{kind=link}

The issue, priced between ₹557 and ₹585 a share, is a complete offer-for-sale by promoters divesting 7.78 million shares. At the upper end, Studds’ market capitalization is pegged at ₹2,302 crore. There’s no fresh capital coming in, which may limit immediate expansion benefits, but it sets up a clear test of investor appetite for a company built at the intersection of India’s mobility and consumer stories.

The listing will also gauge whether Studds can move beyond its niche as a two-wheeler accessory maker to become a lifestyle brand. While the company dominates India’s organized helmet market with a 25.5% value share and 27.3% volume share (2024), its growth has lagged the broader mobility boom. Revenue expansion has been modest, even as profitability surged largely on lower input costs—gains that may prove hard to sustain in a cyclical, price-sensitive segment.

A two-brand play on safety and style

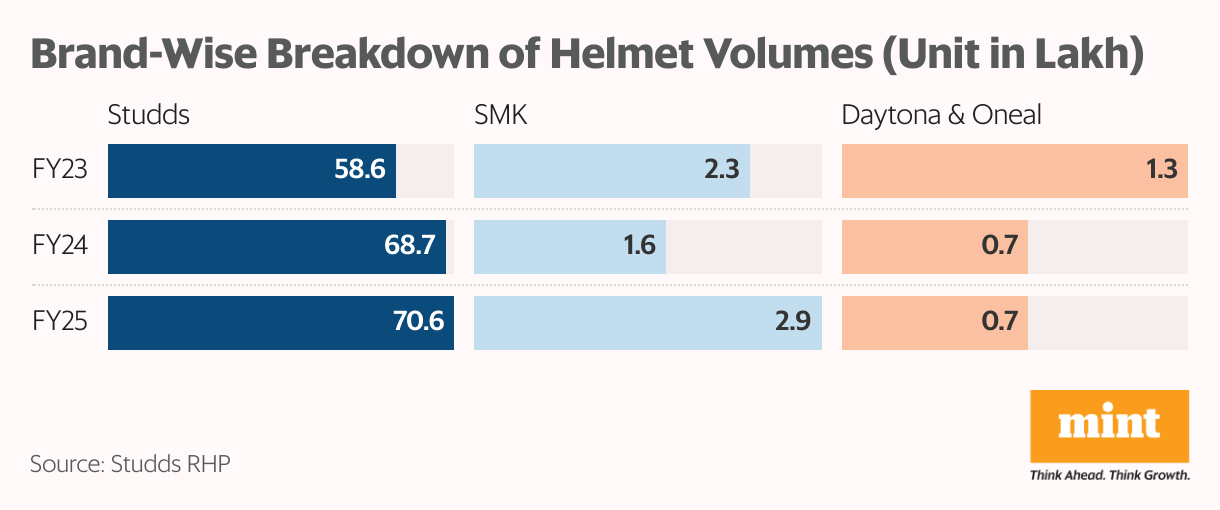

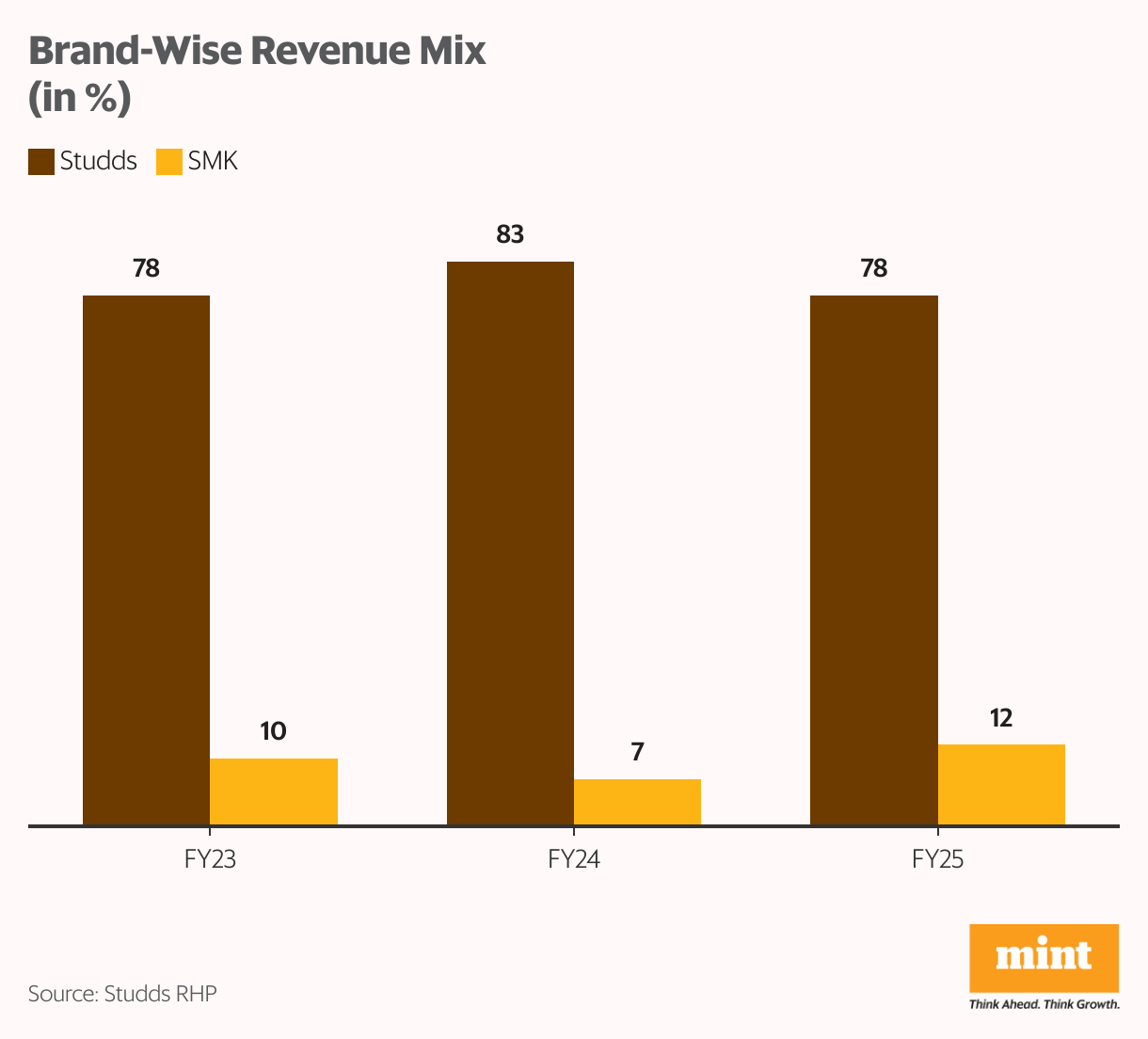

Studds designs, manufactures, and sells helmets under two brands – Studds and SMK. The flagship Studds brand targets mass and mid-market commuters, offering more than 160 models priced between ₹875 and ₹4,000. The premium SMK line caters to aspirational riders in India and mid-market customers in Europe, with helmets priced up to ₹12,800. Together, they contribute roughly 90% of total revenue, with Studds accounting for 78% and SMK for 12%, up from 10% in FY23.

Studds also produces white-label helmets for international brands such as “Daytona” (US) and “Oneal” (Europe), though these volumes have been declining amid changing European safety regulations. Such regulatory shifts, both at home and abroad, remain a key overhang for growth.

Riding the two-wheeler wave—with limits

Helmets make up 92.4% of Studds’ revenue, underscoring its deep linkage to two-wheeler sales cycles. Accessories such as luggage boxes, gloves, and rain suits account for just over 7%, a concentration that leaves the company exposed to industry slowdowns. Some recent product launches, including the Stellar-Wings and Sportster models, have struggled to find traction, highlighting execution and design risks.

That said, its dual-brand strategy gives it a presence across price tiers, from mass commuters to premium enthusiasts. Management plans to expand the SMK portfolio and enter adjacent categories such as bicycle helmets, riding apparel, and high-margin accessories.

