Analysts say the response to LG’s offer will reveal whether investor appetite for steady, domestically focused businesses remains intact after Urban Company’s blockbuster debut revived confidence in India’s consumption story.

Dhruv Jain, consumer electronics analyst at Ambit Capital, expects healthy demand for LG’s IPO, noting that its valuation has moderated since last year’s draft filing range of ₹1.1–1.2 trillion. The issue now values LG India at about ₹77,380 crore at the upper end of the ₹1,140-a-share price band, according to its red herring prospectus.

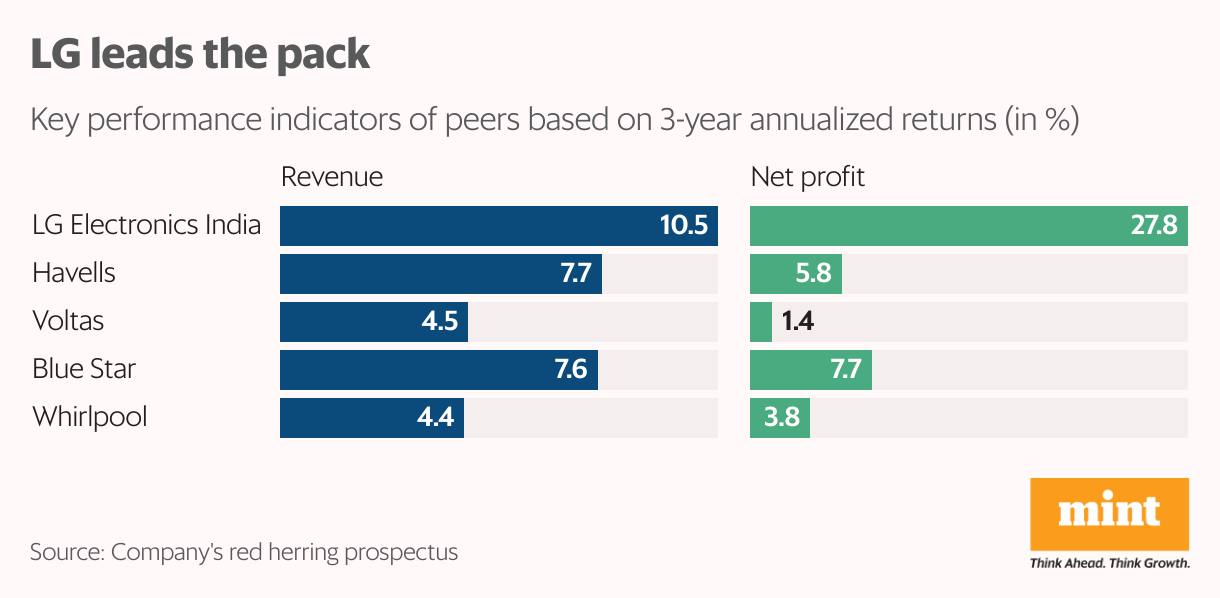

This means investors will be paying about ₹34-35 for every rupee of profit the company earned in FY25. This is well below Havells, Whirlpool, Voltas, and Blue Star, which trade at 47-67x P/E multiples, despite LG’s stronger profitability and scale.

LG’s promoters have left much more on the table for investors, especially as Hyundai’s IPO was deemed expensive last year, according to analysts. Multinational corporations with 40%-plus return ratios usually command higher valuation multiples, so the mid-30s band here signals that investors are getting a quality franchise at a reasonable price, analysts said.

Competitive edge

With a 49% median return on capital employed between FY23 and FY25, LG India is almost thrice as efficient as its peers, as per its IPO filing.

Deep localization, in-house manufacturing of key sub-assemblies and components, a tight supply chain and enduring ties with channel partners have ensured LG’s competitiveness in the domestic market, said Sanjay Chitkara, chief sales officer at LG Electronics India. “Our efficiency prevents sacrifice in margins and supports our premiumisation strategy at scale,” he added.

LG India reported a 7.1% median net profit margin between FY23 and FY25, outperforming all of its competitors. Analysts note that over the past 28 years, LG has cemented its position as a market leader across premium categories in key household appliances such as OLED televisions, front-load washing machines, and five-star inverter air conditioners. This has not only protected margins through pricing power but also lifted sales in the premium category, as Indian consumers have been increasingly opting for higher-end products, aided by easy financing options.

Chitkara said that LG’s strategy has always been to nudge first-time buyers toward premium products and integrate them into its ecosystem. A seamless service network then reinforces brand stickiness, ensuring that when consumers eventually move to higher-end products, LG remains their first choice.

“This helps expand the revenue share of high-margin products while reducing dependence on seasonal demand, supporting consistent revenue and profit growth,” said Ambit Capital’s Jain.

Between FY23 and FY25, LG India’s revenue rose at an 11% CAGR to ₹24,367 crore, while its net profit expanded 28% annually to ₹2,203 crore—nearly 7x the pace of its peers. Strong profitability and the scale of its diversified product mix underpinned this performance, according to the company’s red herring prospectus. Analysts expect the recent Goods and Services Tax (GST) cuts to further lift LG India’s topline in FY26, as lower taxes are likely to spur aspirational purchases.

