Any loan for which the principal or interest payment is overdue for at least 90 days is called a non-performing asset (NPA). Gross NPA refers to the total amount of debt that has stopped generating income for the bank. Net NPA accounts for provisions – funds that banks or financial institutions set aside to cover potential future losses from loans that are likely to default.

High NPAs are an indication of poor financial health as they place a significant burden on a lender’s operations and threaten its stability. Here are five banks with high NPAs over the past five years.

#1 Punjab National Bank

The bank has a five-year average gross NPA ratio of 8.86% and a net NPA ratio of 2.88%. Its loan book is dominated by corporate debt, but micro, small and medium enterprises (MSMEs) and the agriculture sector account for the majority of NPAs.

For FY25, the gross NPA ratio was 3.95% and net NPA ratio at 0.4%. For the June 2025 quarter, gross NPAs stood at ₹42,600 crore and net NPAs at ₹410 crore. The bank has guided for a gross NPA ratio below 3% and net NPA ratio of 0.35% for FY26.

Gross and net NPAs have fallen consistently over the past few years on account of improvements in asset quality, aggressive write-offs, and a more stringent credit policy. Despite all this, PNB remains among the top banks with the highest gross NPA and net NPA ratios.

Net interest income increased at a compound annual growth rate (CAGR) of 7% over the past five years, while net profit clocked a 48.5% CAGR. Provisions decreased by more than half during this period.

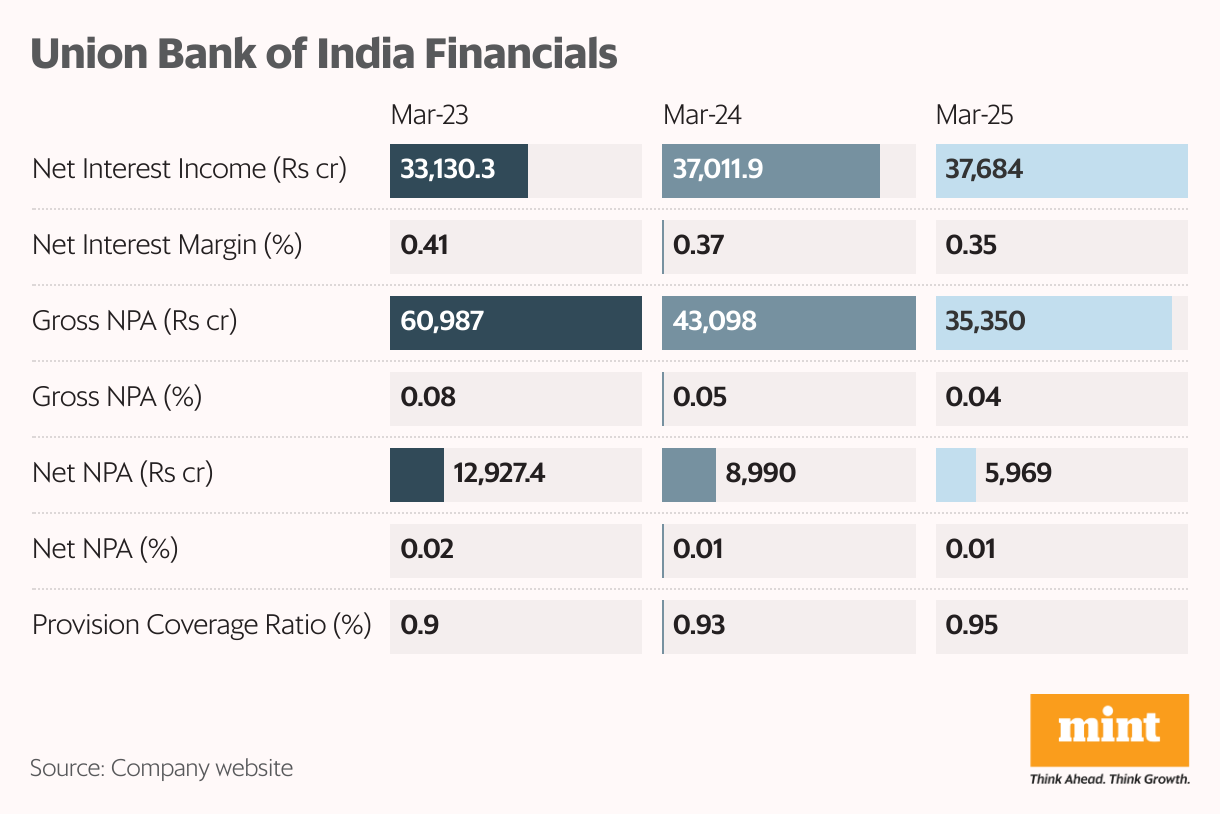

#2 Union Bank of India

The bank has a five-year average gross NPA ratio of 8.15% and a yearly average net NPA ratio of 2.33%. Union Bank of India’s loan book is dominated by retail, agriculture and MSME loans, which comprise 54% of total advances. Corporates are the next biggest segment, with securities rated ‘A’ and above comprising 85% of the corporate loan book.

