Steel Authority of India Ltd (SAIL) shares are down 11% over the past year, despite efforts to amplify capacity.

In its FY25 annual report released this week, SAIL reiterated reaching the production capacity target of 35mtpa (million tonnes per annum) by FY31 from 20mtpa currently. The plan entails a massive total investment of ₹1 trillion. Peak spending of ₹10,000-15,000 crore is expected in FY28-FY29. But a risk to this plan of domestic production oversupply looms, as competitors add substantial capacity.

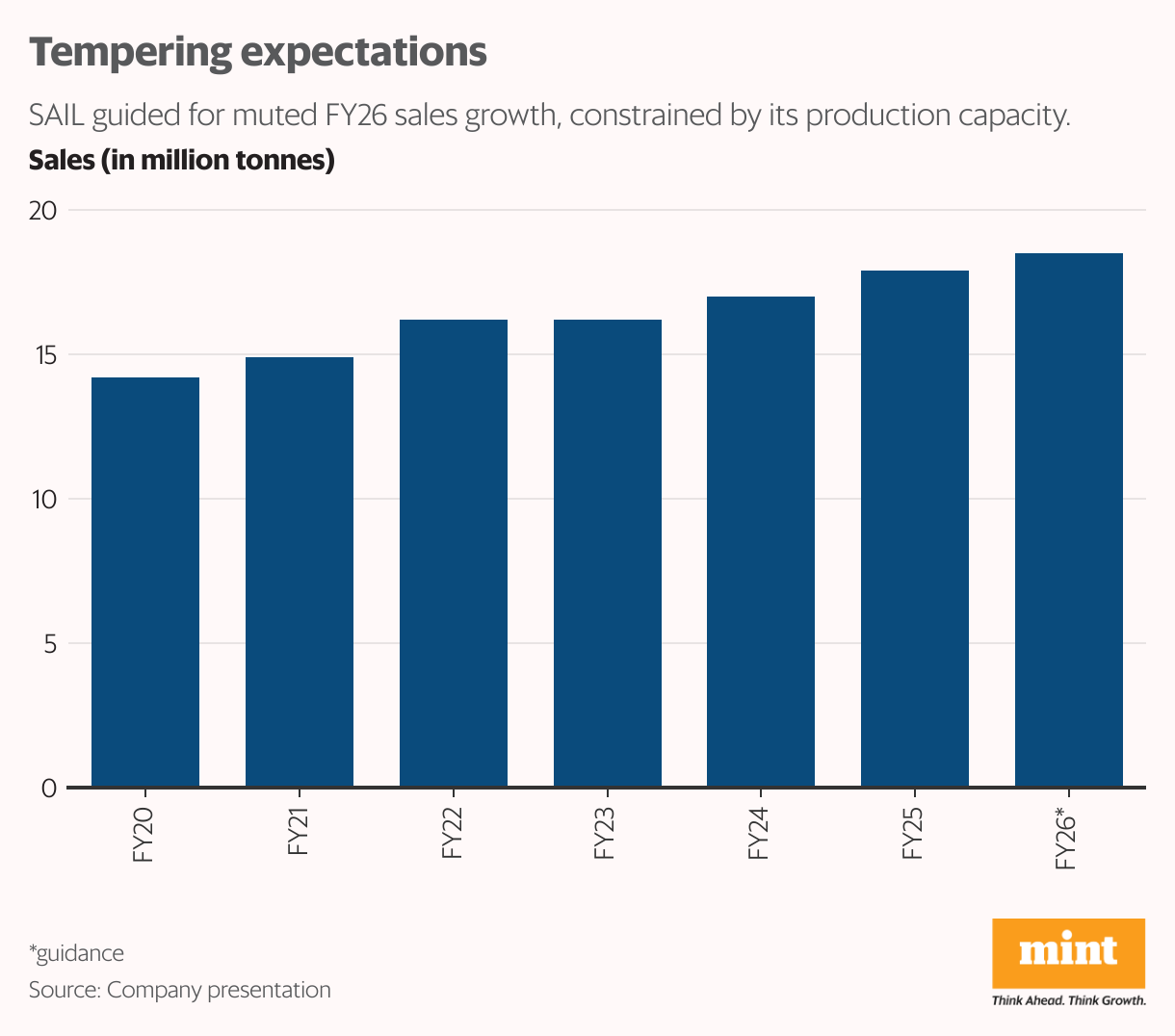

The start to FY26 was unexciting with the management trimming the year’s sales volume guidance to 18.5mt (excluding NMDC Steel sales) from 19.2mt earlier. This is a mere 3% higher than 17.9mt in FY25.

Analysts at IDBI Capital Markets & Securities note that SAIL is lagging behind its peers in capacity addition, and this could potentially slow its volume growth over the next three to five years. “However, additional volumes from NMDC should support topline, albeit with some margin pressure,” added the IDBI report.

SAIL vs peers

SAIL is trailing its peers in some more areas. It faces a significant cost disadvantage. In FY25, employee cost per tonne of production stood at ₹ ₹6,512 against ₹1,817 for JSW Steel and ₹3,943 for Tata Steel (India business).

“High fixed employee costs and lower per capita productivity present challenges in staying competitive with leaner and modernized private players,” the annual report acknowledged.

In the June quarter (Q1FY26), SAIL’s Ebitda/tonne at ₹6,206 (excluding NMDC Steel, sold on a fixed trading margin basis) was much lower than JSW Steel’s ₹11,324. So, in a scenario of oversupply, SAIL’s weak profitability means a severe earnings dent.

SAIL has received some cushion from safeguard duties, which helped net sales realization improve 3% sequentially to ₹51,700/tonne in Q1FY26. Safeguard duty is an additional tax levied on imports to protect domestic producers when imports surge.

While prices declined again in Q2 due to the monsoon, H2FY26 is expected to be strong given the recent recommendation of the Directorate General of Trade Remedies to impose final safeguard duty on flat steel for three years. The duty was imposed on an interim basis in April for 200 days.

Also, SAIL derives advantage with captive iron sources accounting for all of its requirements and is developing two additional mines at Taldih and Gua to meet future requirements. This should aid in costs and prevent it from volatility.

Meanwhile, the stock trades FY26 EV/Ebitda of 6.9X, shows Bloomberg data. Successful execution of planned capex to boost volumes is a key monitorable.

{kind=link}