Inside the factory floor

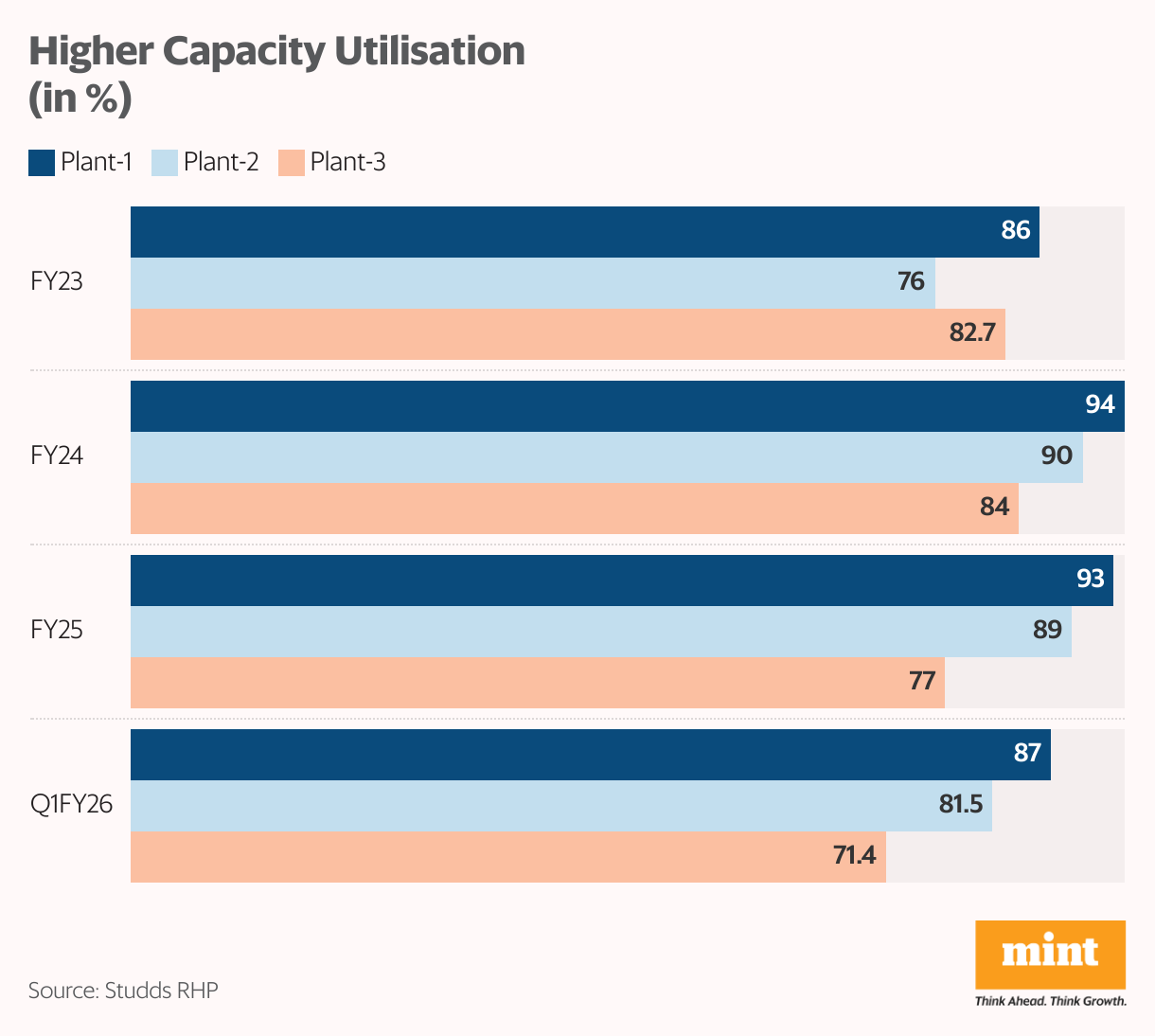

Studds operates four manufacturing facilities in Faridabad, Haryana, with a fifth under construction. The company is vertically integrated—handling everything from raw material procurement and moulding to painting and assembly—which supports quick turnaround and better quality control.

