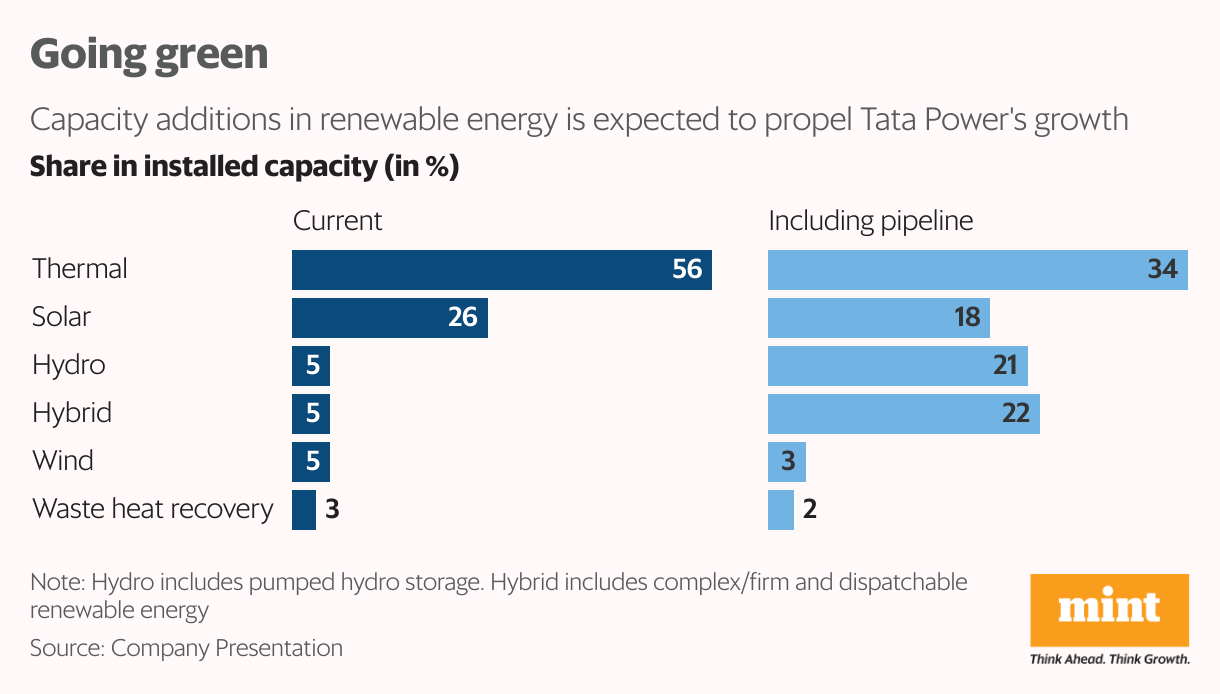

An old issue relating to the Mundra thermal plant has resurfaced for Tata Power Co. Ltd and is feared to further cloud its earnings prospects. In the September quarter (Q2FY26), a jump in profits for renewable energy (RE) and transmission and distribution (T&D) segments was overshadowed by the shutdown of the 4.2GW Mundra thermal power plant, which hurt overall performance.

Consolidated Ebitda saw modest 7% year-on-year growth at ₹3,500 crore, and consolidated revenue was flat at ₹15,500 crore. Ebitda is short for earnings before interest, taxes, depreciation, amortization.

The Mundra problem

The Mundra plant has been shut since July, following the central government’s withdrawal of its directive to operate it under Section 11 of the Electricity Act, 2003. The company was paid a regulated tariff on a cost-plus basis under the directive, whereas the plant’s original power-purchase agreement (PPA) is on a fixed-price basis, which is unviable at current coal prices. The management is in discussion with the Gujarat government for the execution of a supplementary PPA and hopes to arrive at an agreement soon.

The plant, with its associated business, recorded a loss of ₹12 crore at Ebitda level (including other income) in Q2FY26, against profits of ₹516 crore in Q2FY25. RE and T&D saw on-year Ebitda growth of 57% and 17%, respectively. RE profits were primarily driven by the cell and module manufacturing division, which saw a full ramp-up of its plant, with its Ebitda increasing 2.5x to ₹466 crore. The T&D segment got a push from the improving efficiency of Odisha discom with an on-year rise of 67% in its Ebitda to ₹687 crore, on a marginal increase of 8% in revenue.

The rising debt

Even so, Tata Power needs to remain watchful for its debt profile, considering some capital-intensive, high-gestation projects under construction. Among these are two pumped hydro storage projects, entailing a cost of about ₹13,500 crore. JM Financial Institutional Securities projects Tata Power’s total loans to increase to over ₹1.2 trillion by FY28, from ₹58,000 crore in FY25. Its net debt stood at ₹54,000 crore at the end of Q2FY26, up from ₹47,600 crore in Q1FY26.

Meanwhile, the Tata Power stock has remained nearly flat over the past one year and trades at an enterprise value of 12.2x its FY26 estimated Ebitda, shows Bloomberg data. Resolution of the Mudra plant issue is a key near-term trigger for the stock. For now, Nuvama Research cautions of a soft H2FY26 for the company due to continued losses at Coastal Gujarat Power Ltd (Mundra) and lower manufacturing profits on captive sales.

{kind=link}