Data from the country’s largest stock exchange NSE shows that the number of investors trading with less than ₹10,000 each in index options fell 48% by the end of September from a year earlier.

The number of some of the bigger investors fell as well, though not at the same pace. Investors are categorized based on their share in options premium turnover.

The Securities and Exchange Board of India (Sebi) rolled out a series of steps to cool India’s options fever, effective first in November 2024 and then from July this year, after studies showed that the majority of them face steep losses.

The regulator is currently reviewing the impact of the latest steps in July, before it takes any fresh measures. The latest change in retail count is one of the key aspects the regulator will consider while determining the fate of weekly index option expiries, people aware of the matter said.

“Participation levels of small investors will form an important consideration in the Sebi analysis on additional measures in equity derivatives segment (EDS) post the July guidelines, the other aspects being retail investor losses, expiry day volumes relative to cash volumes (which in certain cases are as much as 700 times) and the quality of the derivatives curve, which shows the relative benefit of longer term contracts versus weekly contracts,” a person aware of the regulator’s thinking said on the condition of anonymity.

The count of investors on NSE trading with less than ₹10,000 each stood at around 450,000 as of September end, down 48% from around 860,000 in September last year. Investor count between ₹10,000 and ₹1 lakh turnover range saw a 32% decline to 780,000 from 114,000, NSE data showed.

The change in bigger traders’ count was relatively less to flat, with those trading between ₹1 lakh to ₹10 lakh seeing a moderation of 18.6% to 114,000 investors in September this year, against 1.4 million in September 2024. The counts of those trading ₹1-10 crore and those trading above ₹10 crore, who contribute to the bulk of turnover, remained flat at 160,000 and 10,000 respectively over the comparative period.

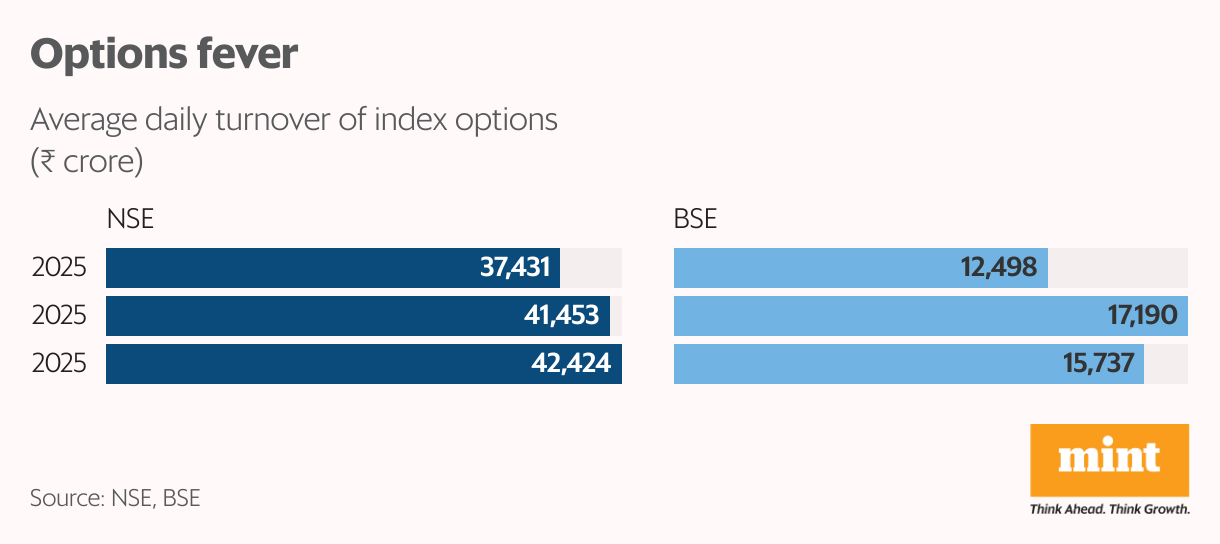

Sebi analyses derivatives data from both NSE and BSE before revising guidelines for the equity derivatives segment (EDS) . Similar data from BSE was not available. As of September end, NSE held 75.6% market share in premium turnover of equity options, with BSE accounting for the rest. Queries sent to Sebi remained unanswered.

Sebi’s first major wave of reforms, which included increasing Nifty contract size to 75 shares from 25 shares, imposing extreme loss margin on expiry day, and restricting weekly expiries to two from five earlier in the options space, took effect from November. A second wave of phased reforms began in July this year. These deal with changes in the calculation of open positions (outstanding buy-sell positions) to better reflect risk and imposing a gross limit for options exposure.

The regulator is expected to examine the impact of these measures from July through December before deciding on the pathway for weekly expiries, an industry official said.

“Recent regulatory changes in the derivatives segment have clearly started delivering the intended results, with a visible moderation in small-ticket retail participation,” said Pranav Haridasan, MD and CEO of Axis Securities.

Haridasan said this reflects a “maturing market” where participation is becoming more informed and risk-aware. “It will be important to observe how these behavioural shifts evolve over the next few months and let the data settle before any further structural changes are considered. Sebi, I believe, will take these emerging participation trends into account while evaluating the framework for weekly index options.”

The regulatory measures on derivatives came after the regulator revealed data on the massive losses faced by retail investors—9.6 million individual traders suffered an average loss of over ₹1 lakh each in FY25 versus 8.6 million traders losing an average of ₹86,728 each in the preceding fiscal, a Sebi report on 7 July said. Sebi also found that while individual investors’ turnover declined by 11% to ₹56,042 crore between December last year and May 2025 from a year ago, it still was 36% higher than ₹41,272 crore between December 2022 and May 2023.

The Sebi study in July coincided with the regulator passing an interim order accusing US hedge fund Jane Street of manipulating the Bank Nifty Index. Jane Street in September moved the Securities Appellate Tribunal (SAT) against Sebi for allegedly withholding crucial information from it during the investigation. SAT is expected to hear the appeal on 18 November.

Rajesh Baheti, MD and CEO of Crosseas Capital, expects Sebi to raise entry barriers for individuals in the derivatives space rather than banning weekly index options outright. He cited NSE IX’s launch of daily Nifty 50 option expiries in Gift City on 13 October to support his belief.

“Index options volumes here have already moderated post the recent Sebi measures and the order against Jane Street. Besides, daily options expiries have been allowed in Gift City. What makes daily option expiries a good product so long as Indians can’t trade them escapes the test of logic for me,” Baheti said.

Meanwhile, Sebi chairman Tuhin Kanta Pandey, at the Business Standards BFSI event on Friday, addressed the “sensitive subject” of equity derivatives, particularly the surge in weekly options trading. Citing the regulator’s own studies that highlighted significant losses for retail investors, he described Sebi’s strategy as a “calibrated approach” that followed market-wide consultations, aimed at containing the irrational exuberance of investors without stifling the market.

However, the chairperson ruled out any drastic measures. “Can we just shut down the market just like that? This is a very important question,” he stated, emphasizing the large number of participants in the equity derivatives space. He reassured the industry that any further steps would be taken only after public consultation and more data analysis to ensure a balanced outcome.

{kind=link}