In FY25, the bank’s gross NPA and net NPA stood at 3.6% and 0.63%, respectively, their lowest levels in the past five years. The primary reasons for this were aggressive write-offs, recoveries of bad debts, and a higher provision coverage ratio.

The bank is now in line with gross NPA guidance of less than 4%, and aims to improve this further through stringent credit policies. However, the total net NPAs have grown from ₹6,300 crore to ₹7,300 crore in just 12 months, primarily due to new NPAs added during the year. Nevertheless, the bank is taking measures to ensure its asset quality remains intact. It also increased its provision coverage ratio by two percentage points to accommodate new bad debts.

Net interest income and net profit increased at a CAGR of 8.7% and 44.5%, respectively, while the provisions fell slightly, indicating improving asset quality.

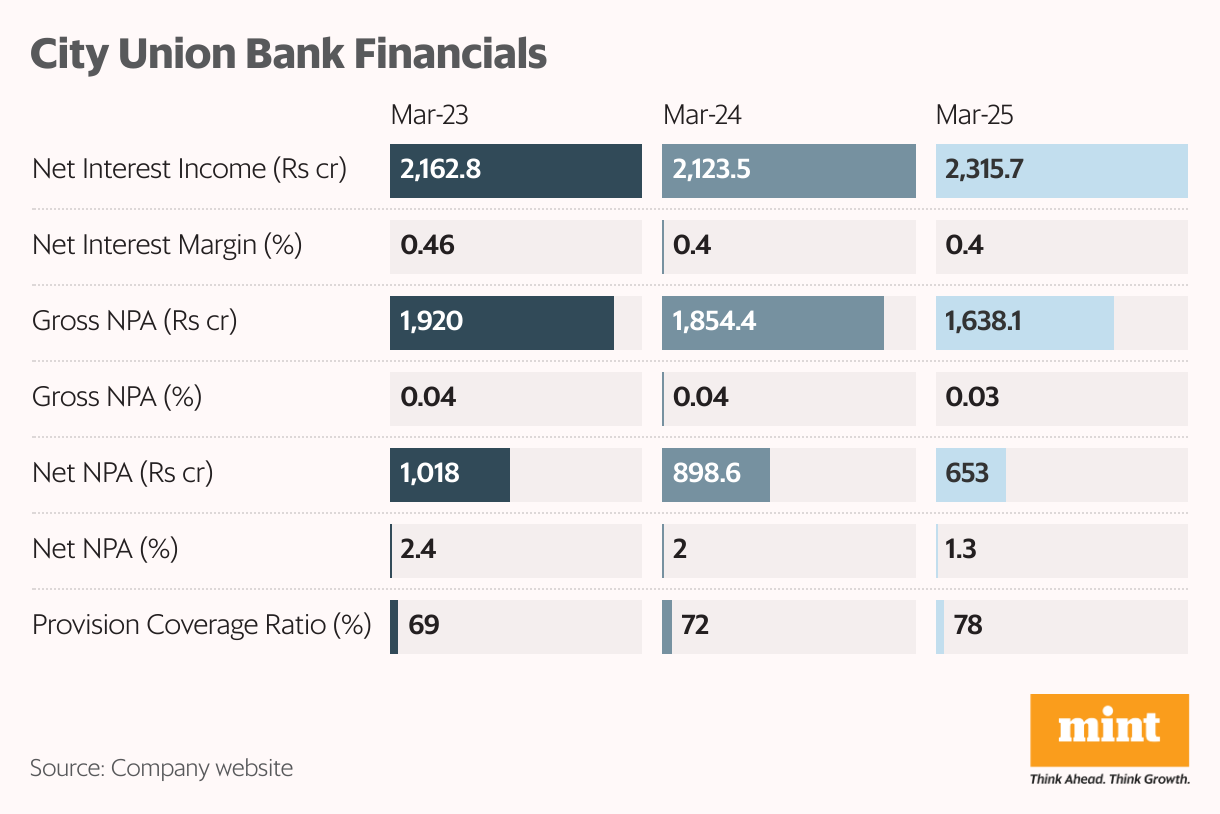

#3 City Union Bank

The bank has a five-year average gross NPA ratio of 4.25% and a yearly average net NPA ratio of 2.3%.

In FY25, the gross and net NPA ratios stood at 3.1% and 1.2%, respectively. Gross NPAs fell considerably from ₹1,850 crore to ₹1,630 crore, while net NPAs fell from ₹890 crore to ₹650 crore.