Its plants are running at high utilization, signalling strong demand, though the tight geographic clustering poses a concentration risk. Any disruption or underutilization in this hub could materially affect operations. Studds sources nearly 89% of its raw materials domestically, limiting global exposure, but depends on its top supplier for about 21% of inputs.

Distribution and market reach

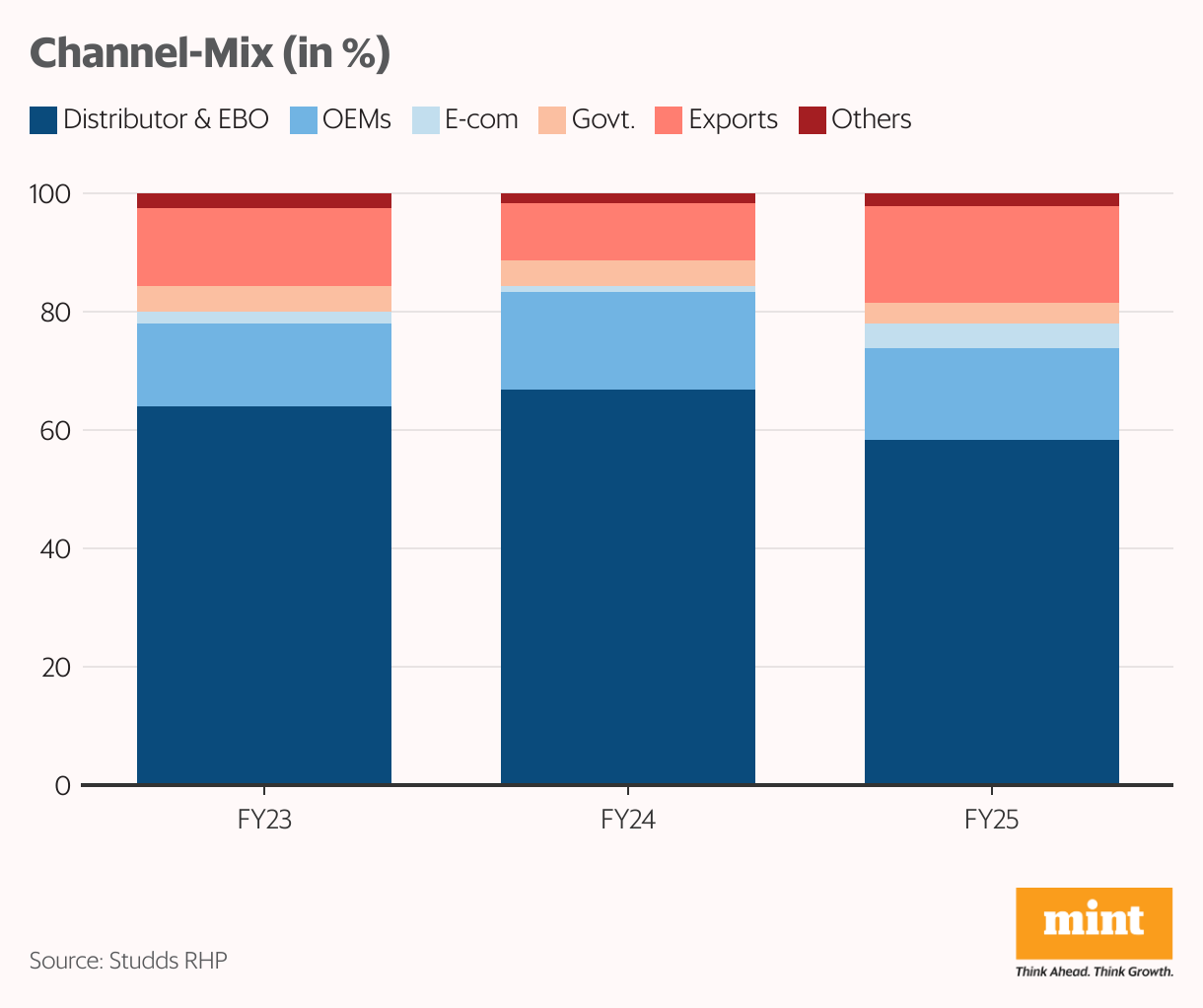

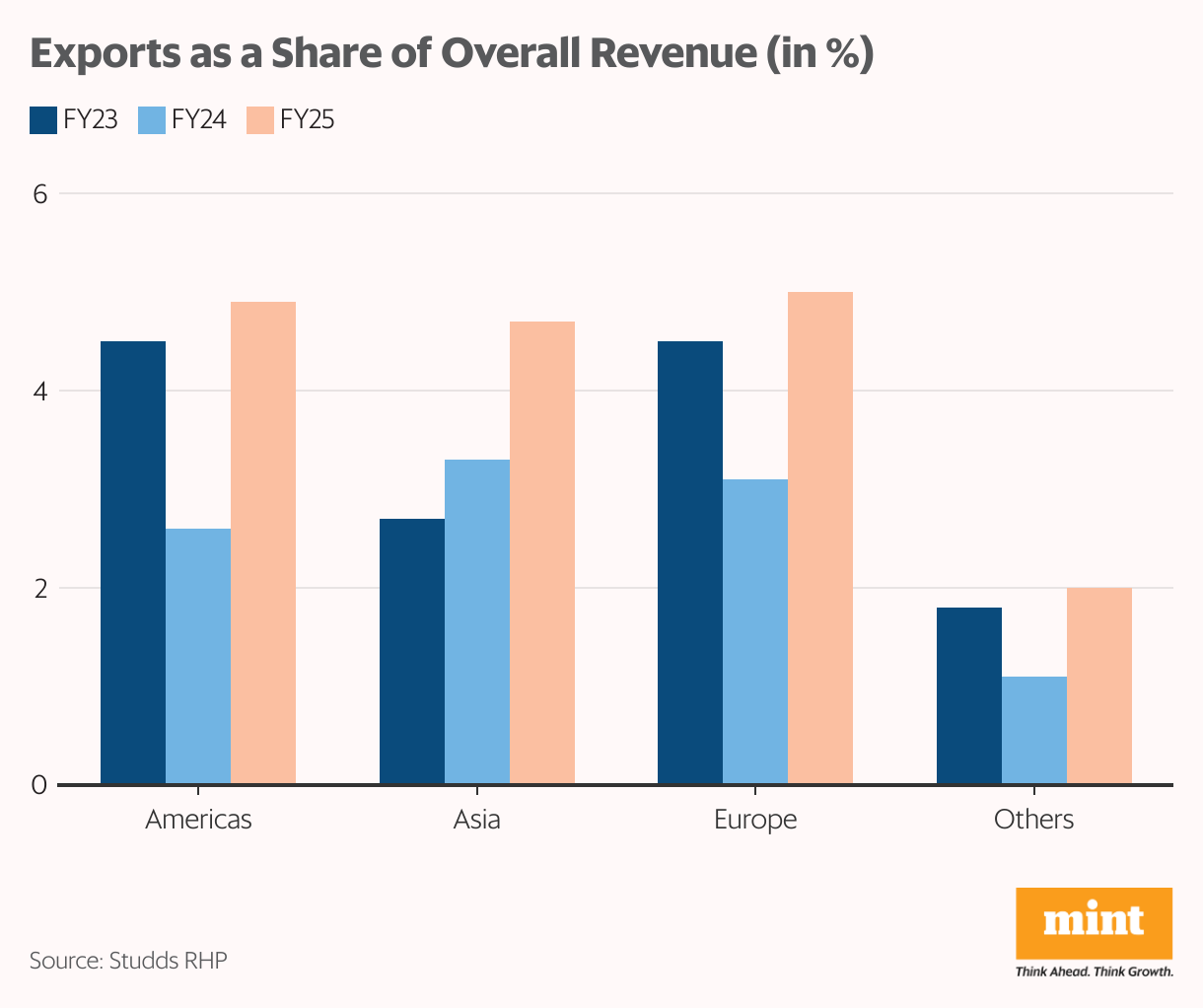

The company sells through 363 active distributors across India, supplying to major original equipment manufacturers such as Hero MotoCorp, Suzuki Motorcycle, Eicher Motors, and Yamaha. Distributors and exclusive brand outlets account for 58.4% of revenue, followed by OEMs (15.5%), e-commerce (4.2%), government channels (3.5%), and exports (16.2%).

