A QIP essentially gives listed companies a fast and relatively simple route to raise equity capital. Instead of approaching a broader set of shareholders, firms raise funds directly from institutional investors, including mutual funds, insurance companies, pension funds, foreign institutions, and banks.

The mechanism is straightforward. Companies get fresh capital without navigating a long regulatory process. And they often do it when the market mood is upbeat and their stock commands a premium. Yet, this is where the pattern turns familiar. Managements usually tap institutional money when their stock price is soaring and confidence is at its peak. But the period that follows often tells a different story.

Many companies turn to a QIP when their stock is already trading at stretched valuations. Once the funds are raised, the picture often shifts. Earnings lose pace, growth slows, and the share price begins to correct. Investors who entered during that phase of optimism (including institutions) often find themselves stuck at elevated levels. More often, they mark the point where the best part of the story is already priced in.

Mint looks at four examples where companies raised money through QIPs, only for their results to weaken and their share prices to follow the same path afterwards.

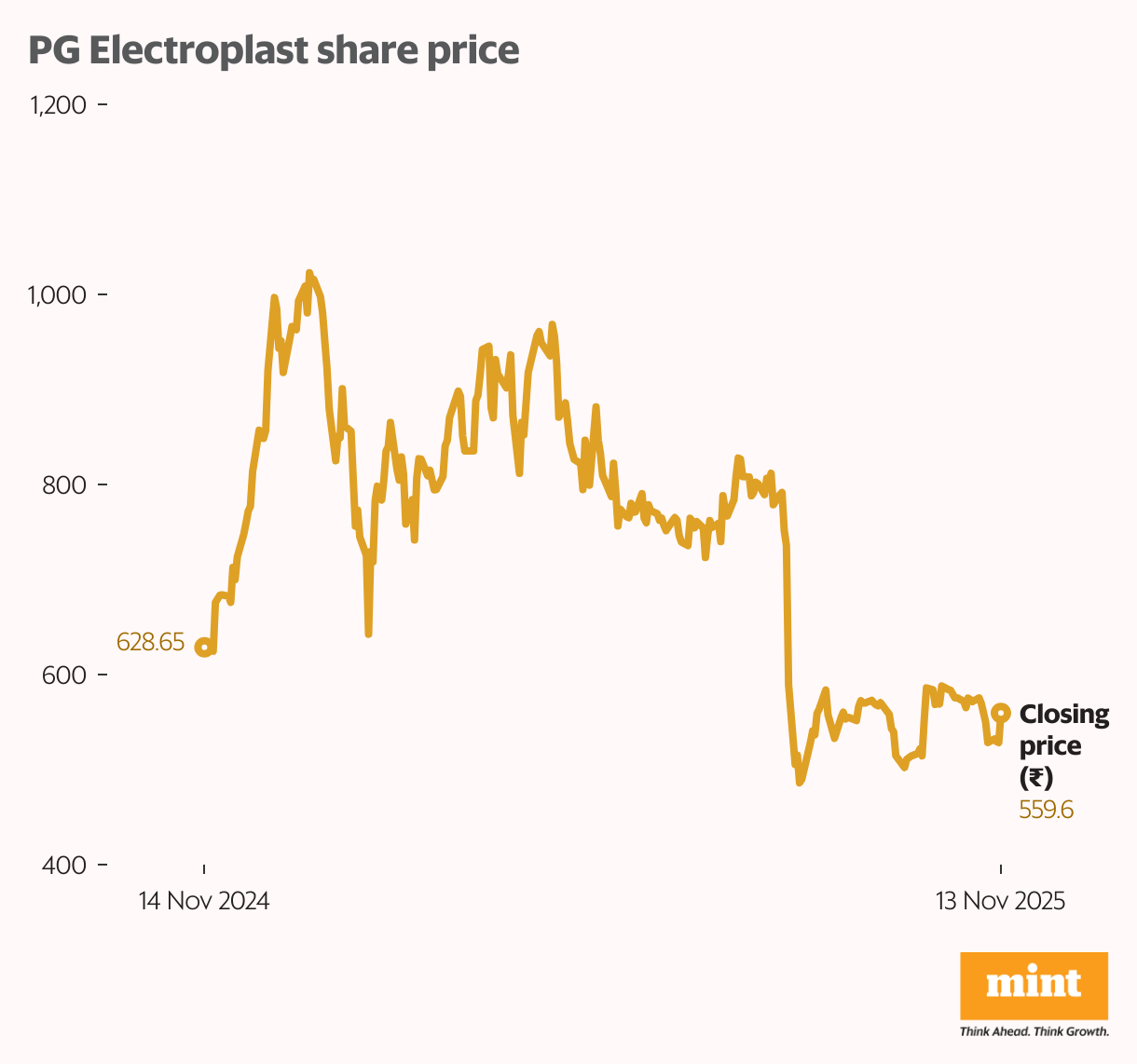

PG Electroplast: Down 20% from QIP price

PG Electroplast Ltd has emerged as a meaningful player in India’s Electronic Manufacturing Services (EMS) ecosystem, a sector that continues to benefit from structural support such as the China+1 shift and the government’s Make in India focus.

Product manufacturing (includes room ACs, washing machines, and air coolers) accounted for 71% of its FY25 revenue. The balance came from plastic moulding (20%), electronics (7%), and moulds (2%).

