It’s raining earnings downgrades for Thermax Ltd, an engineering and environment solutions company, after a dismal September quarter (Q2FY26).

Revenue fell 5% year-on-year to ₹2,474 crore, while Ebitda plunged 38% to ₹172 crore. The drag came from execution challenges and cost overruns in the Industrial Infra segment, which has been weighed down for nearly two years by old, low-margin government and refinery orders.

The segment declined 24% year-on-year, with margins collapsing to 1.6% versus 7.1% a year earlier. These legacy contacts—some taken at thin or even negative margins—have consistently dented performance.

Legacy clean-up phase

The silver lining: most of these low-margin orders are finally nearing completion, with only ₹570 crore remaining. Of this, 62% will be executed in H2FY26. A key problem project—the NRL refinery order—is also nearly behind them, with just ₹180 crore left. With a firm commitment to avoid such contracts going forward, Thermax expects to enter FY27 with a far cleaner project book than FY26.

Thermax termed Q2FY26 a “kitchen-sink quarter,” indicating it deliberately absorbed remaining costs from older projects to clear the slate. Kitchen-sinking refers to frontloading expenses, write-offs or losses into one period to reset profitability. Once the noise from legacy projects fades, core segments—Industrial Products, Green Solutions and Chemicals—are expected to show improved performance. Industrial Products is witnessing strong demand in water treatment, clean air systems, and data centre cooling.

TBWES (boilers and heat recovery steam systems) is entering a multi-year upcycle, backed by strong domestic order flows and improving visibility in the Middle East. Green Solutions continues to build momentum, with hybrid renewable projects, biomass boilers and CBG plants contributing more meaningfully each quarter. Even the Chemicals business—hit by global resin market pressures—expects utilisation and margins to improve from Q3 onward.

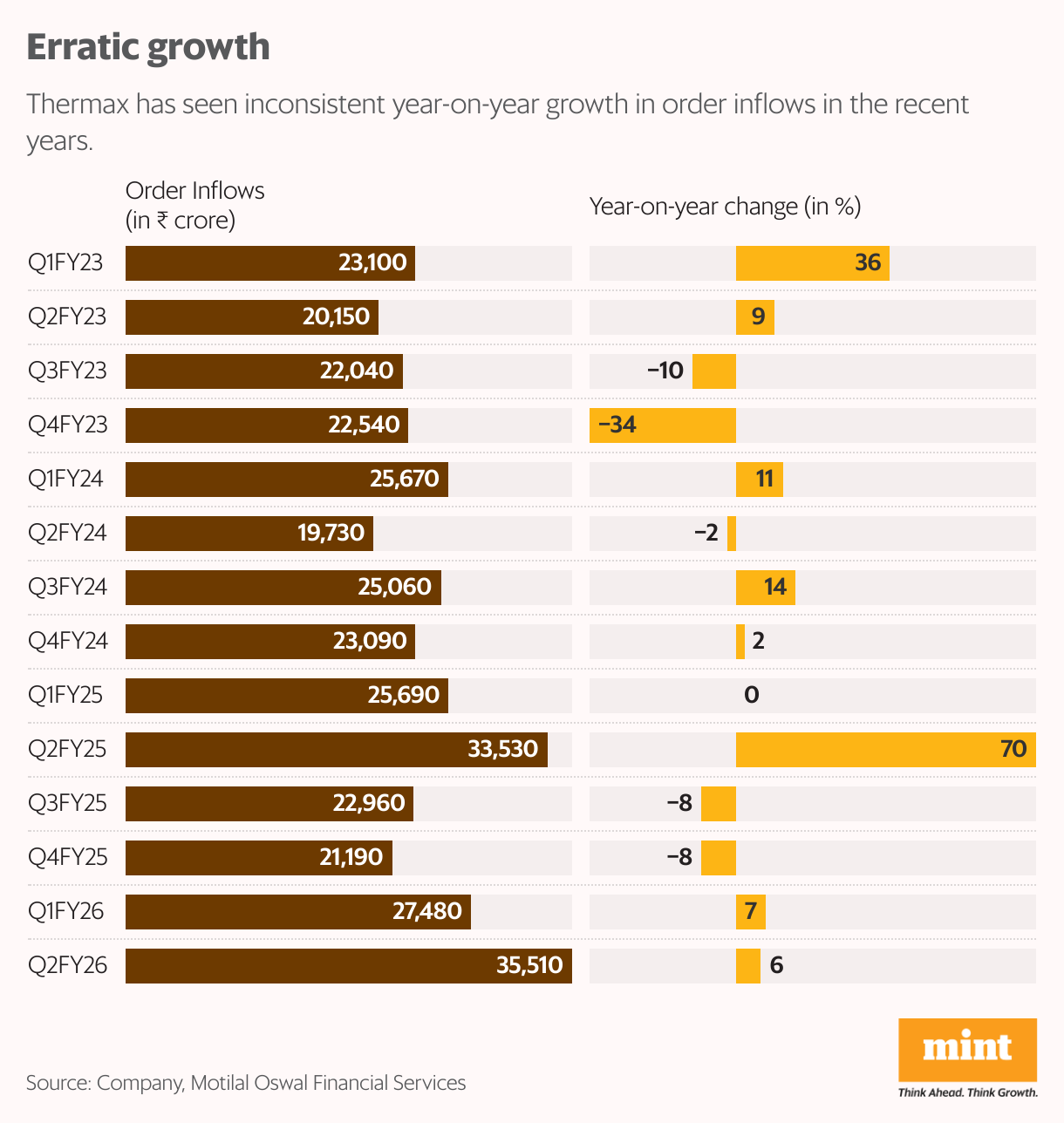

Order flow stays strong

Despite a messy quarter, order inflows rose 6% YoY to ₹3,551 crore, and the order book crossed ₹12,000 crore. The mix has also improved: Thermax is winning higher-quality industrial orders while consciously staying away from long-dated PSU projects that don’t compensate for risk.

Management expects full-year order inflows to rise more than 20%, driven by strong demand from power, metals, refining and petrochemicals. Large data centre opportunities are beginning to contribute meaningfully and could be recurring growth pockets through FY27–FY28. Order inflow growth in FY26 is expected at ~20% YoY, with a sharp pickup of up to 30% in 2HFY26.

Meanwhile, in CY25 so far, the stock is down 24% as investors struggle to digest ongoing challenges. It trades at around 37x FY27 PE, Bloomberg data showed.

“Timely project execution (especially for Industrial Infra), securing large-ticket size orders and margin recovery from current around 8–9% levels are key triggers,” said the Nuvama Research report. Right capital allocation, lower losses from FEPL, selective margin accretive order picking are other key variables, it added.

{kind=link}