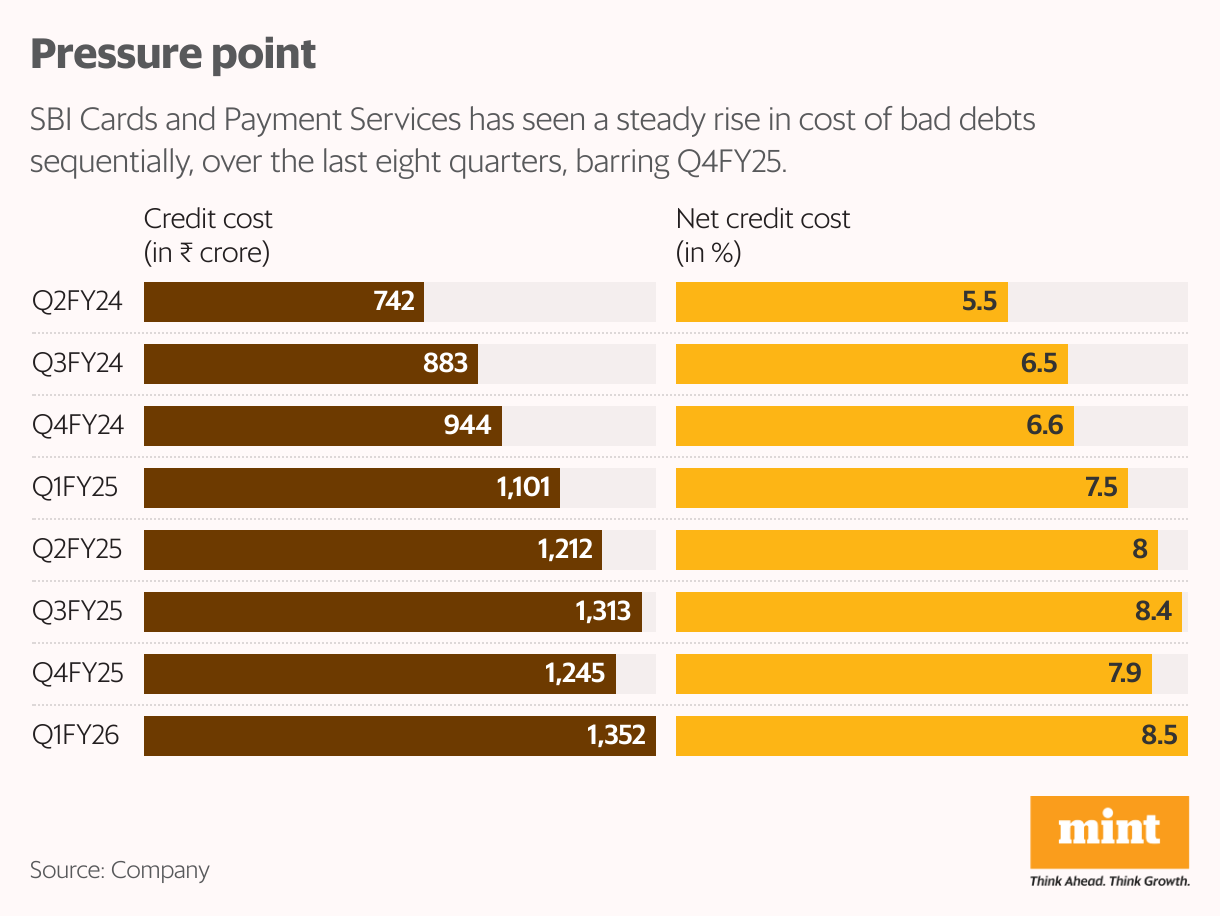

Additionally, the financial performance of SBI Cards and its share price returns have both been inconsistent. In 2025, the stock is up 40% but consistency is missing. Barring intermittent peaks, it has delivered returns of less than 5% compound annual growth rate (CAGR) since its public issue at ₹755 in March 2020, based on its current price of ₹921.75. Poor stock returns are the outcome of a high bad debt problem taking a toll on profitability. From Q2 FY24 to Q1 FY26, the gross credit cost as a percentage of loans has been steadily rising sequentially, from 6.7% to 9.6%, with the exception of Q4 FY25. Additionally, recoveries from past dues are not robust, as net credit costs also increased from 5.5% to 8.5% sequentially during the same period, except in Q4 FY25. So, SBI needs to keep delinquencies in check. After all, cardholders are choosing to default rather than revolving, i.e., rolling over the dues by paying only the minimum amount.

SBI Cards is taking some preventive measures, such as capping the credit limit of existing customers and ensuring the high quality of future card applicants. This is crucial because the credit card business is not immune to macro challenges of elevated household debt and excess leverage.

Capital adequacy

To conclude, capital was never a growth constraint for SBI Cards. In fact, its capital adequacy ratio has gradually moved up from 20.6% in Q1 FY25 to 23.2% in Q1 FY26, largely due to internal accruals. This is above RBI’s minimum capital adequacy ratio requirement of 15%. So, lower capital requirement is not a selling point here. Although SBI Cards has tailwinds of lower interest costs on its borrowings due to RBI rate cuts and likely increase in consumer spending following the GST rate cut, keeping bad debts in check remains critical.

{kind=link}