Amara Raja Energy & Mobility Ltd is juggling persistent margin pressure in its core lead-acid battery business while spending heavily to build capacity in lithium-ion technology, its new-energy business.

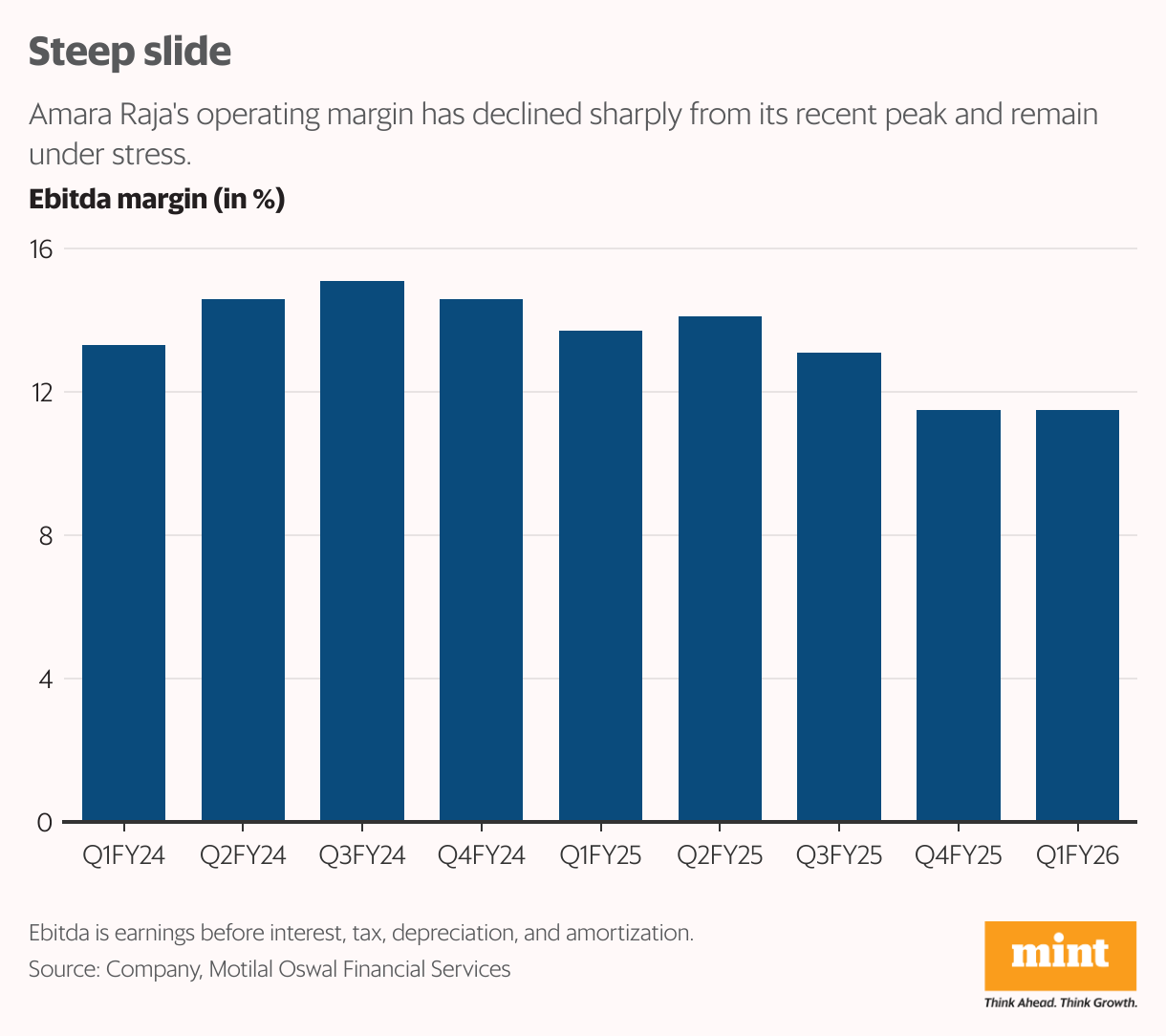

Elevated alloy and power costs, along with a higher share of lower-margin traded products, dragged operating margin down by 220 basis points year-on-year to 11.5% in the June quarter (Q1FY26). Management expects a gradual margin recovery to 13% by Q3FY26, aided by easing power costs, reinstatement of the tubular plant, and the start of operations at the new recycling facility, which should lower input costs.

The lead-acid segment, which contributes 96% of revenue, is showing mixed demand trends. Two-wheeler replacement volumes rose 5-6% in Q1FY26, while four-wheeler OEM demand grew 12-13%. The management expects replacement growth to sustain at 10-11% annually for two-wheelers and 6-7% for four-wheelers. Industrial UPS is guided to grow 5-6%. However, exports were weak, with shipments down 7-8% due to tariff-related headwinds, and are likely to recover only in H2FY26 as supply chain issues ease and new markets open.

Several brokerages trimmed their earnings estimates for FY26-FY27 following the muted performance in Q1FY26. But the stock’s steep 19% decline in calendar year 2025 so far, compared with Exide Industries Ltd’s 6% drop, reflects concerns beyond margin pressure. Diversifying into lithium-ion fits broader industry trends, but scaling-up prospects and visibility on return ratios in this low-margin business remain murky.

Amara Raja has invested ₹1,200 crore in its electric vehicle (EV) arm and needs a similar sum for research labs, a customer qualification plant, and working capital. Capital expenditure is pegged at ₹1,200-1,300 crore for FY26, of which ₹800-900 crore will go into the lithium cell and pack business. The first gigafactory line — 1GWh of NMC (Nickel Manganese Cobalt) cylindrical cells — is due by FY27, with a longer-term ambition of 16GWh by FY30.

For now, however, the company has scaled back the first phase from 2GWh to 1GWh, while keeping the option open to migrate to LFP (Lithium Iron Phosphate) batteries depending on demand. OEMs are increasingly tilting toward LFPs, attracted by their relatively lower costs.

Investors are thus caught between a margin-challenged lead-acid business and an expensive, uncertain lithium pivot, making the stock’s 17x FY27 PE multiple look unattractive.

On the revenue front, Amara Raja’s lead acid business is growing faster than Exide’s. Double-digit replacement growth provides insulation against the cyclicality of OEM and industrial segments, said Elara Securities (India).

However, further order wins in lithium-ion cell manufacturing, especially for PV OEM, will drive near-term valuation, even as the profitability of lithium-ion cell will remain a concern initially, it added.

{kind=link}