Bata India Ltd’s shares have vastly underperformed the broader market, sliding 22.5% so far in 2025 against a nearly 2% gain in the Nifty 500 index. Yet, beaten-down earnings prospects offer little comfort on valuations—the stock still trades at 53 times estimated FY26 earnings, according to Bloomberg data.

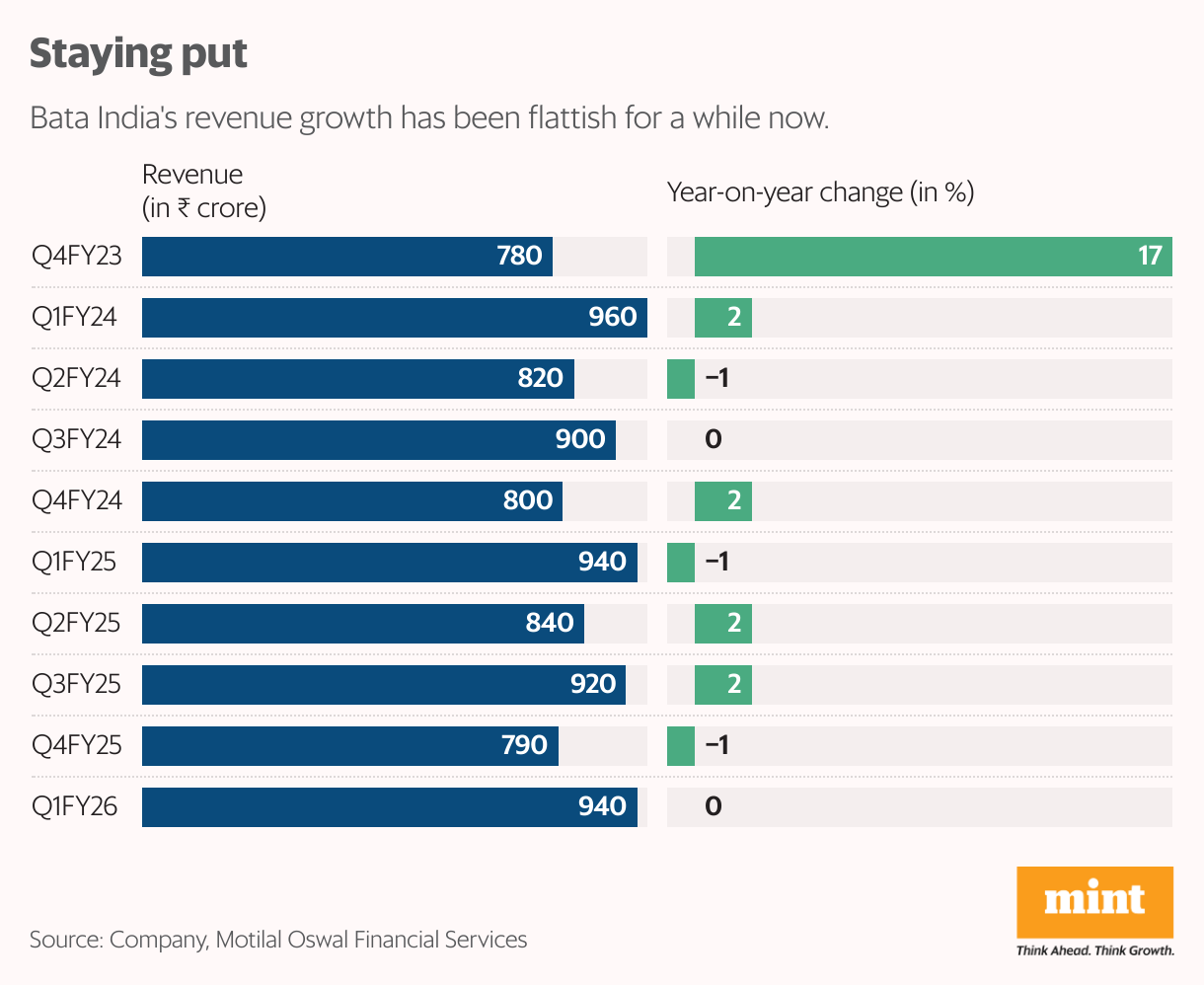

The problem isn’t new. Bata has long struggled to lift sales growth amid intensifying competition and tepid consumer demand. The recently concluded June quarter (Q1FY26) was no exception, with revenue slipping marginally year-on-year to ₹942 crore. That marked the ninth straight quarter of flattish annual growth.

Unsurprisingly, analysts have pared back expectations.

Motilal Oswal Financial Services has cut its FY26-27 revenue and Ebitda forecasts by 3-6% citing the persistent weakness in growth. “Strategic initiatives such as inventory cleanup, curated product refreshes, and franchise-led expansion should enhance efficiency and aid margin recovery, though near-term competitive pressures remain,” the brokerage said in its Q1 review report.

Bata itself points to pressure at the lower price points—products below ₹1,000—as a key drag. Last quarter’s challenges were accentuated by fluctuating weather patterns and geopolitical uncertainties. The company has rolled out its zero-base merchandising project aimed at improving efficiency and enhancing customer experience to 194 stores as of June-end.

Premium brands like Hush Puppies and Floatz were resilient. Floatz grew by 33% on the back of a 29% increase in volumes. Hush Puppies continues to expand, supported by significant investments in refreshed store formats. The premium footwear line now has about 150 exclusive brand outlets and recently launched an office sneakers collection.

Bata’s Q1 gross margin dipped 140 basis points (bps) to 53.5% due to clearance of some older inventory. However, a decline in staff costs and other expenses meant Ebitda margin rose 153 bps to 21.1%. Thus, Ebitda increased 7.5% year-on-year, faring better than revenue growth.

Still, that’s not exciting enough. The stock needs sustained volume and revenue growth to re-rate, but that may not materialize soon.

“Near-term challenges persist, with weak demand mainly due to a significant portion of the mass portfolio still under pressure,” said Axis Securities. Given this, the broking firm has cautious stance and maintains its ‘Hold’ rating on the stock.

{kind=link}