Riding a period of strong investor sentiment and premium valuations, PG raised ₹1,500 crore through a QIP in December at ₹699 per share, when the stock traded at more than 110 times price-to-earnings (P/E) multiple. The fundraise was for expansion, including investments in subsidiaries, debt reduction, and the company’s planned foray into EV manufacturing.

In Q4 FY25, the strategy seemed well supported by the numbers: revenue doubled to ₹1,910 crore from ₹1,077 crore a year earlier, and profit after tax (PAT) showed a similar jump to ₹145 crore from ₹70 crore. However, the momentum didn’t sustain.

In the first quarter of FY26, revenue growth decelerated sharply to 13.8%, and profit after tax (PAT) fell 20.2% to ₹67 crore—a turnaround that surprised the market. The market punished the stock severely. PG Electroplast fell 38% in a matter of days, from ₹790 on 5 August 2025, to ₹490 by 14 August. It is currently trading at ₹560, down 47% from the January all-time high of ₹1,054.

The weakness in performance stemmed largely from lower-than-expected AC volumes and the impact of negative operating leverage. The shorter summer due to the early arrival of the monsoon left the company with elevated inventory and pressure on margins. As a result, PG Electroplast revised its FY26 guidance downward.

The management’s internal target is to reach ₹9,000 crore in revenue by FY28, based on a plan to increase the gross block from ₹1,200 crore to ₹2,200 crore over the next two years. The assumption rests on maintaining asset turnover in the 4.5-5 times range at full utilization. This estimate now depends heavily on how quickly utilization normalizes and whether the AC cycle turns more favourable in the coming quarters.