While this diversified mix gives Studds reach, the absence of long-term distributor agreements could make its network vulnerable to competitive pressures. Rivals offering better terms could lure away dealers, hurting sales stability.

Financials and efficiency gains

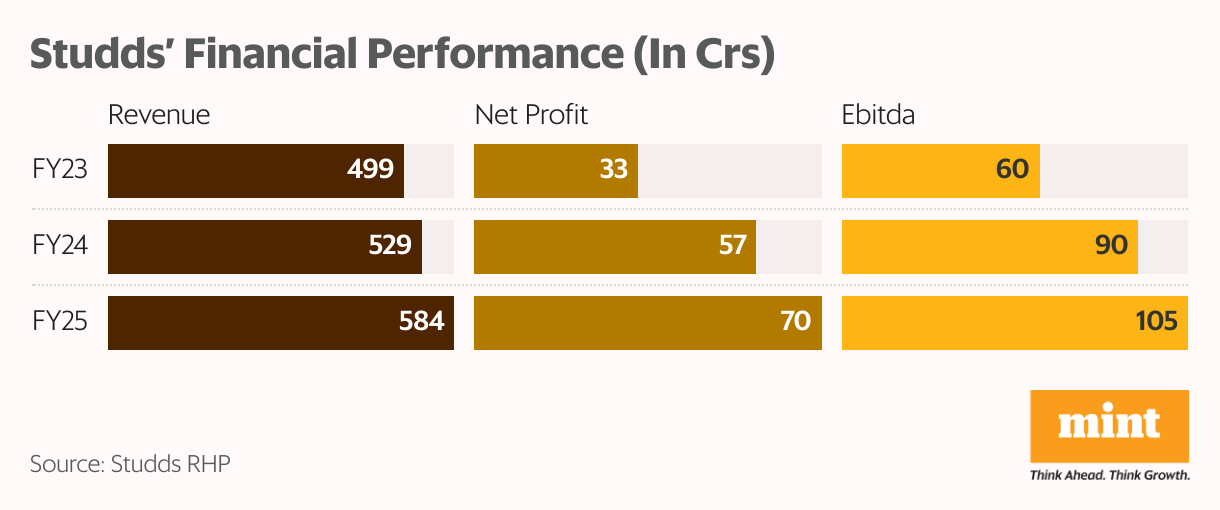

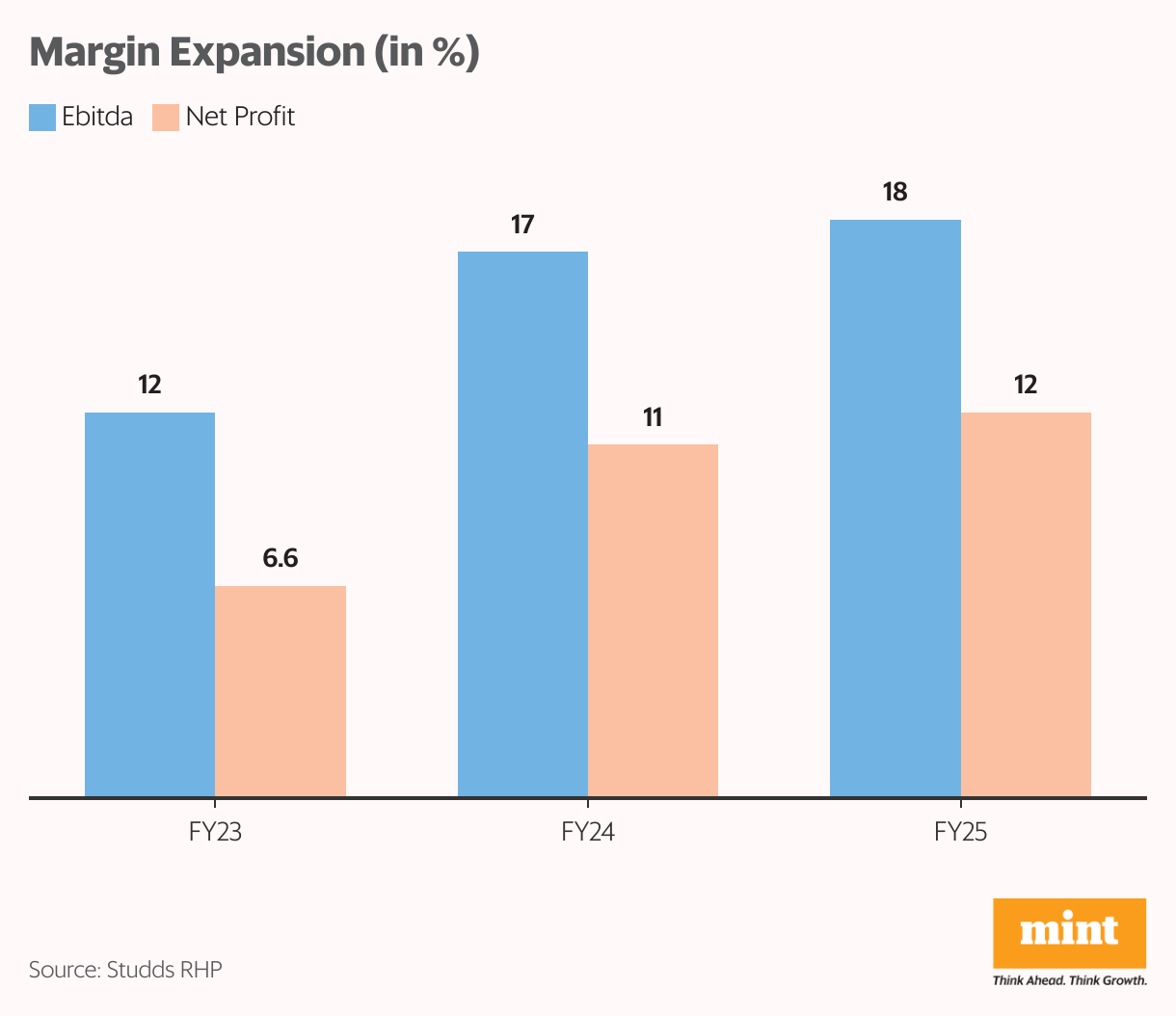

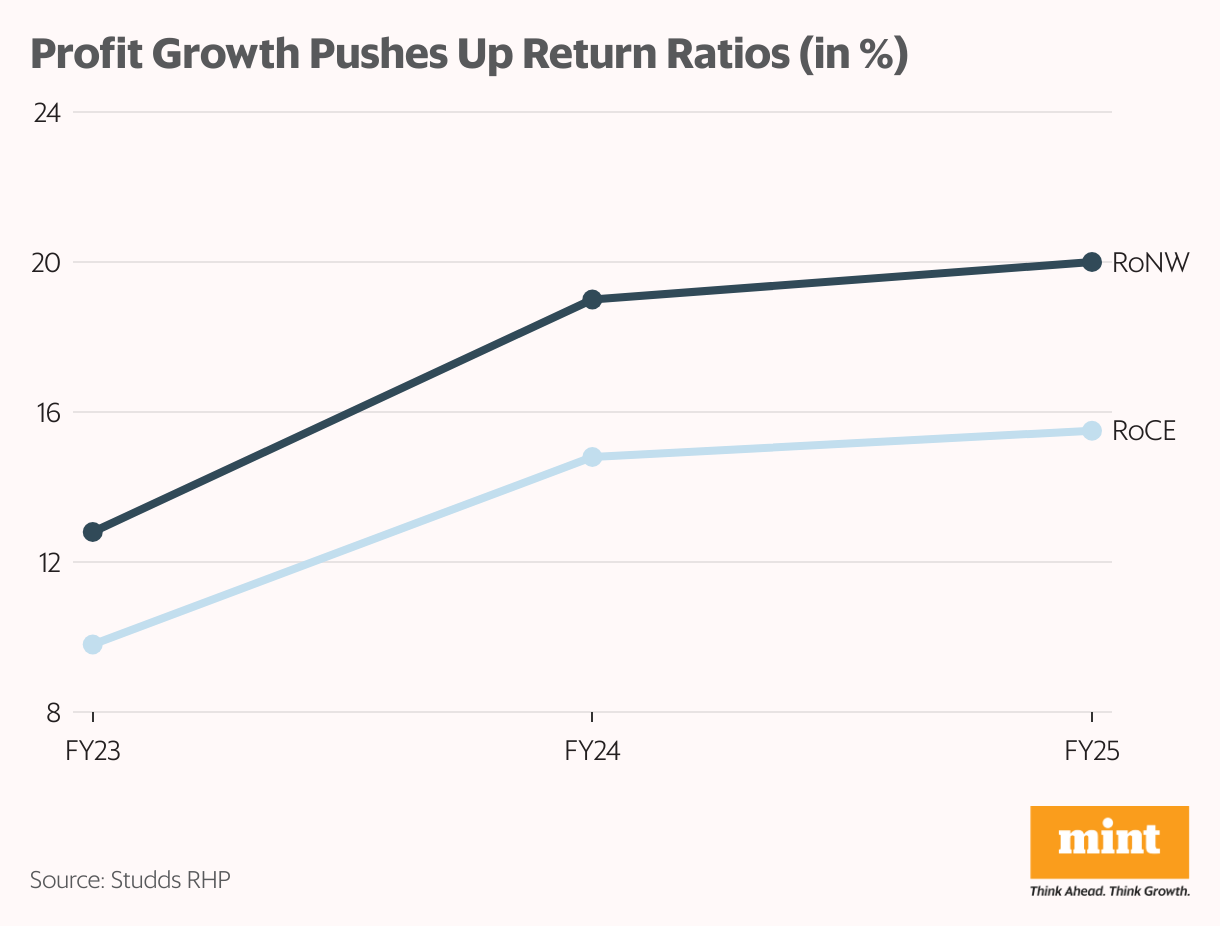

Revenue grew from ₹499 crore in FY23 to ₹584 crore in FY25, a compound annual growth rate (CAGR) of 8.5%. However, Ebitda rose much faster, 32% CAGR over the same period, lifting margins by nearly 600 basis points to 18%. Net profit nearly doubled to ₹70 crore, translating to a 12% margin.

The improvement largely reflects lower plastic and raw material prices. Net debt is nil, supported by disciplined working-capital management and weekly distributor payments. As of June 2025, cash and equivalents stood at ₹55 crore, up from ₹25 crore in FY23.

