With a client base boasting marquee names such as Lowe’s, Ferguson Enterprises, Moen, and Kraus USA Plumbing, in addition to Karran USA and Ikea, it holds a strong position in the global quartz sink market.

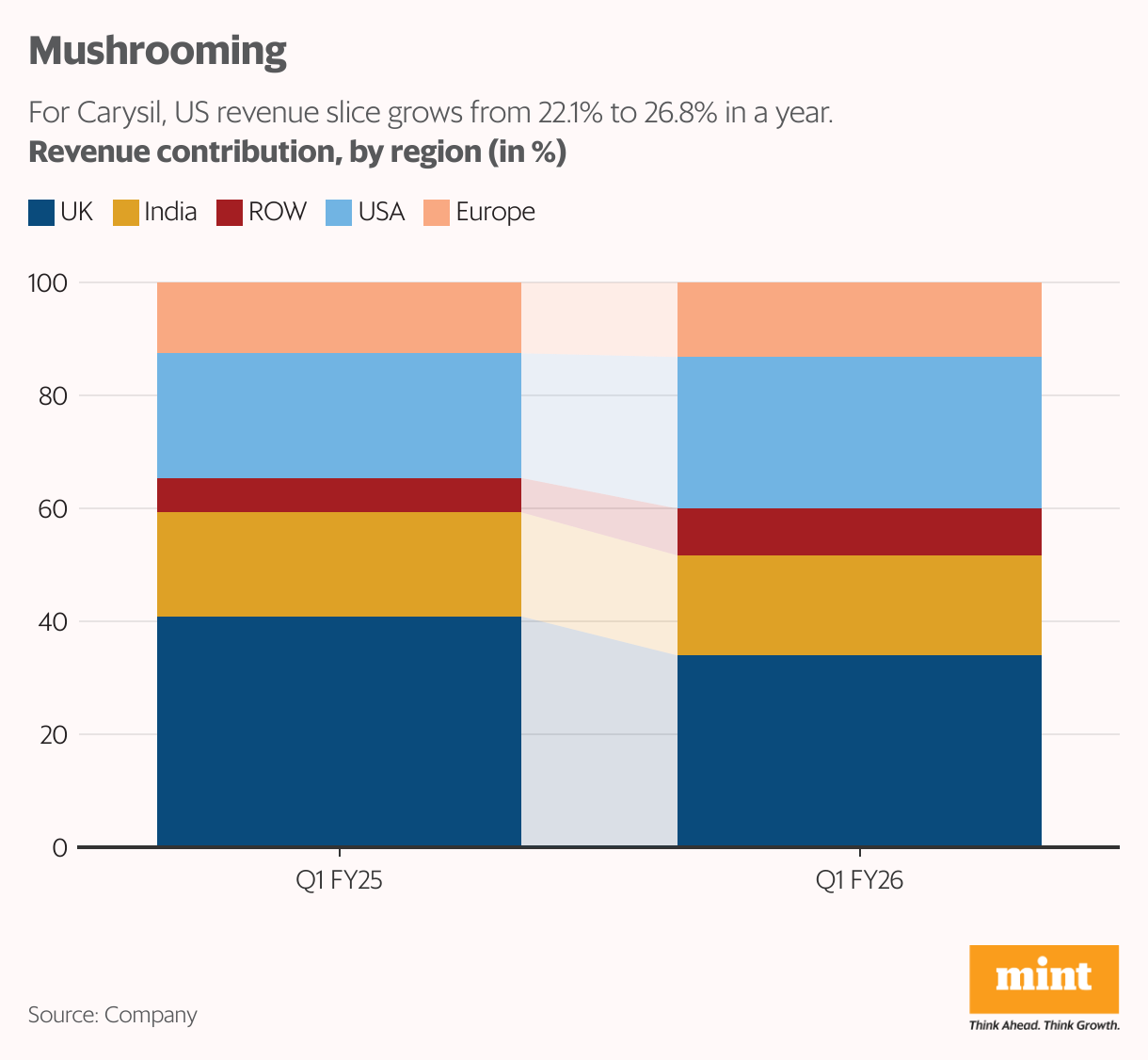

However, since exports dominate the sink maker’s revenue—with little over a fourth of it coming from the US market—investors are closely monitoring the impact of the Donald Trump-led administration’s 50% tariff on India on the stock.

The key worry is whether the rally would lose steam.

The US imposed a 25% reciprocal tariff and an additional 25% punitive tariff on India for buying Russian oil. While Carysil passed the first 25% levy on to customers, it may absorb a portion of the incremental 25% to preserve relationships, said financial services provider Monarch Networth Capital in its 8 September report after meeting the company’s management.

“However, despite US tariffs rising sharply to 50% (vs ~23% earlier), the management expects limited impact given a) 10-15% landed cost advantage versus peers and b) meaningful passage of the tariff increase to its end-user,” it said.

Sandeep Raina, head of research at financial services firm Nuvama Professional Clients Group, doesn’t expect Carysil to be hit too hard by the US duties.

He said the company can pass on part of the cost to customers since there is no real like-for-like competitor in India. Plus, global rivals such as Blanco, Franke, and Schock already price their products 30-40% higher, so even after tariffs, it still looks like a bargain.

