The September quarter (Q2FY26) results of both companies had their share of misses. Even so, Jindal Steel SL is doing better on select parameters.

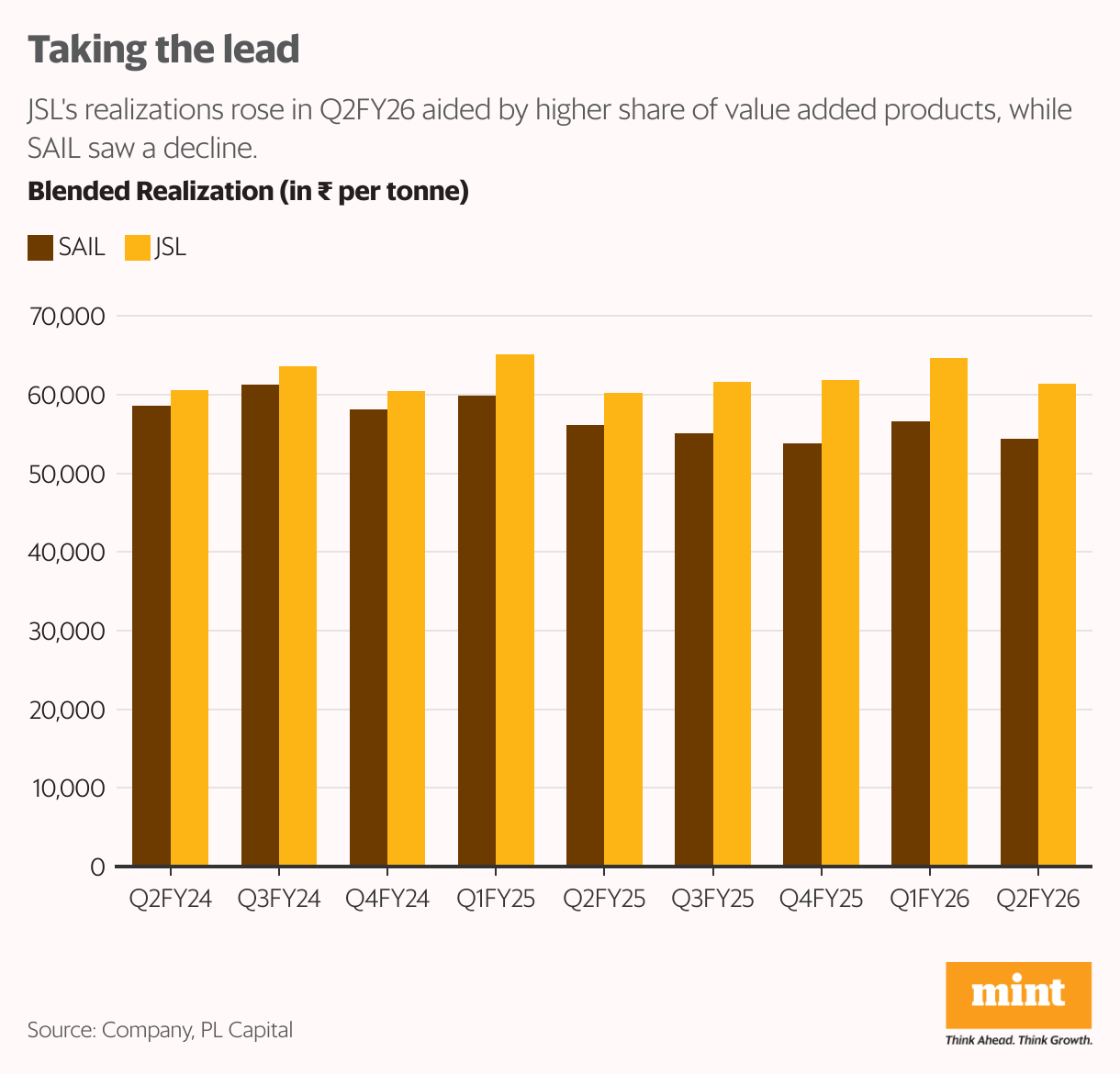

Take for instance their realizations. SAIL’s standalone revenue rose 8% year-on-year to ₹26,700 crore in Q2FY26, backed by a strong 20% volume jump. However, blended realization fell by 10%, impacted by softer steel prices, with heavy monsoon affecting demand.

On the other hand, JSL’s consolidated revenue increased 4% year-on-year in Q2FY26 to ₹11,686 crore, aided by about 3% increase in realization.

JSL managed to improve its realization despite a subdued market, thanks to a higher proportion of value-added grades, which rose to 73% during the quarter, up from 58% last year. On a per tonne basis, JSL’s realization at ₹61,400 was about 15% higher than SAIL’s ₹54,400 per tonne.

Further, despite an improved topline, SAIL’s Ebitda declined 13% to ₹2,530 crore, weighed down by higher raw material cost, which rose 15% with higher coking coal prices, and higher other expenses.

While JSL’s raw material cost rose only marginally by 3%, with savings arising due to production of captive iron ore, its profitability was impacted by one-off costs related to plant shutdown.

As a result, its Ebitda, adjusted for foreign exchange fluctuations, fell by 12%, to ₹1,900 crore. Raw material-to-sales ratio for JSL stood at 45%, against 50% for SAIL, giving it a notable competitive advantage.

A higher cost structure along with lower realization meant Ebitda per tonne of ₹5,493 for SAIL during the quarter (excluding volumes sold on behalf of NMDC Steel at fixed margin basis), close to half that of JSL at ₹10,027 per tonne.

In Q2FY26, JSL’s volume grew a modest 1% year-on-year in Q2FY26 owing to a maintenance shutdown. The management has guided for sales of 8.5-9 million tonnes (mt) in FY26, against 8 million tonne in FY25, aided by the newly commissioned facilities.

In comparison to JSL, the industry volume grew 9%, said HDFC Securities Ltd and JSL’s guidance which implies 15-30% growth in H2FY26.

Note that JSL is undertaking significant capital expenditure (capex) and commissioned a blast furnace and a basic oxygen furnace at Angul during the quarter. It would be commissioning some additional facilities in H2FY26 also.

Despite all the capex, JSL has maintained a healthy balance sheet with net debt-to-Ebitda of 1.48x at the end of Q2FY26, almost the same as 1.49x in Q1FY26. This is the lowest among all steel majors.

SAIL’s first expansion project, increasing its capacity by 2-3 million tonne per annum (mtpa), is expected to come online by FY28 only.

It is still at the equipment tendering stage for its expansion plan to 35 mtpa from 20 mtpa now, projected by FY31.

“SAIL’s earning profile is now a function of cost and realisations, as volume growth will likely remain muted for the next few years due to capacity constraints,” said ICICI Securities.

Meanwhile, JSL is trading at an enterprise value of 10x its FY26 estimated Ebitda, as per Bloomberg, higher than 7.4x for SAIL, with investors factoring in potential gains from the capacity expansion.

Steel and coking coal price trend, along with demand pick up in a seasonally strong second half, would determine the stock price movement, going forward.

{kind=link}