“GST cuts have permanently reset affordability in TVs and ACs. Buyers will steadily move up to higher specifications, setting new norms for consumption,” said LG India’s Chitkara.

Recipe for growth

Further, he expects the premium mix in durables—now about 17%—to rise to 25-27% by FY29. “LG aims to capture this growth by deepening its premium reach in tier-2 and tier-3 markets as incomes and affordability rise,” he added.

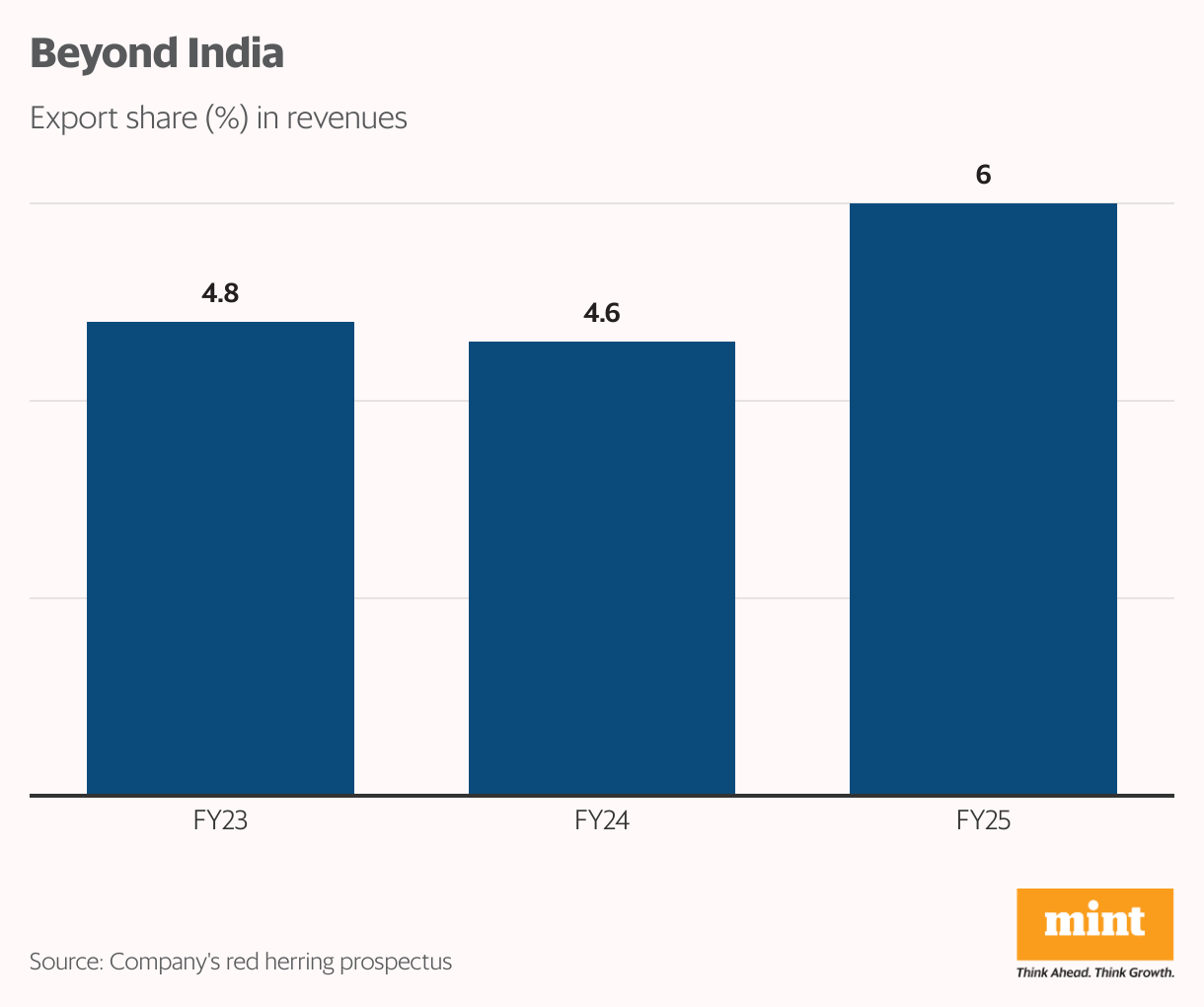

Beyond the domestic market, LG also plans to scale up exports, which currently account for about 6% of its revenue and grew 47% year-on-year. Chitkara expects the upcoming plant at Sri City in Andhra Pradesh to strengthen LG’s east-coast logistics and open new export routes for both entry-level and premium products made in India.

Interestingly, LG India is repositioning itself from a traditional appliance maker to a solutions-led brand, tapping growing demand in the commercial space. The company is broadening its range of climate-control, air-purification, and energy management systems, as well as large-format professional display panels.

