Demand for consumer durable products is set to rise, fuelled by the income tax relief announced in Budget 2025, which is expected to boost purchasing power. Among the key beneficiaries is Voltas Ltd, though the company is currently navigating the challenge of balancing market share growth with profitability.

Read this | Budget 2025 | A ₹1 trillion largesse for India’s middle class

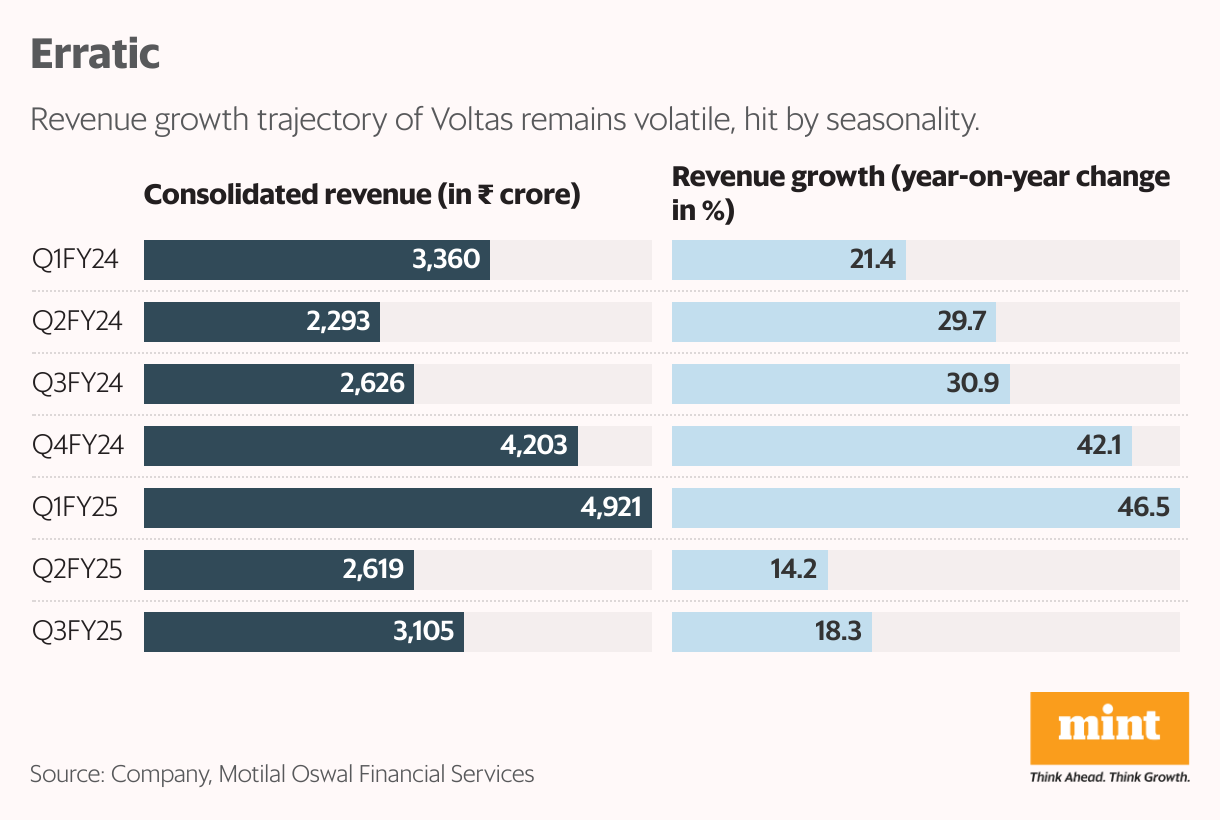

In a seasonally weak December quarter (Q3FY25), Voltas delivered a strong performance, with consolidated revenue increasing 18% year-on-year to ₹3,105 crore. The company also swung to a net profit of ₹130 crore, reversing a loss in the same period last year.

The growth was driven by robust performances in its Unitary Cooling Products (UCP) and Electro-Mechanical Projects (EMP) segments, with the latter posting a profit for the third consecutive quarter, supported by strong execution in both domestic and international markets. The demand outlook remains positive for both segments.

Read this | Voltas’ fortune tied to AC business despite Voltbek optimism

However, market share trends in key categories present a mixed picture.

Voltas’ room air conditioner (RAC) market share saw a marginal sequential dip, ending December 2024 at 20.5%, compared to 21% in September 2024, though it improved year-on-year. The company refrained from price hikes in Q3, given the seasonally weak demand, and instead focused on boosting sales volume, the management said.

In other home appliances, Voltas Beko, the company’s joint venture in refrigerators and washing machines, holds a market share of 5.1% and 8.3%, respectively. Meanwhile, air cooler market share stood at 11.1%.

To further strengthen its position, Voltas has been actively expanding its product portfolio. It recently invested ₹450 crore in its Chennai facility to ramp up production and has earmarked an additional ₹400 crore for backward integration, including a new compressor plant.

Margin concerns

But investors are losing their cool due to subdued margins.

In Q3FY25, Ebitda margin stood at 6.4%, missing the consensus estimate of 6.8%. This was led by the pressure on UCP’s margins primarily due to brand spends during the off-season and the clearing of weak commercial refrigeration inventory. Even so, the management has retained its high single-digit margin guidance for this segment for Q4FY25, banking on summer-driven demand to turn the tide.

Read this | Dixon Technologies: A flurry of acquisitions, collaborations, and capacity expansions

As things stand, earnings estimates have been trimmed.

“We cut our earnings per share estimates by 8% for FY25 and 14% for FY26/FY27 each, considering lower margin in the UCP segment (reduced segment margin by 70bp through FY25-27) and higher loss in Voltbek until FY27 as focus on network expansion/branding will continue,” said Motilal Oswal Financial Services report on 30 January.

Also read | For Godrej Consumer Products, growth initiatives offer a ray of hope but cost pressures loom

Meanwhile, in FY25 so far, the Voltas stock has risen by 27%, outperforming the S&P BSE Consumer Durables Index’s 15% returns. The management expects Voltbek Ebitda break-even in FY26, if achieved, could be among the key re-rating triggers for the stock.

{kind=link}