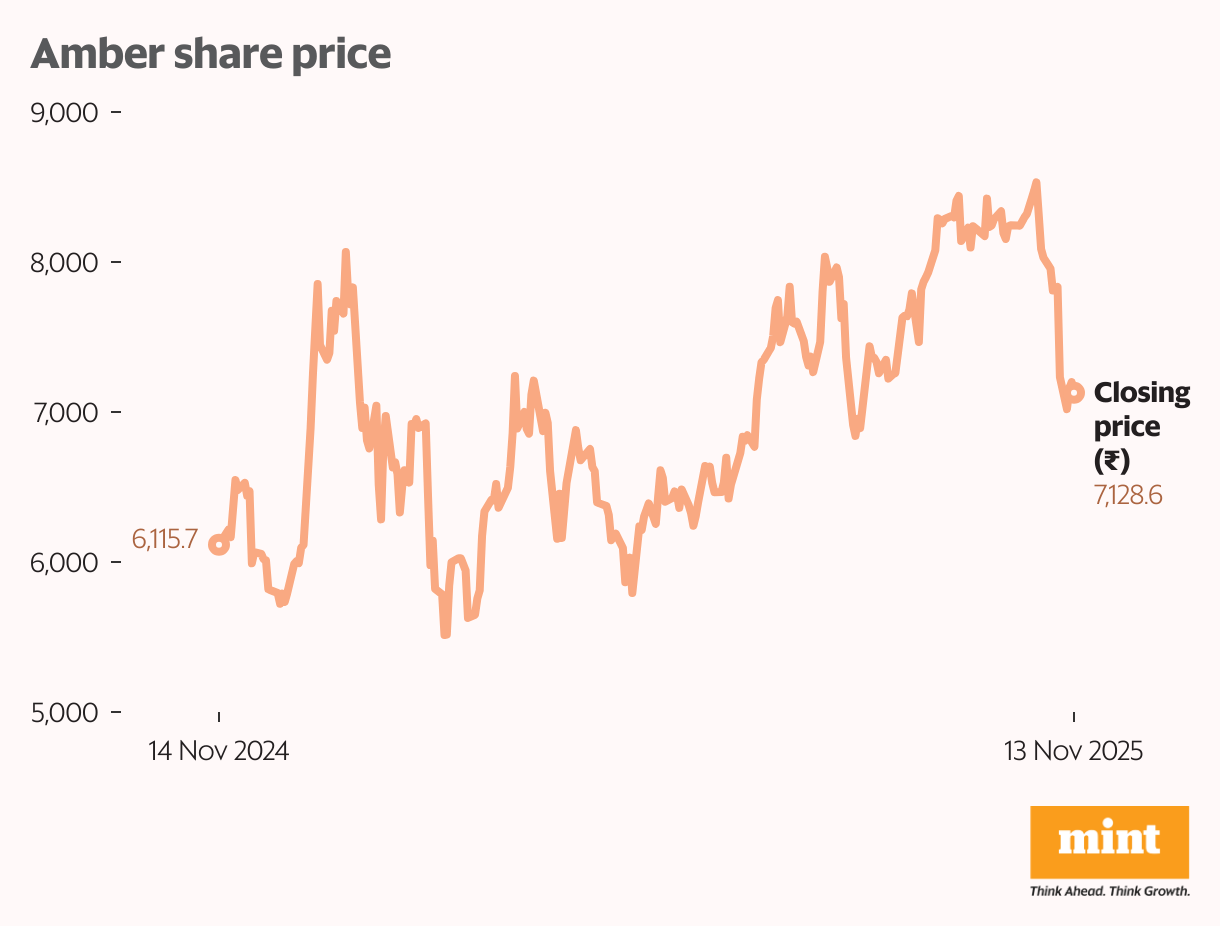

Amber Enterprises: Down 10% from QIP price

Amber Enterprises India Ltd is a backwards-integrated and diversified B2B solutions provider operating across consumer durables, electronics (including EMS), railway subsystems and defence. Its strong presence in room AC manufacturing allows it to cater to nearly 70% of the AC bill of materials, making it a preferred partner for leading brands.

The company holds an estimated 27% market share in room AC manufacturing in value terms, and has steadily expanded into producing fully automatic top-loading and front-loading washing machines, along with key components.

In September 2025, Amber raised ₹1,000 crore through a QIP at ₹7,950 per share, a level that reflected a P/E of more than 110 times. Most of the proceeds, around ₹900 crore, were directed toward repaying existing borrowings, with the remainder earmarked for general corporate purposes. The stock climbed further to ₹8,626 by late October, helped by positive sentiment around the fundraise.

The tone shifted soon after. Amber reported a loss of ₹32 crore in Q2FY26, accompanied by a 2.2% decline in revenue to ₹1,647 crore. Higher finance costs and elevated inventory levels in the room AC business largely drove the loss. The market reacted sharply, with the stock closing 7.7% lower on 7 November at ₹7,227 after the results.