These higher-margin solutions are expected to further improve profitability, said Atul Khanna, chief accounts officer at LG India.

Profit vulnerability

However, the market, for now, values LG India largely on its consumer electronics growth prospects, implying slower expansion than peers. With its focus on driving upgrades over low-end penetration, LG’s revenue growth is likely to lag mass-market players, noted experts.

Ambit Capital’s Jain pegs its medium-term growth at 7-9% compounded annual growth rate, versus 15-20% for pure-play AC makers. He cautions that Samsung’s aggressive pricing could also erode LG’s edge in premium categories, while its absence from emerging segments such as wearables and hearables underscores limited innovation beyond legacy products for retail customers.

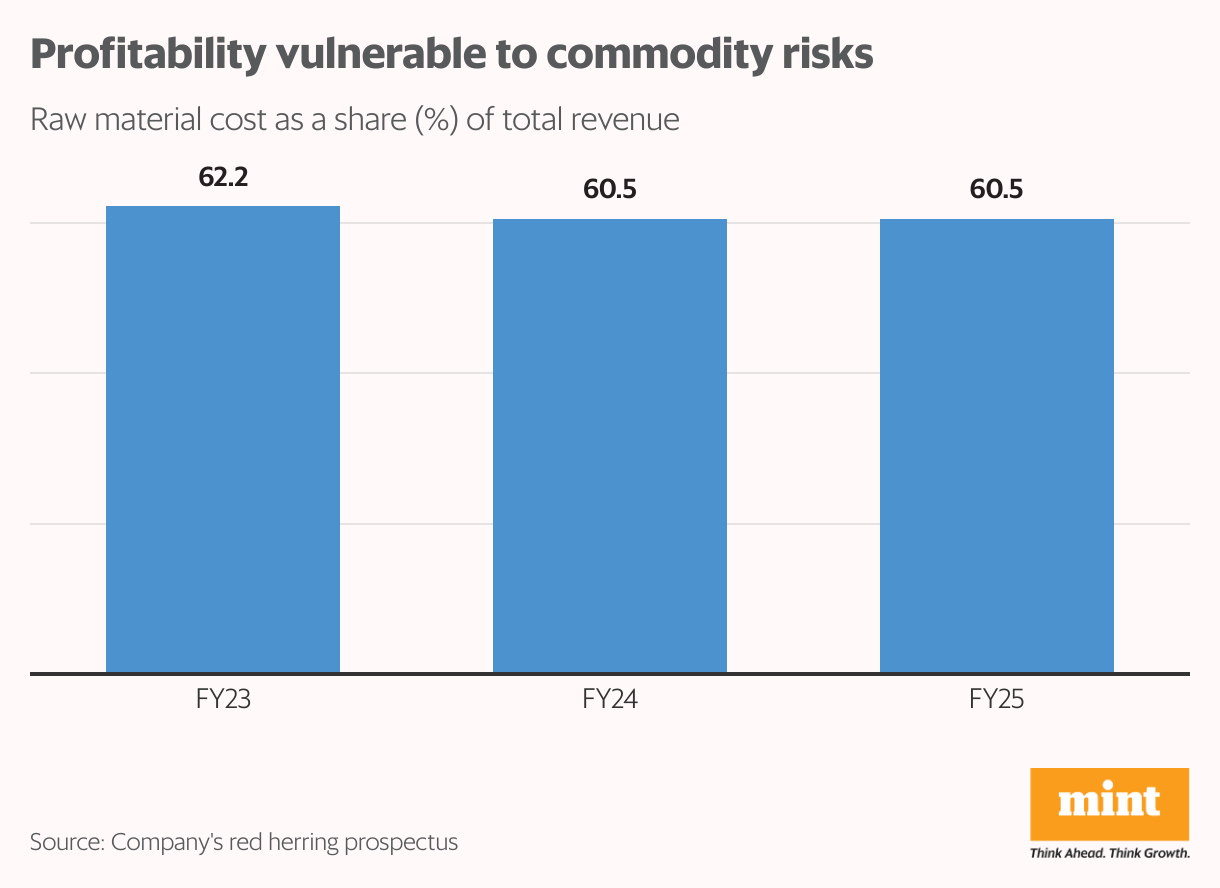

Financial risks remain. Raw material costs make up nearly 61% of LG India’s revenues, leaving profitability vulnerable to swings in commodity and currency markets. The company’s reliance on imported open-cell panels and compressors exposes it to foreign exchange volatility.

It also faces contingent tax liabilities of ₹4,717 crore, which could dent profitability if rulings turn adverse, according to its IPO filing.

But LG India’s debt-free balance sheet and ₹4,570 crore in cash reserves, as of June, should comfort investors, experts said. With limited capital expenditure plans, dividend pay outs could also be healthy, they added.

However, Ambit Capital’s Jain noted that past pay outs—exceeding 100% of profits in FY23 and FY24—largely benefited the parent and might not hold up post listing.

Still, amid global volatility, LG’s domestic focus and brand trust could serve as a steady anchor for investors, even if all proceeds flow back to South Korea.

{kind=link}