The bank’s loan book is dominated by MSME loans, followed by agricultural loans. Both categories have higher NPAs than others. Although the bank’s asset quality has been improving over the last few years, it expects slippages to be around ₹700 crore in FY26. Hence, the provisions are expected to increase slightly for the year.

City Union Bank has been taking extensive measures to improve its asset quality with a strict loan recovery policy and credit risk management policy.

This has improved its financials. In the past five years, the bank’s net interest income and net profit increased at a CAGR of 4.8% and 13.7%, respectively, while provisions fell by more than ₹300 crore, indicating a healthy loan book.

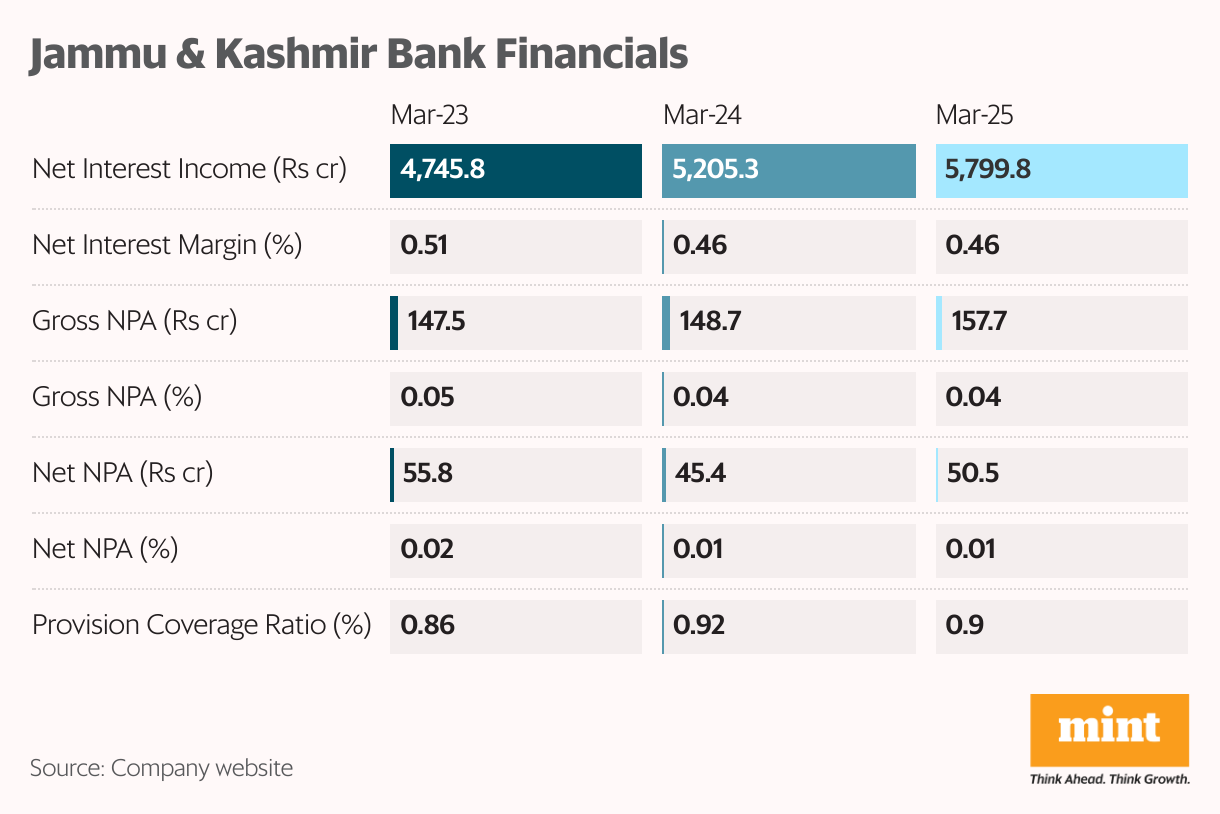

#4 Jammu & Kashmir Bank

The bank has a five-year average gross NPA ratio of 5% and a yearly average net NPA ratio of 2.15%. In FY25, the gross and net NPA ratio stood at 3.8% and 1.25%, respectively, down from 4.1% and 1.3% in FY24.

The bank’s loan book is dominated by retail, MSME, and agriculture advances (70%), followed by corporate advances (30%). Within the corporate advances, 60% of the borrowers are rated AAA. In the retail, MSME, and agriculture advances category, the majority of the bad debts are in the agriculture and MSME categories.

The bank’s asset quality has been improving on account of loan recoveries, upgrades and lower slippages. However, in the June 2025 quarter, the slippages increased on account of high bad debts.

Net interest income and net profit increased at a CAGR of 9% and 37.2% in the past five years, while provisions fell slightly on account of stable asset quality.