The stock is now down about 10% from its QIP price ( ₹7,950) to ₹7,122, and nearly 17% below its October peak of ₹8,626. Management expects the excess inventory, a key reason behind the Q2 loss, to normalize by Q4 FY26, which will be crucial for retaining profitability.

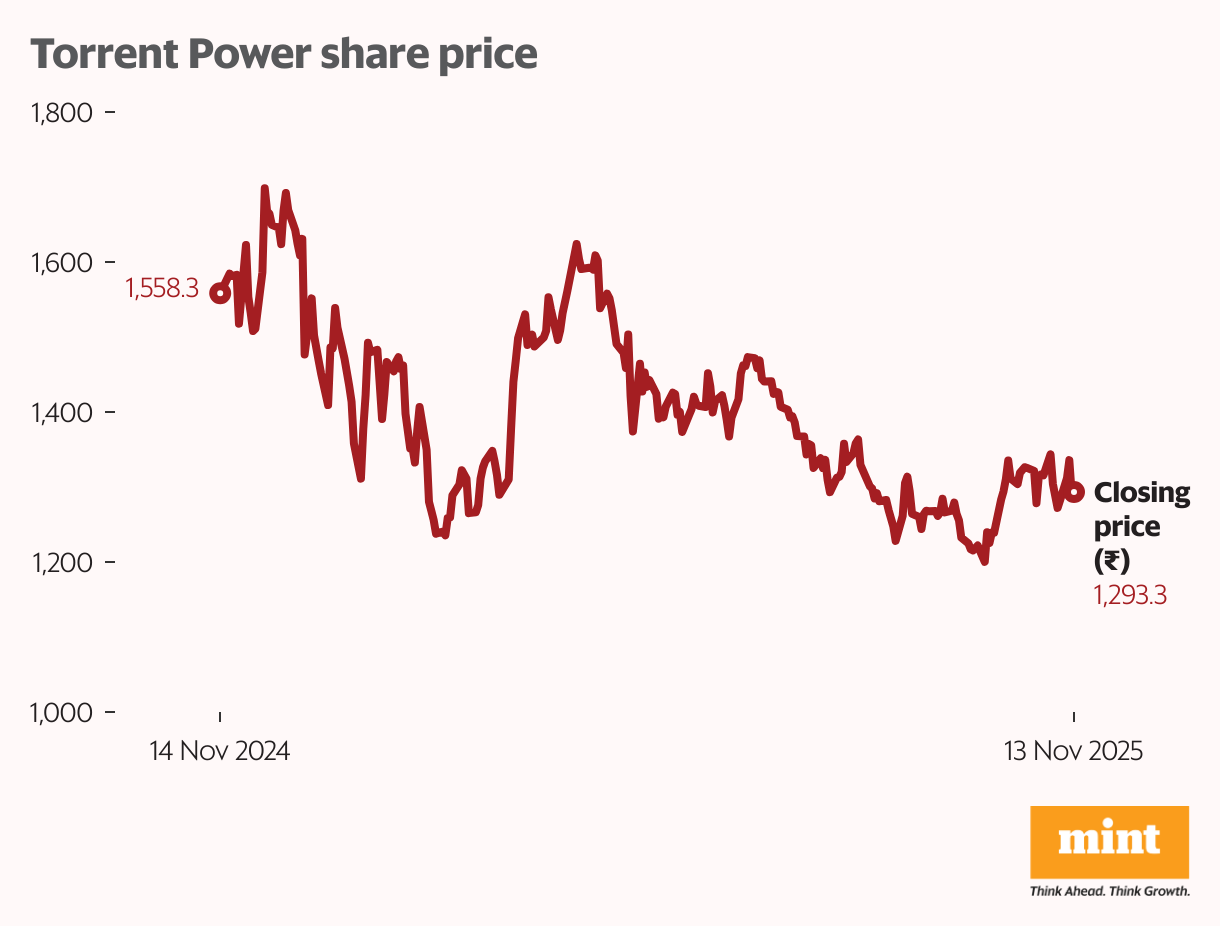

Torrent Power: Down 14% from QIP price

Torrent Power Ltd is an integrated power utility company with a strong presence across the entire energy value chain, from generation, transmission, to distribution. The company has a total generation capacity of 7,992 megawatt (MW), comprising 2,730MW thermal energy and 4,900MW renewable energy.