The question now is whether these margins are sustainable if input costs rise or if growth fails to accelerate.

Is the valuation justified?

At its FY25 earnings of ₹69.6 crore, Studds’ IPO is priced at roughly 33 times earnings—reasonable by auto-ancillary standards but elevated for a business with modest top-line growth. The company has no direct listed peers, either in India or globally, giving it a scarcity premium.

The last private share issue at ₹450 (adjusted for bonus, August 2024) suggests the IPO isn’t excessively priced. Still, investors must weigh whether current profitability reflects structural strength or a temporary commodity tailwind.

The road ahead

The long-term story remains intact. India’s helmet ownership per two-wheeler stands at just 0.6x versus a global average of 1.5x. With stricter enforcement of BIS safety standards and rising consumer preference for premium designs, the organized sector’s share is projected to rise to 80% by 2029 from about 70% in 2019.

For more such stock analysis, read Profit Pulse.

For Studds, which spans both value and premium segments, these tailwinds could sustain demand even as competition intensifies. But in the short term, valuation comfort will hinge on whether the company can translate efficiency-led profitability into consistent revenue growth.

For investors, this is less a momentum trade and more a test of Studds’ ability to evolve from a cyclical two-wheeler supplier into a consumer brand with staying power.

Madhvendra has over seven years of experience in equity markets and writes detailed research articles on listed Indian companies, sectoral trends and macroeconomic developments.

The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.