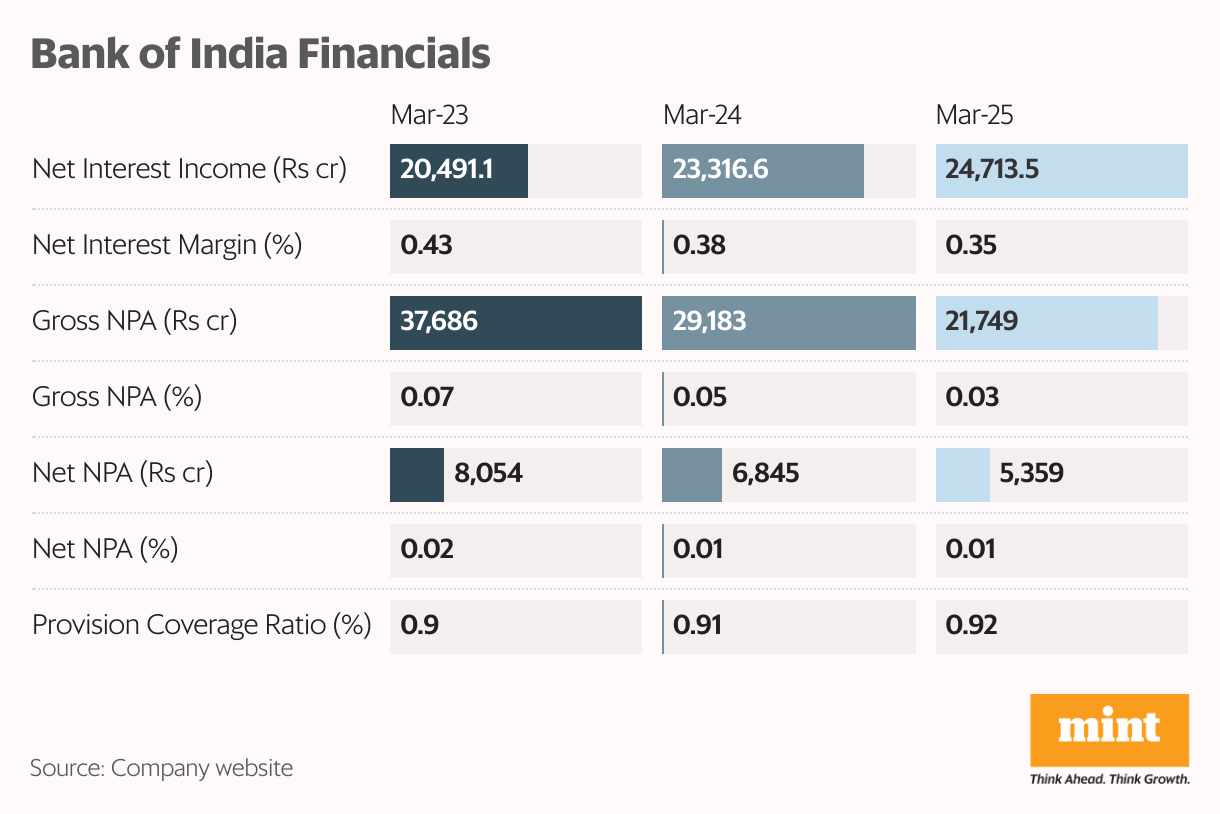

#5 Bank of India

The bank has a five-year average gross NPA ratio of 6.57% and a yearly average net NPA ratio of 1.54%.

Bank of India’s loan book is dominated by agriculture, MSME and retail loans. With respect to corporate loans, the majority of the rating profile is dominated by AAA-rated securities (72%).

In FY25, the bank’s gross and net NPA ratio stood at 3.27% and 0.82%, respectively. Slippages were also high during the year. However, owing to write-offs and recoveries, gross NPA and net NPA ratios fell slightly from the previous year. Management is optimistic about reducing gross and net NPAs ratios further and has guided for a net NPA ratio of 0.7% in FY26.

Net interest income and net profit increased at a CAGR of 11.4% and 35.6% in the past five years, while provisions remained stable at ₹7,800 crore.

Conclusion

Gross NPA ratios and net NPA ratios of these banks have fallen significantly over the past five years. This is mainly because during 2015-2018, the Reserve Bank of India (RBI) reviewed the asset quality of banks and discovered a large amount of bad loans.

With the worst already behind banks, the RBI and government have taken steps to reduce NPAs through capital infusion, aggressive write-offs, high provisions, recoveries under the Insolvency and Bankruptcy Code, and improved lending practices.

In addition, corporate deleveraging and an economic recovery have pushed NPAs down to multi-year lows, strengthening the Indian banking sector.

That said, one must be cautious about banks with high NPAs. It is always better to invest in those with consistently growing interest income, declining NPAs, and improving net profit.

Happy investing!

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com

{kind=link}