The company serves over 4.2 million customers across three states and one Union territory. Torrent is exploring new avenues such as achieving 10 gigawatt (GW) of renewable capacity by 2030, developing large pumped storage hydro projects (with a cumulative potential capacity of about 8.4GW), and also planning to expand into green hydrogen and green ammonia.

Torrent Power raised ₹3,500 crore through a QIP in December 2024 at ₹1,503 per share, marking the Torrent Group’s first equity issuance in more than three decades. Most of the funds went toward debt repayment ( ₹2,625 crore), while the remaining ₹822 crore was allocated to general corporate purposes. At the time of the fundraiser, the stock was trading close to its peak valuation of about 35 times earnings, reflecting the strong optimism surrounding the business.

But the quarters that followed didn’t fully justify that elevated pricing.

In Q4 FY25, revenue remained flat at ₹6,456 crore compared with ₹6,529 crore a year earlier. Profit before tax also showed no movement, staying at ₹619 crore (versus ₹617 crore). We have not considered PAT due to a one-off tax adjustment during the period.

The slowdown became more visible in Q1FY26, when revenue declined 12.5% year-on-year to ₹7,906 crore, and PAT dropped 25.5% to ₹742 crore. The market reacted accordingly. Since the QIP, the stock has corrected about 14% to ₹1,294, and it is down nearly 25% from its 52-week high of ₹1,720 per share. Although Torrent’s PAT grew 49.6% to ₹742 crore in Q2 FY26, the damage to sentiment had already been done.

