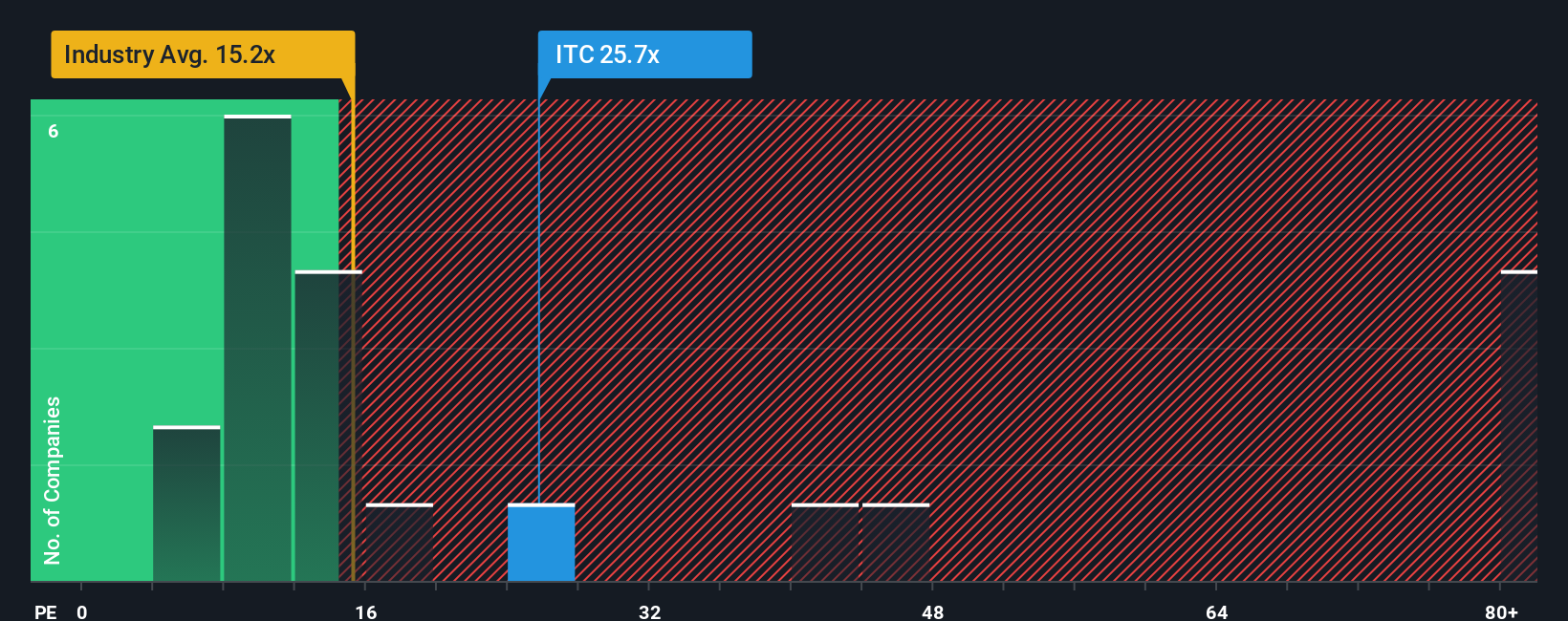

It’s not a stretch to say that ITC Limited’s (NSE:ITC) price-to-earnings (or “P/E”) ratio of 25.7x right now seems quite “middle-of-the-road” compared to the market in India, where the median P/E ratio is around 27x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

ITC hasn’t been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. One possibility is that the P/E is moderate because investors think this poor earnings performance will turn around. You’d really hope so, otherwise you’re paying a relatively elevated price for a company with this sort of growth profile.

View our latest analysis for ITC

Want the full picture on analyst estimates for the company? Then our free report on ITC will help you uncover what’s on the horizon.

Is There Some Growth For ITC?

There’s an inherent assumption that a company should be matching the market for P/E ratios like ITC’s to be considered reasonable.

Taking a look back first, the company’s earnings per share growth last year wasn’t something to get excited about as it posted a disappointing decline of 2.6%. This has soured the latest three-year period, which nevertheless managed to deliver a decent 20% overall rise in EPS. So we can start by confirming that the company has generally done a good job of growing earnings over that time, even though it had some hiccups along the way.

Turning to the outlook, the next three years should generate growth of 10% per year as estimated by the analysts watching the company. With the market predicted to deliver 19% growth per year, the company is positioned for a weaker earnings result.

In light of this, it’s curious that ITC’s P/E sits in line with the majority of other companies. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Key Takeaway

It’s argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We’ve established that ITC currently trades on a higher than expected P/E since its forecast growth is lower than the wider market. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the moderate P/E lower. Unless these conditions improve, it’s challenging to accept these prices as being reasonable.

You always need to take note of risks, for example – ITC has 1 warning sign we think you should be aware of.

If these risks are making you reconsider your opinion on ITC, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

{kind=link}