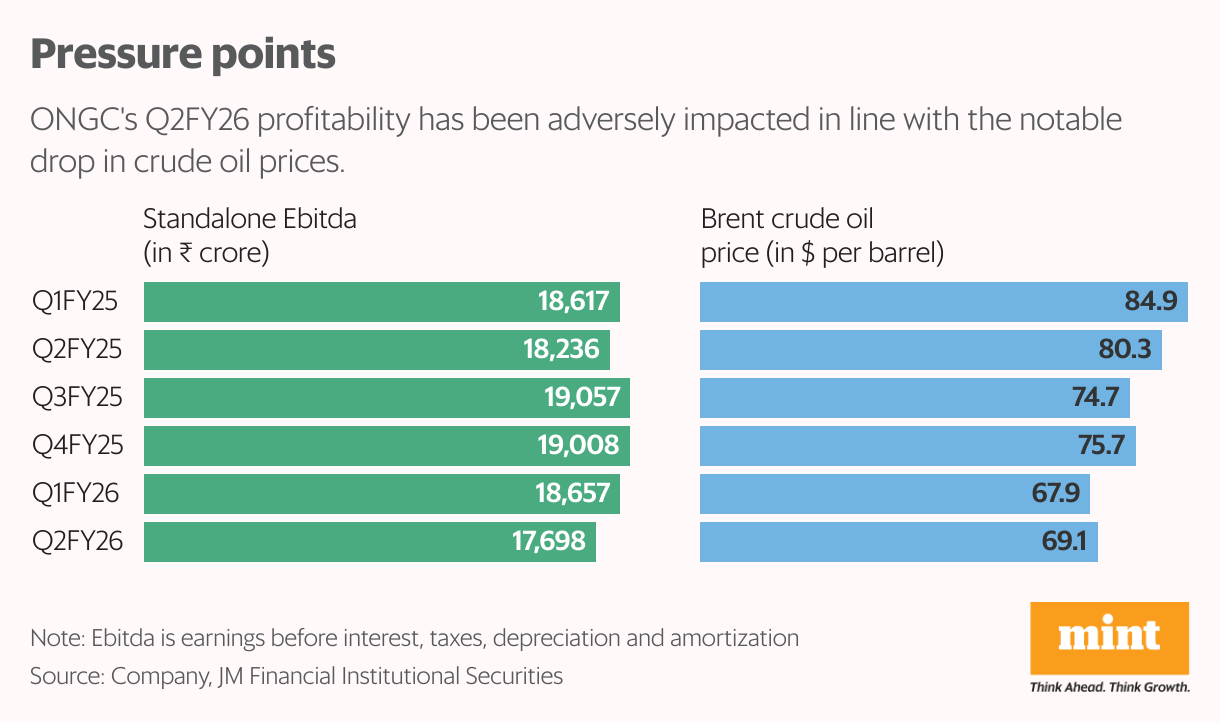

Oil and Natural Gas Corp. Ltd’s (ONGC) shares have stayed largely flat over the past year amid lower crude oil prices and stagnant volumes. Unfortunately for investors, the September quarter (Q2FY26) results hardly move the needle.

Standalone Ebitda, excluding forex transactions, declined about 3% in the September quarter (Q2FY26) to ₹17,700 crore. Despite improved gas realization and marginally higher sales volumes, falling crude prices and higher operating expenses weighed on earnings.

On the positive side, petrochemicals subsidiary ONGC Petro-additions Ltd’s (OPaL) recorded an Ebitda of ₹210 crore, against ₹10 crore loss in Q2FY25. OPaL’s profitability could further improve as capacity utilization is likely to surpass 90% vis-à-vis about 80% in Q2.

ONGC’s standalone Q2 revenue declined by 2.5% to ₹33,000 crore. Average crude oil realization (excluding joint ventures) fell 14% year-on-year to $67.3 per barrel. The decline was lower in rupee terms at about 10% due to currency depreciation.

Prices for nomination-based gas rose to $6.75 per mmbtu (million British thermal units) versus $6.5 per mmbtu in Q2FY25, as per the government’s pricing formula and would rise by another $0.25 per mmbtu from April.

Prices of new wells gas (NWG) fell by 11% to $8.4 per mmbtu, but higher volumes helped total gas revenue increase by 12%. Total oil and gas sales increased 3% to 8.7 million tonnes of oil equivalent (mmtoe).

NWG contributed 13.4% of Q2’s total gas volume, and this share is expected to increase to 30-35% over the next 3-4 years as new fields get commissioned.

To be sure, ONGC continues to struggle to accelerate its production. H1FY26 production (including share of JVs) at 20.4 mmtoe was down 0.2% year-on-year. Against this backdrop, the management has lowered its FY26 guidance to 40 mmtoe from 41.5 mmtoe earlier. ONGC’s FY25 production was 41.1 mmtoe.

Post results, some analysts have lowered their earnings projections and target price for the stock. Nomura Global Market Research has cut ONGC’s consolidated earnings per share by 14% and 17% for FY26 and FY27, factoring in lower volumes and crude realizations—which are partly offset by higher EPS for Hindustan Petroleum Corp. Ltd (HPCL). ONGC has about 60% stake in HPCL, which is seeing strong earnings growth, aided by low crude prices.

Ray of hope

Still, Q4 could see some uptick in volumes. The Daman field development is running ahead of schedule and should start contributing by Q4, the management said in the earnings call.

Construction of living quarters in the offshore KG Basin is expected to be complete by January, which will help ramp up gas production from the field.

The basin is now producing three mmscmd (million standard cubic metre) of gas, which is expected to rise to 10 mmscmd in FY27.

Also, British Petroleum has started work on Mumbai High fields as technical service provider, and expects to see better recovery from January.

JM Financial Institutional Securities estimates ONGC’s production to grow by about 6% over FY26-28, driven by KG basin and Western offshore blocks.

ONGC stock trades at an enterprise value of 4.7 times FY26 estimated Ebitda, according to Bloomberg. Amid subdued crude price environment, improvement in volumes would be key for the stock’s re-rating.

“Every $7 per barrel rise/fall in net crude realization results in increase/decrease in our EPS (earnings per share) and valuation by 12-18%,” said the JM Financial report.

{kind=link}