Deven Kulkarni, senior analyst at portfolio manager Marcellus Investment Managers, which still owns Carysil in some of their funds, highlighted that “At 25% tariff, it is still cheaper than its peers in Europe (subject to a 15% tariff) and Canada (subject to a 35% tariff). However, at a 50% tariff, we expect it will give up some of its margins to protect the business”.

Plus, Carysil is widening its portfolio to include more appliances and faucets, categories that are increasingly manufactured in-house, thereby boosting pricing power, efficiency, and margins.

With exports de-risked, appliances picking up pace, and stainless steel gaining traction, it is steadily becoming a business with multiple growth drivers, according to market participants.

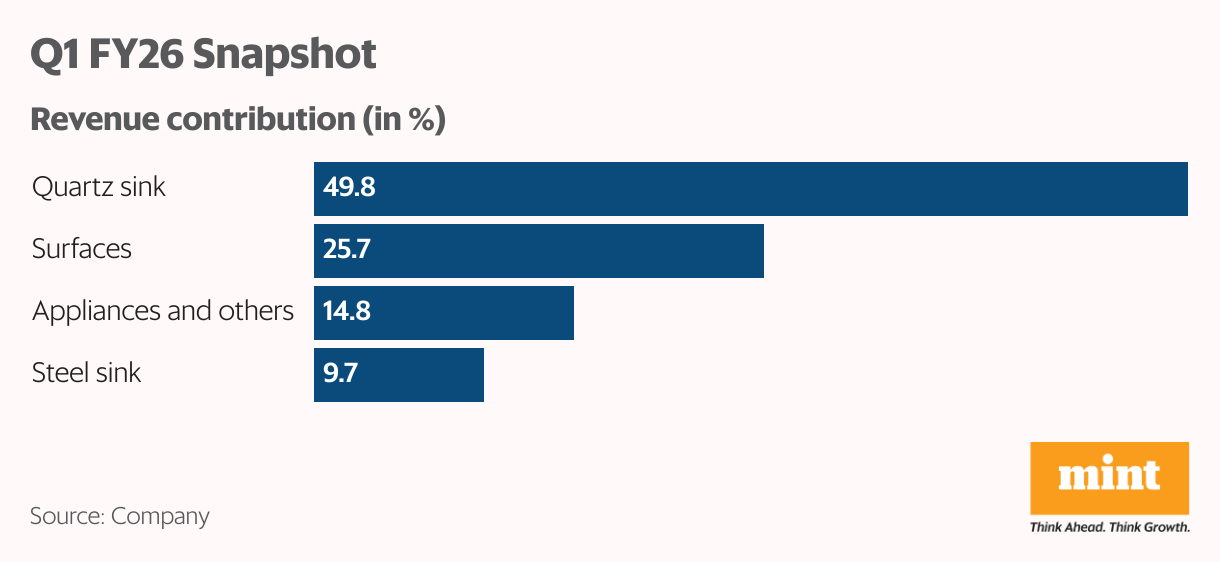

The latest investor presentation showed that quartz sink volumes rose 22% year-on-year in the June quarter, steel sinks 9.4%, and kitchen appliances, faucets, and tiles a stellar 60%.

Queries sent to Carysil remained unanswered.

Investor appetite

Investor interest in the stock is hard to miss.

Domestic institutional investors’ (DIIs) stake has risen to 11.19% as of the June quarter from 7.2% a year ago, while foreign institutional investors (FIIs) more than doubled their holding to 1.55% from 0.7%.

“The majority of the increase in DII stake is due to qualified institutional placement (QIP) of ₹121 crore in 2024-25 to raise money mainly for capacity expansion and loan repayment,” said Kulkarni of Marcellus Investment Managers. DSP Mutual Fund and Ohana India Growth Fund were the largest investors in the QIP, he added.

Besides, Sunil Singhania’s Abakkus Emerging Opportunities Fund-1 held 5.34% and Ashish Kacholia 3.52% of the sink maker as of the June quarter, according to the BSE shareholding data.

Kulkarni explained that the key reason for the sentiment improvement is big order wins. In March 2025, Carysil secured an order of 150,000 sinks per annum from Karran USA on behalf of US retailer Lowe’s. Deliveries began in May 2025.

To be sure, 150,000 sinks make up approximately 25% of 2024-25 quartz sink volumes, he explained. “So, at current realization per sink, the order can contribute around ₹80-100 crore to the company’s revenue (10-12% of total 2024-25 revenue).”

Valuation check

Raina said valuations remain attractive despite the stock’s rally, and if there’s no fresh tariff shock, the rally still has legs. “There’s still scope for a rerating,” he added.

The stock is trading at a price-to-earnings ratio of 37.9X, well above its five-year average multiple of 31.65X, according to Bloomberg.

He expects the company’s top line to record a 15-18% compound annual growth rate over the next two years, with a bottom-line growth of as high as 35-38%, thanks to margin gains.

Red flags

Near-term risks arise not only from tariffs, which could squeeze margins, but also from second-order effects on US consumer demand.

Over the medium term, the company is expanding into adjacent categories like faucets and kitchen appliances in India, but faces stiff competition in both categories from strong existing brands, market participants noted.

Its two acquisitions—solid surface fabrication firms UK-based Slymar in April 2022 and US-based United Granite in October 2023—are also in very competitive markets.

While performance in Slymar has been good, United Granite has been a loss-making entity since its acquisition in 2023-24, and the path to profitability remains uncertain, more so due to tariffs, said Kulkarni of Marcellus.

{kind=link}