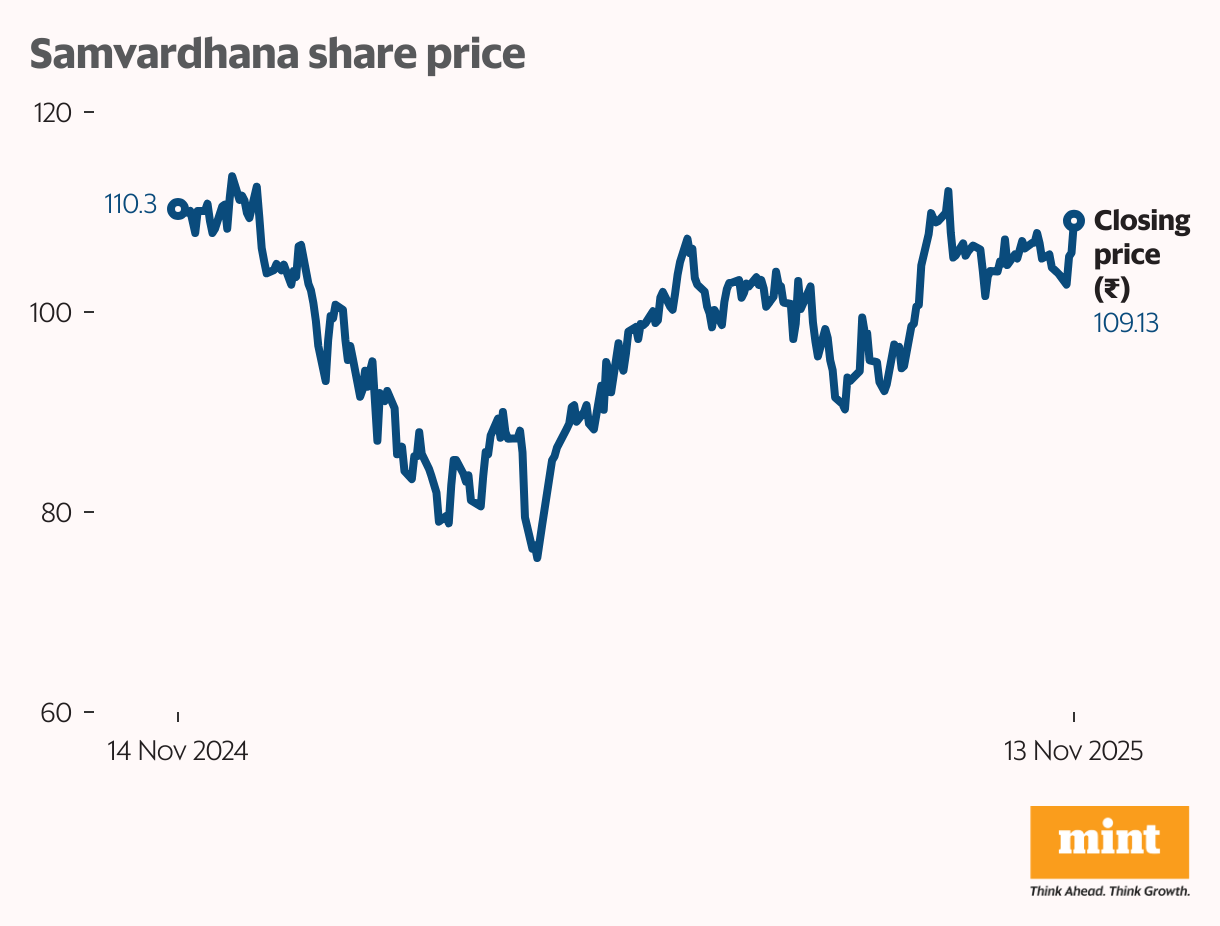

Samvardhana Motherson International: Down 18% from QIP price

Samvardhana Motherson International Ltd is India’s largest auto ancillary company and ranks among the top 15 global automotive suppliers. Its footprint spans multiple geographies and industries, giving it one of the most diversified portfolios in the auto component space.

In the second half of September 2024, the company raised ₹6,438 crore at ₹133 per share (adjusted for the 1:2 bonus issue in July 2025). The fundraising was structured as a composite offering of equity shares and compulsorily convertible debentures, with the proceeds used mainly for debt repayment and general corporate purposes.

At the time of the issue, the stock was trading at nearly 45 times earnings, reflecting the strong sentiment around the business. But the momentum didn’t hold. From the March 2025 quarter onward, the company’s numbers began to soften. Profitability declined 22.8% in Q4FY25, then 44.7%, and 10.8% over the next two quarters up to the September 2025 quarter.

The steady drop in earnings weighed on the stock, which now trades at around ₹109 per share—almost 18% below the QIP price.

Looking ahead, Samvardhana Motherson has outlined its Vision 2030 plan, which marks the beginning of its seventh five-year strategy cycle. The company aims to increase content per vehicle, deepen its presence in emerging markets, and expand into new industries. The roadmap leans on three pillars—organic expansion, acquisitions, and strategic partnerships—with the goal of achieving multi-fold growth over the coming decade.

Valuations matter more than fundraising.

The recent QIP cycle shows a clear pattern: when companies raise money at stretched valuations, even a slight slip in performance can trigger sharp corrections. PG Electroplast, Amber Enterprises, Torrent Power, and Samvardhana Motherson all tapped the market when optimism was high, but their subsequent results didn’t fully support those elevated prices.

These are just a few examples. Sona BLW is also down 30% from its QIP price of ₹690 to the current price of ₹489. Swiggy is now planning to raise another ₹10,000 crore through a QIP, just after mobilising ₹4,500 crore via its IPO a year back. The move comes at a time when the quick-commerce battle is heating up again, and competitors are burning cash to chase growth.

For investors, the takeaway is simple. A QIP may strengthen a balance sheet or fund expansion, but the valuation at which it is priced leaves little room for error. When expectations run ahead of fundamentals, the downside tends to arrive faster than the growth that was promised.

For more such analysis, read Profit Pulse.

Madhvendra has over seven years of experience in equity markets and writes detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

{kind=link}