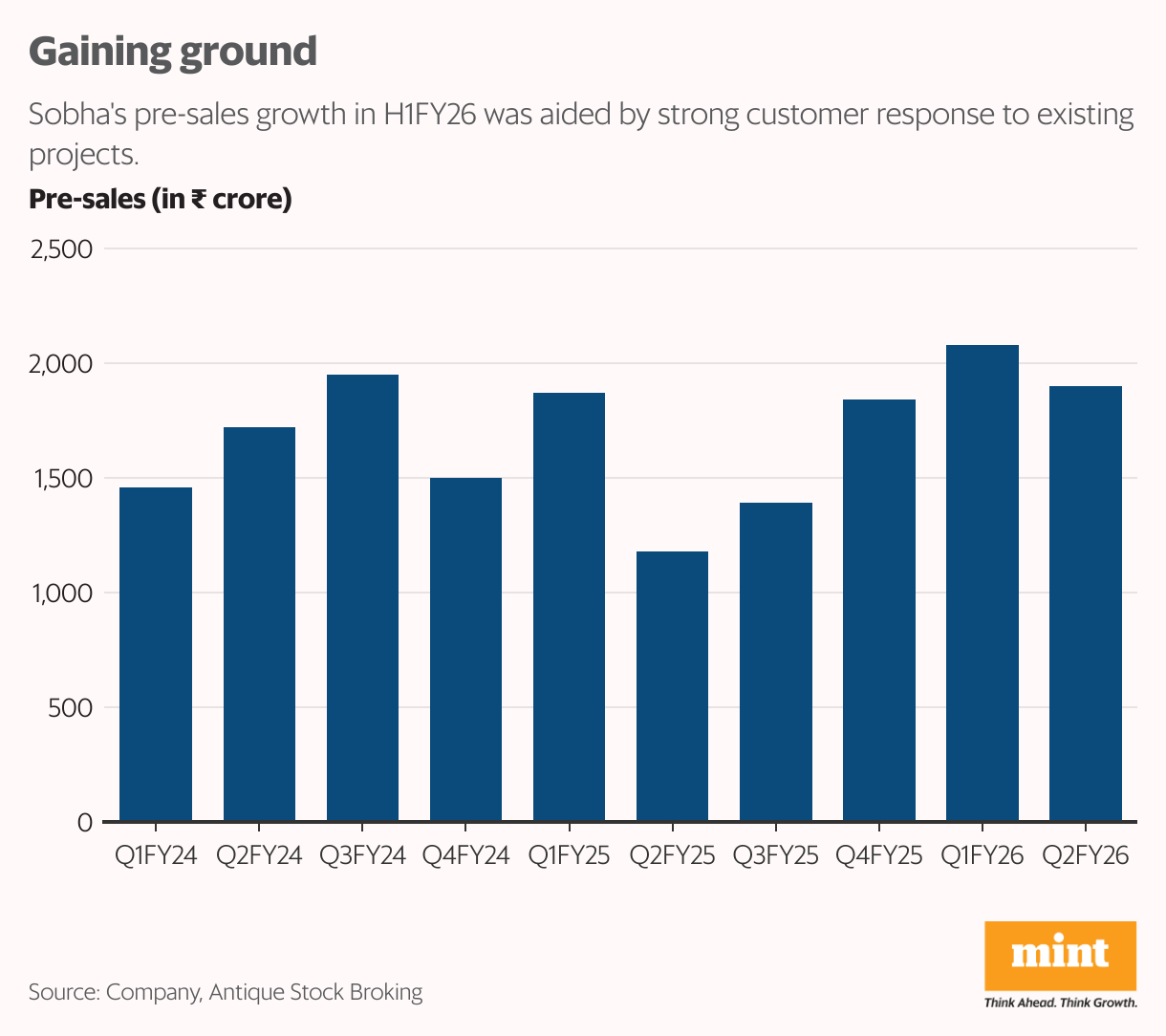

Realty developer Sobha Ltd closed the first half of FY26 (H1FY26) on a strong note, sustaining the pre-sales momentum seen in the June quarter (Q1FY26). Pre-sales, or bookings, in Q2 rose 61.4% year-on-year to ₹1,903 crore, taking the H1FY26 total to ₹3,981.4 crore against the FY26 target of ₹8,000-8,500 crore. This marks Sobha’s best-ever H1 pre-sales.

Strong absorption (sales) in the existing Sobha Town Park project in Bengaluru largely drove Q2 pre-sales. Sobha also launched a boutique luxury villa project in north Bengaluru, though there were no major new launches last quarter.

“The planned launch of Sobha Magnus (gross development value of ~ ₹900 crore) in Q2 has slipped to Q3 due to approval-related issues, which will be a key monitorable,” noted an Antique Stock Broking report dated 6 October. Had Sobha Magnus launched in Q2, the company would have crossed ₹2,000 crore in pre-sales for the second consecutive quarter, the report added.

Sobha’s Q2 sales by volume improved 49% year-on-year to 1.4msf and realization rose 8% year-on-year to ₹13,648 per square feet. Whether Sobha manages to surpass its FY26 pre-sales guidance, depends on the pace of new launches. The company has planned pan-India projects for the rest of FY26, targeting high-value markets of Mumbai Metropolitan Region, Pune, Greater Noida, and Gurugram Sector 63. Multiple projects are also slated for launch in Bengaluru.

Still, concerns linger over mass IT sector layoffs in Bengaluru, as the city accounts for much of the company’s residential demand, driven by technology sector employees. The management’s commentary on demand outlook will therefore be closely watched in the Q2 earnings call.

Interactions with property consultants in Bengaluru suggest that Sobha enjoys strong brand equity due to high quality developments, larger layouts, community living, and more end-user driven demand, said HDFC Securities. This gives Sobha pricing power. The HDFC report dated 22 September highlighted that Sobha’s pricing is 15-20% higher than peers and attractive payment plans seem to have helped sustain sales.

Sobha’s shares are down around 6% so far in 2025, though it fared better than the Nifty Realty index’s 15% drop. The company’s healthy balance sheet and cash flows offer some cushion, but pre-sales and launches trajectory remain key re-rating triggers.

{kind=link}